The Quiet Compounder with Embedded Optionality

Wesfarmers remains one of the highest quality compounders in the Australian market, combining mature, high return retail franchises with measured exposure to lithium and emerging digital monetisation platforms. It is not flashy.

Headquartered in Perth, the group spans home improvement, discount department retail, office supplies, chemicals, energy, fertilisers and health related distribution, creating a diversified earnings base that smooths volatility while preserving capital allocation flexibility.

The investment appeal is its barbell structure, dependable cash generation from Bunnings and Kmart on one side, with lithium, retail media and data platforms offering asymmetric upside on the other.

In H1 FY26, Wesfarmers reported revenue of $24.2 billion, up 3.1%, EBIT of $2.493 billion, up 8.4%, and NPAT of $1.603 billion, up 9.3%, reflecting margin discipline and productivity leverage.

The interim fully franked dividend was lifted to $1.02 per share.

Governance and Capital Discipline

Wesfarmers is led by Managing Director Rob Scott and operates with a board structure typical of an investment grade industrial, with strong emphasis on governance, safety and disciplined capital allocation. Chair succession is also in motion. The group has flagged that Chairman Michael Chaney will retire following the 2026 AGM, with Ken MacKenzie expected to join the board from 1 June 2026 as successor. Continuity reduces uncertainty.

Management commentary consistently emphasises return thresholds, productivity programs and balance sheet strength, which frames how new investments are assessed and why excess capital is periodically returned to shareholders.

Investment Thesis

Our core thesis remains straightforward. Wesfarmers is a high return compounder supported by category dominant retail assets. Protected by scale advantages and productivity initiatives, with lithium and digital platforms providing optional upside without threatening balance sheet stability. The near term share price setup is balanced.

On the positive side, EBIT and NPAT growth outpaced revenue in H1 FY26, reinforcing operating leverage and margin control, while dividend growth signalled confidence in cash generation. On the watchlist side, the Covalent Lithium joint venture ramp up has been extended due to intermittent odour issues at the lithium hydroxide refinery, creating headline risk around execution timing even as first product has been achieved and remediation works are underway. Lithium sentiment moves quickly. Retail sentiment moves gradually.

Management has also noted uneven cost of living pressure and sensitivity to interest rate expectations, which can influence discretionary mix even when value retailers continue to gain share.

Divisional Performance Snapshot

The familiar Wesfarmers pattern continued in H1 FY26. Modest top line growth paired with stronger profit expansion driven by cost discipline and productivity initiatives.

Bunnings

Bunnings delivered revenue of $10.713 billion, up 4.2%, with EBT excluding property contribution of $1.389 billion, up 5.0%, and rolling 12 month return on capital of 70.8%. Those are elite retail returns. Category leadership remains intact. Investment continues across digital, marketplace expansion, commercial trade penetration and retail media monetisation, reinforcing its structural moat.

Kmart Group

Kmart Group reported revenue of $6.307 billion, up 3.3%, and EBT of $683 million, up 6.1%, with return on capital of 69.8%. Value positioning is resonating. Digitisation of supply chain and store operations is improving productivity while expanding addressable market share across Australia and New Zealand.

Officeworks

Officeworks grew revenue by 4.7% but saw earnings decline as it commenced a multi year transformation program involving restructuring, ERP replacement and automation investment. Short term margin pressure is intentional. Execution is critical.

WesCEF and Lithium

Wesfarmers holds a 50% interest in Covalent Lithium, where the Mt Holland mine and concentrator reached nameplate capacity during the half, while the lithium hydroxide refinery achieved first production but experienced extended ramp up due to engineering remediation works targeted for completion mid CY26. Lithium remains optionality. Materiality depends on execution.

Financial Health and Capital Structure

Wesfarmers maintains investment grade credit ratings of A3 stable from Moody’s and A minus stable from S&P Global Ratings. Net financial debt stood at $4.878 billion at 31 December 2025, with Debt to EBITDA of 1.9 times, consistent with a conservatively geared industrial profile. Liquidity remains solid. Committed undrawn facilities total approximately $1.3 billion.

The weighted average cost of debt was 3.56%, with average maturity of 4.5 years. This reflects deliberate term staggering and funding discipline. Free cash flow increased 35.6% to $2.745 billion in H1 FY26, while the cash realisation ratio was 99%. Reinforcing earnings quality.

Dividend policy remains consistent. The interim dividend of $1.02 per share was fully franked, and management continues to reference franking balances, cash flows and credit metrics when determining capital returns.

A separate $1.50 per share capital management initiative was executed in December 2025, comprising a $1.10 capital return and $0.40 fully franked special dividend.

Technical Considerations

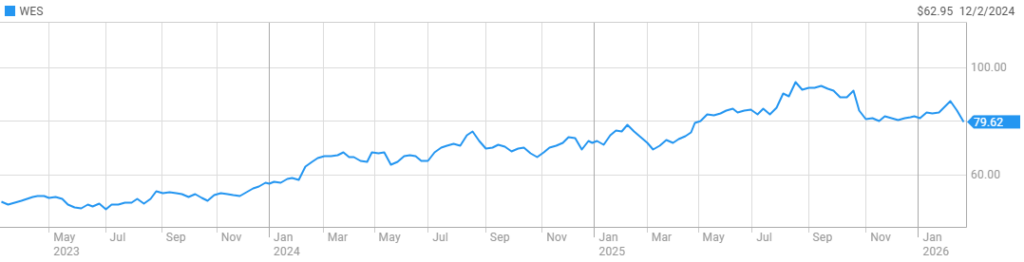

Wesfarmers typically trades as a quality defensive within Australian equities. Meaning macro sentiment and consumer outlook can influence short term price action even when underlying business fundamentals remain stable. The post result reaction range provides near term support and resistance reference points. The broader 52 week trend channel offers the clearer structural guide.

WES often respects longer swing structures rather than short lived volatility spikes, making weekly timeframes particularly relevant for investors focused on medium term positioning.

Read More

Risks to Monitor

Consumer sensitivity remains a live variable.

Officeworks execution risk sits front of mind.

Lithium commissioning timelines may influence sentiment disproportionately to current earnings contribution.

Commodity and energy exposures within WesCEF introduce cyclicality absent from the core retail divisions.

Capital allocation discipline remains critical to preserving the compounder profile investors value.

Outlook and Valuation Framework

In our base case, Wesfarmers enters the second half of FY26 with solid operating momentum, continued productivity focus and sufficient balance sheet capacity to invest while maintaining shareholder returns.

Management commentary suggests retail divisions traded well in the first six weeks of 2H FY26. With Bunnings and Officeworks broadly in line with first half trends and Kmart stronger. WesCEF expects second half earnings modestly ahead of first half based on contracted spodumene volumes.

The swing factors for the next 6 to 12 months are clear. Officeworks stabilisation. Lithium ramp up clarity.

For long term investors seeking a margin of safety. An entry band between $75 and $80 per share appears reasonable, sitting below 52 week highs in the low $90s and above 2026 intraday lows in the low $70s.

An exit or trim range between $85 and $90 aligns with consensus targets in the low to mid $80s while allowing for lithium execution upside should ramp up headlines improve. The compounder remains intact. Optionality adds leverage. Execution determines rerating.

Disclaimer

The Investor Standard provides general information for education and research only. It is NOT personal advice, a recommendation, or an offer to buy/sell any security. This content has been prepared without taking into account your objectives, financial situation or needs. Past performance is not indicative of future results. Before acting on any information, consider its appropriateness and seek independent advice from a licensed financial adviser.