Business Description

Fortescue Ltd. (ASX: FMG), headquartered in Perth, has transformed from a traditional iron‑ore‑focused miner into a diversified global enterprise spanning green energy, technology, and future‑facing metals. Fortescue is one of the world’s largest iron ore producers, operating major hubs in the Pilbara region of Western Australia. This includes the Chichester and Solomon hubs, plus newer assets such as Eliwana and Iron Bridge. It ships close to 200 million tonnes of iron ore annually to customers, primarily steelmakers in China and other Asian markets, and is recognised as a low‑cost producer.

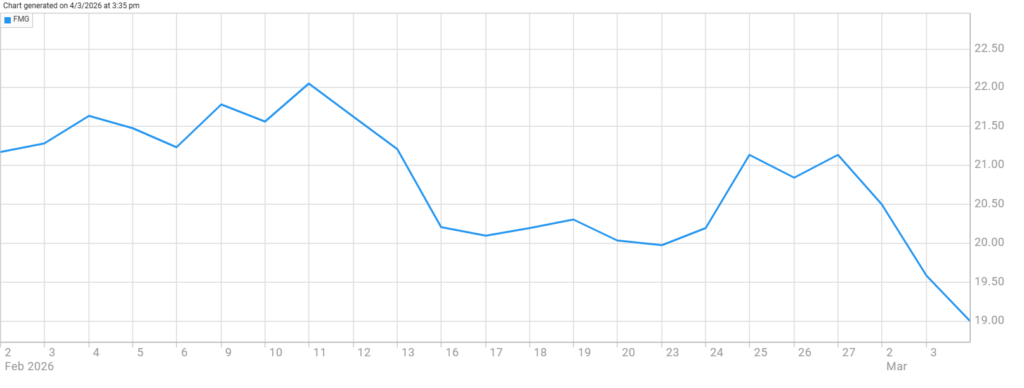

Fortescue Down 12% in the Past Month: Good Time to Invest?

Fortescue offers compelling value now with record H1 FY26 shipments, lowest‑in‑class costs, and 23% EBITDA growth supporting a bigger dividend. A rock‑solid balance sheet (US$4.7B cash vs. US$1B debt) funds green energy expansion. Shares are attractively priced for iron ore resilience and diversification upside amid the energy transition.

Positive Insights:

- Exceptional Production Levels and a Leading Low‑Cost Position—The company reported record iron ore shipments of 100.2 million tonnes in H1 FY26, a 3% increase on the prior corresponding period. It also preserved its position as a lowest‑cost producer, with Hematite C1 unit costs reduced to US$18.64 per wet metric tonne, a 3% improvement attributed to operational efficiencies and decarbonisation measures that cut diesel use. This combination of higher volumes and lower costs is supporting robust margins despite ongoing volatility in iron ore prices.

- Robust Financial Results and Compelling Shareholder Returns—In H1 FY26, Fortescue’s underlying EBITDA climbed 23% to US$4.5 billion, The net profit after tax is rising by a similar margin to US$1.9 billion. This performance underpinned a fully franked interim dividend of A$0.62 per share, up 24% year on year and equating to a robust 65% payout ratio, underscoring the company’s ongoing willingness to return capital to investors in favorable conditions. With cash of US$4.7 billion against net debt of only US$1 billion. Fortescue’s balance sheet remains strong, providing both a buffer against market volatility and ample headroom to fund future growth projects.

- Expanding Growth Opportunities in Metals, Energy, and Decarbonization—Fortescue is diversifying beyond iron ore into high-growth areas like green energy, electrification, and critical minerals to ensure its long-term role in the global energy transition. Recent progress includes rolling out its first battery energy storage systems, introducing electric mining equipment, and pursuing key acquisitions such as the remaining 64% stake in Alta Copper to expand its presence in strategic metals. These moves are delivering cost savings while building a more diversified revenue stream over time.

2026 Expectations

Fortescue heads into 2026 with solid momentum, supported by record first-half shipments and reaffirmed full-year guidance. Strong margins are sustained by industry-leading low costs and ongoing decarbonisation initiatives, including battery storage and electric fleets. A robust balance sheet enables generous dividends and funds growth projects such as Alta Copper and Belinga, helping offset potential China demand risks.

Disclaimer

The Investor Standard provides general information for education and research only. It is NOT personal advice, a recommendation, or an offer to buy/sell any security. This content has been prepared without taking into account your objectives, financial situation or needs. Past performance is not indicative of future results. Before acting on any information, consider its appropriateness and seek independent advice from a licensed financial adviser.