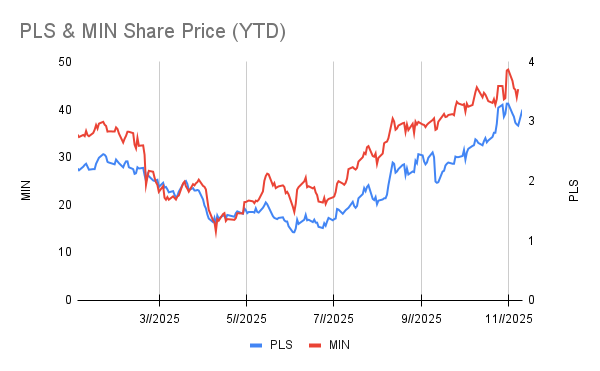

Pilbara Minerals’ CEO says hedge-fund shorts are unwinding in PLS after a sharp rebound in lithium prices. The immediate catalyst: bullish upgrades from Citi (and earlier JPMorgan) lifting medium-term demand assumptions, battery demand up ~31% in 2026, led by energy storage systems (ESS) +45% and EVs +26%. The thesis is simple: grid needs firming and data centres powering AI need stable electricity, both push utilities toward large-scale batteries, expanding lithium’s addressable market beyond autos. On the supply side, China’s CATL is inching toward restarting the Jianxiawo project in Yichun, but timing and ramp speed remain uncertain, enough ambiguity to keep price momentum intact near term.

Why It Matters – Beyond EVs

For the last two years, lithium pricing hinged on a single question: EV unit growth vs supply additions. The market is now broadening that lens. ESS could be ~30% of global battery demand by 2030 (vs ~20% in 2024), according to Citi, material at the margin for pricing during the next up cycle (2026-27). Utilities and hyper-scalers care about total cost of reliability, not just cost per kWh, and in many jurisdictions lithium-ion still clears procurement hurdles faster than alternatives. That demand diversification reduces single-end-market risk and helps earnings durability through EV cycles.

Australia Angle: Implications for Sectors

Lithium miners & developers (ASX)

Higher forward demand assumptions + supply-timing uncertainty support price and margin repair into 2026-27. Short interest unwinds can amplify upside in names like PLS, but operational delivery and cost curves still separate winners from passengers.

Critical-minerals services & contractors

If sentiment stabilises, deferred sustaining and expansion capex can resume, supporting contractors, drillers, and processing upgrades.

Power, utilities, and grid equipment

ESS procurement pipelines should thicken, particularly where renewables penetration/stability gaps meet AI-driven data-centre load growth. The flow-through is more tenders, faster off-takes, and potential policy support.

ETF Flows

After outflows into AI/defence themes, a sustained price base in lithium could pull passive money back into miners, adding a second-order bid to equity prices.

Investor Takeaways

- Demand stack is broadening. ESS is becoming a co-equal driver with EVs in medium-term models that typically compresses the downside tails on price scenarios.

- Supply timing > supply totals. CATL’s Jianxiawo restart is not instantly bearish, ramp curves, permitting cadence and grade/impurity issues dictate when tonnes actually hit spot.

- Positioning matters. Reported short unwinds in PLS highlight why crowding is a risk factor, both ways. Dislocations can overshoot fundamental value on the way up and down.

- Quality still commands the multiple. Balance sheets, cost position (cash costs on the left side of the curve), and conversion optionality (chemical vs concentrate exposure) will dictate who converts a price lift into durable free cash flow.

- Second-derivative checks. Watch downstream indicators, utility ESS RFPs awarded, interconnection queues cleared, hyper-scaler power PPAs mentioning storage components. If those accelerate, the ESS bull case gains credibility.

Risks To The Up-Cycle View

- Faster-than-expected supply return: Quicker restarts (CATL/Yichun and other Chinese or African projects), or accelerated Australian brownfield debottlenecking, cap price upside.

- Chemistry shifts: Sodium-ion or LFP variants with lower lithium intensity scaling faster than expected, especially in ESS.

- Policy/credit risk: EV incentives, grid rules and permitting timelines can whipsaw procurement and commissioning schedules.

Read More

Near-Term Signposts

- ESS awards and utility filings in key markets; data-centre power procurement with attached storage.

- Chinese permit flow and ramp profiles at Jianxiawo; shipment data vs guidance.

- Broker model revisions: If more houses converge on ESS-led demand and push through 2026-27 price upgrades, the equity bid broadens.

- ETF flow reversal: Stabilising spot and margin guidance could turn passive outflows into inflows for ASX lithium baskets.

Base Case Outlook – Balanced, Not Breathless)

Upgrades from Citi and JPMorgan plus supply-timing uncertainty improve the skew for prices into 2026-27, but it’s a repair, not a straight-line melt-up. Expect choppy progress, better floors, volatility earnings, where quality operations translate any price lift into cash, and crowded positioning does the rest. For Australia, that means lithium can re-enter a constructive phase, especially where ESS demand is visible and projects sit on the left side of the cost curve.

Disclaimer

General information only. This is not financial advice and does not take into account your objectives, financial situation or needs. Consider your own circumstances or seek professional advice before acting.