Private equity secondaries have experienced a remarkable transformation over the past decade, evolving from a niche corner of the alternatives market into a fundamental component of the private capital ecosystem. Historically, secondaries were primarily used as a liquidity tool for limited partners seeking to exit investments before the end of a fund’s life. Today, however, the market has become a sophisticated and strategic asset class in its own right, providing investors with liquidity, flexibility, and access to private market opportunities at scale.

- The Growth of the Major Secondary Platforms

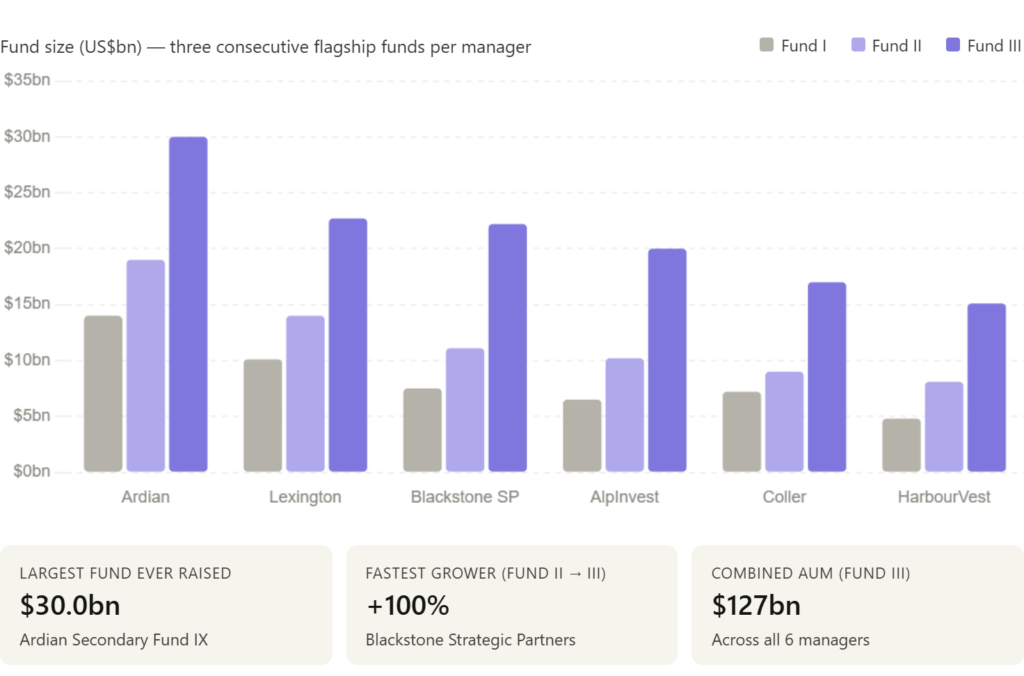

- Ardian

- Lexington Partners

- Blackstone Strategic Partners

- Carlyle AlpInvest

- Coller Capital

- HarbourVest Partners

- Key Insights From the Growth Trajectory

- 1. The Latest Funds Saw the Sharpest Growth

- 2. The Largest Secondaries Fund Now Exceeds the Largest Buyout Fund

- 3. GP‑Led Deals Now Represent Nearly Half of Market Volume

- 4. Slower Traditional Exits Are Fueling Demand

- The Growth Story Isn’t Over

- Conclusion

As private markets have grown significantly, the demand for liquidity within an otherwise illiquid asset class has increased alongside them. The secondaries market has emerged as a key solution, facilitating capital recycling and enabling investors to manage portfolios more dynamically.

This evolution is reflected in the rapid growth of the industry’s leading platforms. Firms that were once specialist secondaries managers have developed into multi-billion-dollar franchises, with fund sizes expanding dramatically over time. What was once a market characterised by $5–10 billion vehicles now includes funds raising more than $20–30 billion. A small group of leading firms has come to dominate the upper end of the market, highlighting how secondaries have progressed from a largely administrative liquidity mechanism to a mainstream and increasingly important asset class.

The Growth of the Major Secondary Platforms

The expansion of secondaries is best captured through the fund‑raising arcs of the six largest managers. Each has scaled aggressively, with the most recent vintages marking the sharpest step‑ups.

Ardian

$14.0bn → $19.0bn (+36%) → $30.0bn (+58%) Ardian has cemented its position as the global leader in secondaries. Its $30bn Secondary Fund IX is now the largest secondaries fund ever raised, surpassing even the biggest buyout funds.

Lexington Partners

$10.1bn → $14.0bn (+39%) → $22.7bn (+62%) Lexington has consistently grown its flagship program and remains one of the most active LP portfolio buyers globally.

Blackstone Strategic Partners

$7.5bn → $11.1bn (+48%) → $22.2bn (+100%) Under Blackstone’s ownership, Strategic Partners has doubled its fund size and expanded aggressively into GP‑led deals and infrastructure secondaries.

Carlyle AlpInvest

$6.5bn → $10.2bn (+57%) → $20.0bn (+96%) AlpInvest has leveraged Carlyle’s global platform to scale its secondaries franchise and broaden its mandate.

Coller Capital

$7.2bn → $9.0bn (+25%) → $17.0bn (+89%) One of the original pioneers of the asset class, Coller continues to grow despite increased competition.

HarbourVest Partners

$4.8bn → $8.1bn (+69%) → $15.1bn (+86%) HarbourVest’s Dover Street program remains a cornerstone of the market, with strong LP relationships and a diversified strategy.

Key Insights From the Growth Trajectory

1. The Latest Funds Saw the Sharpest Growth

Across all six managers, the latest fund vintage has delivered the most significant increase in fund size, highlighting the accelerating growth of the secondaries market.

Several factors are driving this expansion, including rising demand from limited partners for liquidity solutions, broader acceptance of secondaries as a strategic portfolio management tool, and the rapid development of GP-led transactions as a mainstream segment of the market.

Importantly, these increases are not merely incremental. They represent a fundamental shift in the scale and importance of the asset class, underscoring how secondaries have evolved into a core component of modern private market investing.

2. The Largest Secondaries Fund Now Exceeds the Largest Buyout Fund

Ardian’s $30 billion Secondary Fund IX has surpassed the size of the largest buyout fund ever raised, CVC Capital Partners Fund IX, which closed at $29.2 billion. This milestone highlights a profound shift within private markets. Secondaries are no longer viewed as a complementary or niche investment strategy; they have evolved into a standalone mega-fund asset class, capable of attracting capital on a scale comparable to — and now exceeding — the industry’s largest traditional buyout vehicles.

3. GP‑Led Deals Now Represent Nearly Half of Market Volume

Historically, the secondaries market was largely driven by limited partner (LP) portfolio sales. Today, however, GP-led transactions—particularly continuation funds—represent nearly half of total market activity.

This evolution has been fuelled by several factors, including longer private equity holding periods, sponsors seeking to retain ownership of their highest-quality assets, growing demand from LPs for greater flexibility, and the increasing use of structured liquidity solutions.

As a result, continuation funds have significantly broadened the role of secondaries within private markets, transforming the market from a simple liquidity mechanism into a sophisticated tool for portfolio management, value creation, and capital recycling.

4. Slower Traditional Exits Are Fueling Demand

The private equity exit environment has remained challenging in recent years. IPO activity continues to be subdued, merger and acquisition volumes have declined, holding periods have extended beyond historical norms, and valuation expectations between buyers and sellers remain difficult to reconcile.

Against this backdrop, the secondaries market has emerged as an important source of liquidity and flexibility. By facilitating transactions when traditional exit routes are constrained, secondaries provide a valuable mechanism for price discovery, capital recycling, and attractive risk-adjusted return opportunities for both buyers and sellers.

The Growth Story Isn’t Over

Several of the industry’s leading managers are already back in the market with successor vehicles, each seeking to raise even larger pools of capital than their predecessors.

- Lexington Capital Partners XI — targeting $25 billion

- Blackstone Strategic Partners X — targeting $22.5 billion

- HarbourVest Dover Street XII—targeting $20 billion

If these fundraising efforts are successful, they will further accelerate the growth of the secondaries market and reinforce its position alongside the largest buyout and infrastructure strategies. The scale of these funds suggests that secondaries are increasingly competing for capital on equal footing with other private markets mega-fund categories.

Conclusion

Private equity secondaries have transformed from a specialised liquidity solution into one of the fastest-growing segments of the private markets landscape. The dramatic increase in fund sizes, the expansion of GP-led transactions, and the growing dominance of large specialist platforms all signal a market that is rapidly maturing and gaining strategic importance.

With the next generation of funds already targeting record-breaking capital raises, the growth trajectory of the secondaries market remains firmly intact. Far from being a temporary trend, secondaries are becoming a core pillar of private markets and could ultimately redefine the balance of power across the broader alternatives industry.