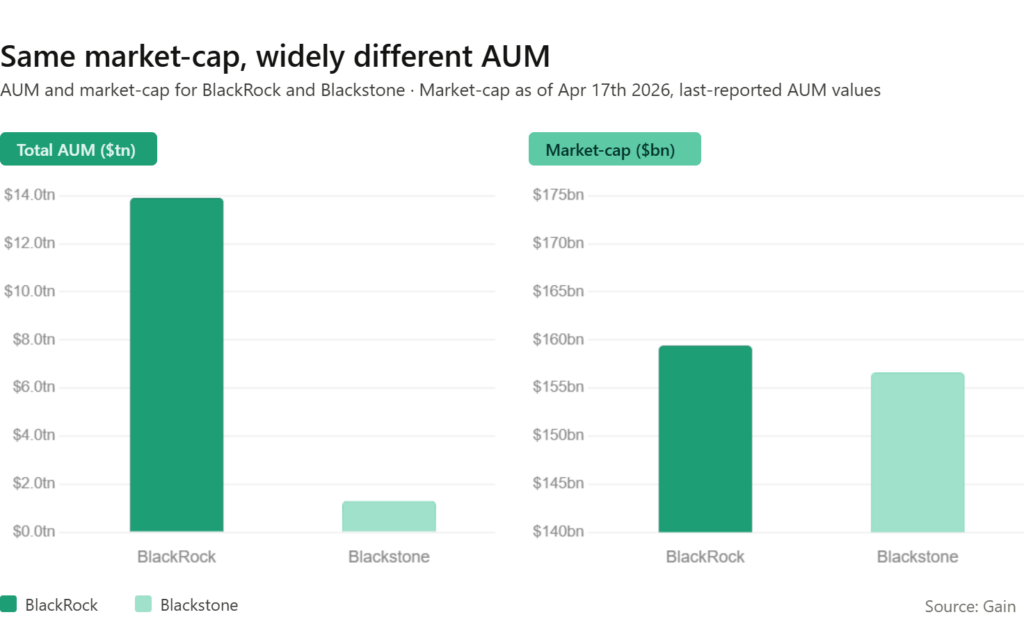

At first glance, BlackRock and Blackstone seem almost indistinguishable. Their names are frequently mixed up, their visual branding carries a similar aesthetic, and, most intriguingly, their market capitalisations sit at nearly the same level: roughly $159.4 billion for BlackRock and $156.6 billion for Blackstone. On the surface, this parity implies two financial giants of comparable scale and influence.

But that impression dissolves quickly once you look beneath the branding. BlackRock manages an extraordinary $13.9 trillion in assets, making it the world’s largest asset manager by a wide margin. Blackstone, while still a heavyweight, oversees about $1.3 trillion, less than one-tenth of BlackRock’s AUM. This dramatic gap naturally prompts a fundamental question: how can two firms with such vastly different asset bases trade at almost identical valuations?

The AUM Illusion

In traditional finance logic, a larger asset base should naturally translate into a more valuable firm. More AUM typically means more fee revenue, greater scale advantages, and stronger market influence. By that reasoning, BlackRock’s valuation ought to tower over Blackstone’s.

But AUM is a blunt metric, useful for headlines, misleading for valuation. Different types of assets generate very different levels of revenue, and even more importantly, vastly different profit margins. A dollar managed in a low-cost index fund produces only a sliver of revenue, while a dollar invested in private equity, private credit, or real assets can generate far higher management fees and lucrative performance fees.

BlackRock: Scale Built on Low Fees

BlackRock’s strength largely comes from its leadership in passive investing, especially through the iShares ETF franchise. Passive strategies track market indices rather than trying to beat them, which allows providers to charge very low fees—often only a few basis points in expense ratios.That low-cost model has been extraordinarily effective at drawing capital. From individual savers to major institutions, investors have steadily shifted into passive vehicles because of their low fees and predictable benchmark-relative performance. BlackRock has been a primary beneficiary of this migration, accumulating trillions in AUM.

The downside of that scale is compressed margins. With fees so thin, BlackRock must rely on enormous asset volumes to produce meaningful revenue, and even then its per-dollar profitability is limited compared with managers in higher-fee niches. Put simply, BlackRock operates a high-volume, low-margin business: vast, highly efficient, and built to move enormous pools of capital rather than to extract large fees from each dollar managed.

Blackstone: Fewer Assets, Higher Margins

Blackstone operates in a very different segment of the investment landscape. Rather than concentrating on liquid public markets, it specialises in private equity, real estate, infrastructure, and private credit—collectively known as alternatives. These strategies command materially higher fees: investors typically pay both management fees (often in the 1–2% range) and performance fees (commonly around 20% of profits, or carried interest). That fee structure enables firms like Blackstone to generate substantial earnings even from a much smaller asset base.

Fee Margins: The True Driver of Valuation

The key difference between the two firms comes down to fee economics. BlackRock generates only a small amount of revenue per dollar of AUM, while Blackstone earns substantially more from each dollar it manages. Investors therefore value not just the size of a firm’s asset base but how effectively it converts that capital into earnings. That helps explain why BlackRock’s enormous AUM does not translate into a proportionally larger market value: despite managing nearly ten times the assets, its earnings power is weaker on a per‑dollar basis. Blackstone’s higher margins and performance‑linked fee streams deliver stronger profitability per unit of capital, so the market places a premium on quality of earnings rather than sheer asset quantity.

The Strategic Shift Toward Private Markets

The gap in fees between public and private markets has become impossible to ignore and is reshaping the asset management industry. Public-market managers are increasingly moving into higher‑margin private strategies to boost profitability and diversify revenue sources. BlackRock has been among the most assertive in this shift, acknowledging the limits of its low‑fee model and pursuing strategic acquisitions to build out its alternatives franchise. Notable deals include Global Infrastructure Partners with $193 billion of AUM, HPS Investment Partners with $185 billion of AUM, and the $3 billion purchase of Preqin, a software and data provider, moves that expand BlackRock’s footprint in infrastructure, private credit, and private-markets technology.

BlackRock’s Acquisition Strategy

One of BlackRock’s most consequential moves was buying Global Infrastructure Partners, adding roughly $193 billion of infrastructure AUM. Infrastructure investments—think energy networks, transport systems, and utilities, tend to deliver steady, long‑dated cash flows and typically command higher fees than plain‑vanilla index products. The firm also acquired HPS Investment Partners, bringing in about $185 billion of private credit assets. Private credit has emerged as a fast‑growing area for asset managers, benefiting from reduced bank lending and strong demand for alternative financing solutions.

BlackRock’s purchase of Preqin for around $3 billion bolsters its private‑markets capabilities by adding a leading source of data and analytics, even though Preqin is not an asset manager itself.Taken together, these deals mark a deliberate strategic shift: BlackRock is extending beyond its passive roots to capture higher-margin opportunities across infrastructure, private credit, and private-markets intelligence.

Convergence or Continued Divergence?

The widening fee gap between public and private markets is reshaping the asset‑management landscape. Public‑market managers are increasingly moving into higher‑margin private strategies to boost profitability and diversify revenue streams. BlackRock has been particularly active in this shift, acknowledging the constraints of its low‑fee model and pursuing strategic acquisitions to expand its alternatives capabilities, most notably Global Infrastructure Partners (about $193 billion AUM), HPS Investment Partners (around $185 billion AUM), and the roughly $3 billion purchase of Preqin, which enhances its private‑markets data and analytics.

Conclusion

The nearly identical market valuations of BlackRock and Blackstone underscore a key lesson in asset management: sheer size does not equal value, what matters is how that size converts into earnings. BlackRock showcases the advantages of scale, dominating global markets with low‑cost, high‑volume products, while Blackstone illustrates the power of margins, extracting greater profitability from a much smaller asset base. Their contrast teaches investors and industry participants that in a crowded, capital‑rich market, the ability to generate high‑quality, high‑margin revenue is ultimately more valuable than simply managing large sums.

Disclaimer

The Investor Standard provides general information for education and research only. It is NOT personal advice, a recommendation, or an offer to buy/sell any security. This content has been prepared without taking into account your objectives, financial situation or needs. Past performance is not indicative of future results. Before acting on any information, consider its appropriateness and seek independent advice from a licensed financial adviser.