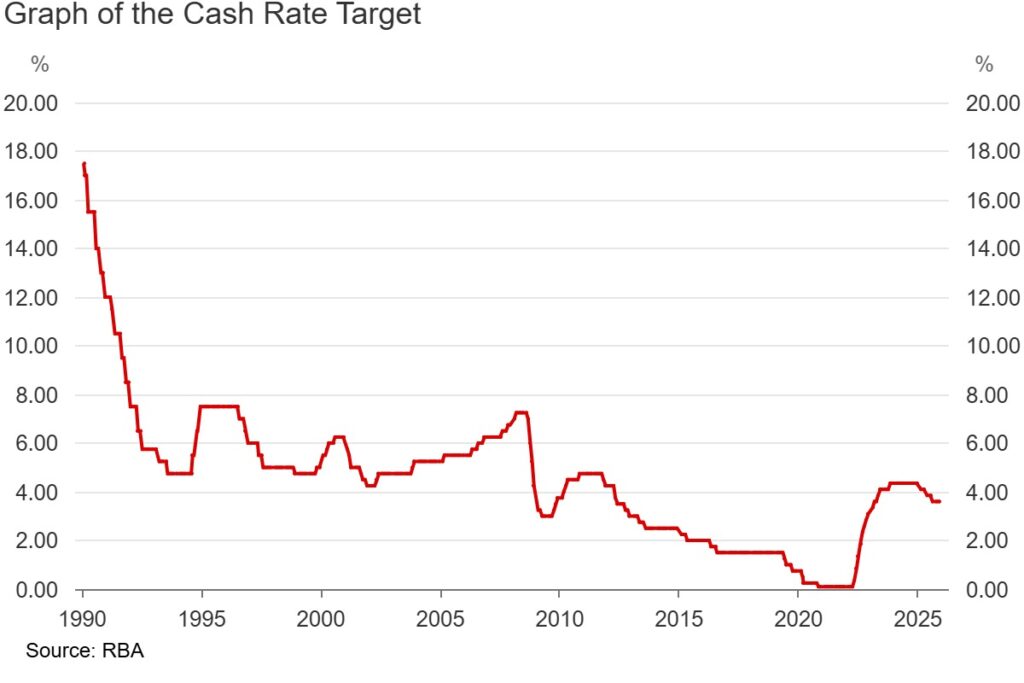

The risk of an RBA rate hike February 2026 has moved sharply back into focus after a stronger-than-expected household spending print challenged the market’s soft-landing narrative. For ASX investors, the question is no longer just when rate cuts arrive, but whether the Reserve Bank has been handed fresh justification to tighten policy once more, even as equity markets hover near record levels. Latest data show consumer spending accelerating into the Black Friday and early Christmas period, complicating the disinflation story and forcing markets to reassess how restrictive monetary policy may remain through early 2026.

The Spending Data That Shifted the Narrative

The latest household spending indicator showed November spending rising by around 1% month on month, with annual growth still running well above levels consistent with a clean disinflation path. Discretionary categories such as retail, travel and selected services surprised to the upside, helped by aggressive Black Friday promotions and a labour market that remains tighter than many expected this late in the cycle.

Market reaction was swift. Over the weekend, rate markets repriced the probability of a February hike, and the ASX 200 slipped modestly as investors reassessed the near term policy outlook. The index is still close to all time highs, but sentiment has shifted from debating cut timing to acknowledging renewed hike risk first.

What This Means for the RBA’s Next Decision

Economists are now openly discussing the possibility of a 25 bps hike in February, particularly if upcoming inflation and wages data refuse to cool. The logic from Martin Place is familiar and consistent.

Consumer spending remains strong enough to threaten progress on inflation. The labour market is still tight, keeping wage pressure elevated. The RBA has repeatedly stated it would rather risk doing too much than allow inflation expectations to re accelerate. For markets, that combination points to higher short term rates for longer, a firmer Australian dollar and renewed pressure on sectors that have been trading on early rate relief assumptions. Westpac’s latest FX commentary notes the AUD has remained well supported into early 2026, reflecting commodities strength and relative rate expectations versus offshore peers.

Sector Winners and Losers if Rates Rise Again

If the RBA does move in February, the impact across the ASX will not be uniform.

Sectors under pressure

Domestic cyclicals including discretionary retail, housing exposed names and smaller cap industrials that rely heavily on Australian demand. Highly leveraged REITs and property developers facing higher funding costs and softer valuation support.

Relative winners

Resources and energy, which remain driven more by global demand and commodity pricing than domestic consumption alone. Exporters with US dollar revenues and contained local cost bases, particularly if AUD strength remains orderly rather than explosive. Banks sit squarely in the middle. Higher rates can support net interest margins, but rising arrears and slower credit growth cap upside if household stress begins to emerge.

Read More

How ASX Investors Might Frame the Risk

For long only investors, the household spending surprise argues for incremental caution rather than wholesale retreat. Favour balance sheet strength and genuine pricing power over simple cyclical leverage.

Tilt toward sectors less exposed to Australian household demand and more aligned with global growth or structural themes such as resources, healthcare and selected profitable tech.

Keep dry powder available, as a February hike combined with a hot US data print could deliver the pullback needed to upgrade portfolio quality at better prices.

The broader takeaway is simple. As long as spending and wages stay resilient, the RBA rate hike February 2026 risk remains alive, and equity markets will need to work harder to justify stretched valuations in rate sensitive parts of the ASX.