Less than 3 years after bond markets effectively ended the premiership of Liz Truss, Britain’s government bond market is once again flashing warning signs.

Yields on UK government bonds (gilts) have risen above levels reached during the 2022 Truss episode, reflecting growing investor concerns about fiscal sustainability, political instability and rising debt burden.

While the headlines focus on turmoil within Westminster, bond investors are increasingly focused on a more fundamental question: can Britain continue borrowing and spending at current levels without consequences?

The answer from the gilt market appears to be increasingly sceptical.

What Is The Gilt Market?

Gilts are bonds issued by the British government to finance public spending.

When investors purchase gilts, they are effectively lending money to the government in exchange for interest payments and repayment of principal at maturity.

The yield on a gilt reflects the return investors demand for lending to the government.

When yields rise, borrowing and servicing debt becomes more expensive for the government and often signals growing concerns about inflation, debt sustainability or fiscal position.

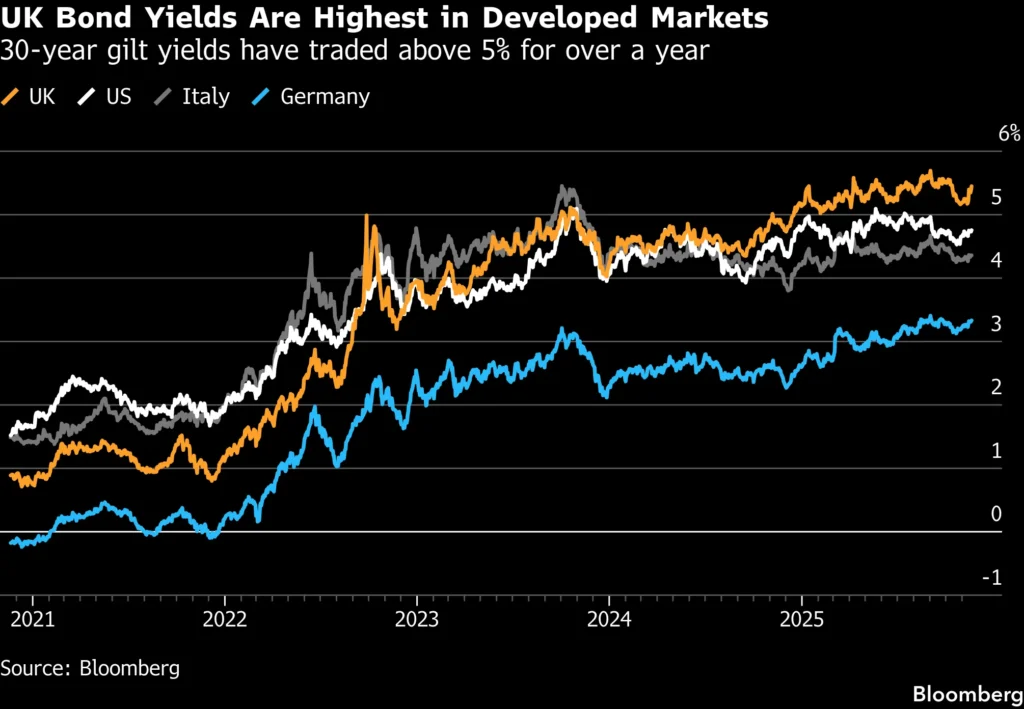

Source: Bloomberg

In recent months, yields have risen sharply as investors have become increasingly concerned about Britain’s economic and political outlook.

Why Are Gilt Yields Rising?

At the heart of the sell-off is a growing concern that Britain has very little fiscal breathing space left.

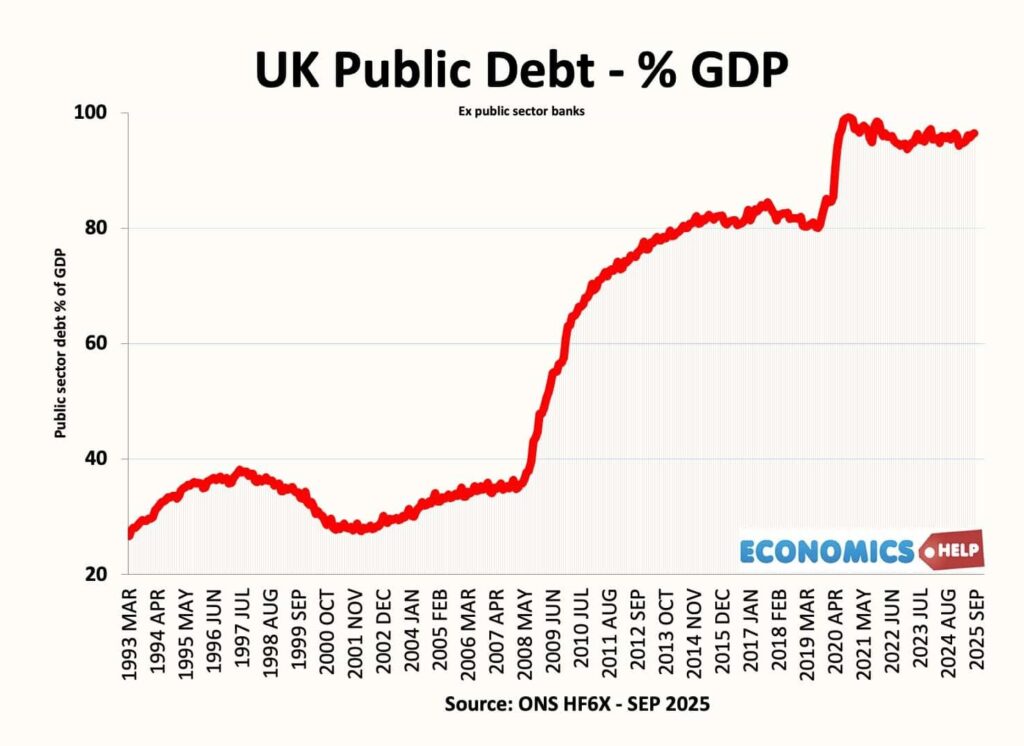

Like many developed economies, the UK emerged from the GFC, COVID-19 and the energy crisis with significantly higher levels of public debt. At the same time, demands on government spending continue to increase through healthcare, pensions, defence and social services.

Investors are increasingly questioning how governments intend to finance these commitments without either raising taxes, reducing spending or increasing borrowing.

The more governments rely on deficit spending with no trajectory to change, the more important market confidence becomes.

Source: Financial Times

Political uncertainty has added to these concerns.

Britain has had five prime ministers in just 8 years, while both major political parties face growing competition from smaller parties on both the left and right. Investors worry that future governments may seek to increase spending in an effort to differentiate themselves politically, further worsening an already difficult fiscal position.

Bond markets increasingly view the risks as skewed towards greater spending rather than greater fiscal restraint. That is precisely the outcome that bond investors dislike.

The Shadow Of Liz Truss

To understand why investors pay such close attention to the gilt market, you have to go back to the events of the Truss episode.

Following the announcement of her government’s “mini-budget”, Prime Minister Liz Truss proposed a series of large unfunded tax cuts that would have significantly increased government borrowing.

Bond markets reacted immediately.

Gilt yields spiked, the pound fell and parts of the pension system came under severe stress. Within weeks, the government was forced into a humiliating reversal and Truss to resign, becoming the shortest-serving prime minister in British history.

This demonstrates something many politicians had forgotten after years of near-zero rates: markets can impose discipline on governments.

What makes today’s situation particularly striking is that UK government bond yields have now risen above the levels reached during the Truss crisis. Unlike 2022, however, there has been no single policy shock. Instead, investors are becoming concerned about Britain’s longer-term fiscal trajectory.

The Gilt Market’s New Power

For much of modern history, it was FX markets that imposed discipline on governments.

Britain experienced this repeatedly throughout the twentieth century. The pound was devalued in 1967, the country was forced to seek assistance from the IMF during the 1970s and the Conservative Major Government suffered a huge blow during Black Wednesday in 1992 when sterling was forced out of the European Exchange Rate Mechanism.

Today, however, the focus has shifted from currencies to gilts.

As exchange rates have become more flexible and central banks have gained greater credibility in controlling inflation, government bond markets have increasingly become the primary mechanism through which investors express concerns about fiscal policy.

Rising bond yields effectively act as a warning signal. They increase borrowing costs, reduce fiscal flexibility and place greater pressure on governments to demonstrate credible plans for managing the budget.

In this sense, bond markets have become a form of financial constraint on policymakers. Governments remain free to spend and borrow, but the price they pay for doing so is increasingly determined by investors rather than politicians and voters.

The lesson from the Truss episode was clear: governments can challenge markets, but markets often have the final say.

Britain Is Not Alone

Britain’s pressures are far from unique.

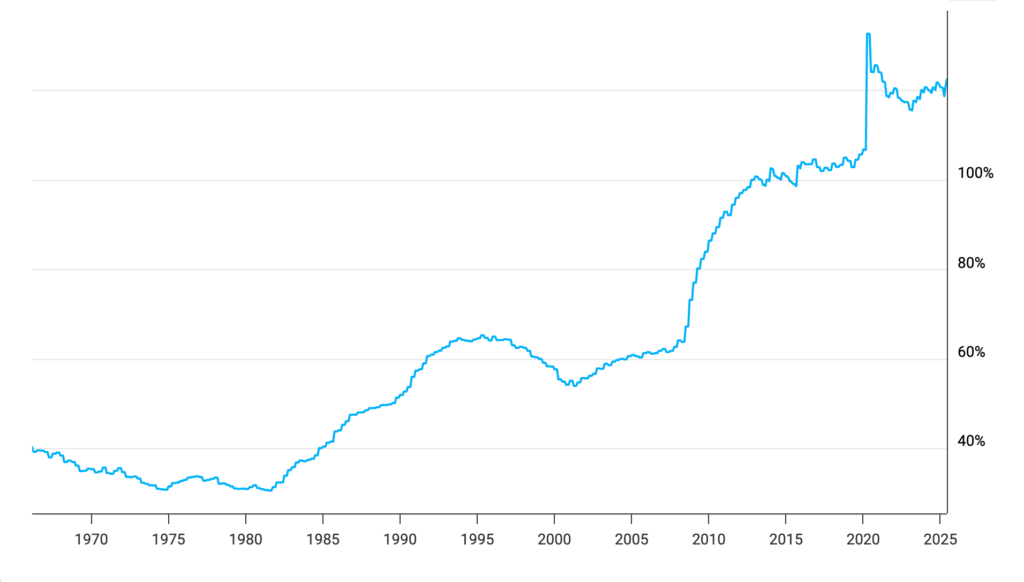

Across much of the developed world, governments are grappling with rising debt levels, ageing populations and increasing demands for public spending. The United States provides perhaps the clearest example.

Prior to the GFC, federal debt stood at roughly 60 per cent of GDP. Today, that figure is closer to 120 per cent. Despite this, both major political parties have continued to support policies that increase deficits, whether through higher spending, lower taxes or both.

The US enjoys advantages that Britain does not. It has the world’s reserve currency, a larger and faster growing economy and a greater ability to finance itself internally. These factors provide a degree of protection from the pressures currently confronting Britain.

However, the underlying issue remains the same. Governments cannot indefinitely increase borrowing faster than their capacity to generate economic growth and tax revenue. Eventually, investors begin demanding compensation for that risk.

US Federal Debt-to-GDP Source: Macrotrends

This risk was shown best when both the UK and US had their credit rating downgraded to AA.

Britain may simply be confronting this reality sooner than most.

What Happens Next?

The warning from Britain’s bond market extends well beyond Westminster.

Investors are not just reacting to the latest political controversy or leadership challenge. They are responding to a broader concern that governments across the developed world have become increasingly reliant on debt while avoiding difficult decisions on taxation and spending.

For now, Britain remains a wealthy, developed economy with deep capital markets and strong institutions. There is no immediate crisis.

But the rise in yields serves as a reminder that fiscal credibility matters. Governments can ignore bond markets for a time, but they cannot ignore them forever.

The question facing Britain is not whether governments can continue spending indefinitely. Bond markets have already answered that.

The real question is whether politicians act before markets force them to and what politicians will do.