California is considering one of the most ambitious tax proposals in American history: a wealth tax, a one-time 5% tax on billionaire wealth.

Supporters of the measure, including economists Gabriel Zucman and Emmanuel Saez, estimate it could raise almost US$100 billion in revenue while affecting only a tiny fraction of the state’s residents. They argue the funds could help address budget pressures and protect public services at a time when federal funding is under strain.

At first glance, the proposal appears compelling. California is home to more billionaires than any other US state, while wealth inequality has widened significantly over the past decades.

Yet critics argue the proposal suffers from a fundamental flaw. It attempts to solve what appears to be a long-term structural deficit problem with a one-time tax on a highly mobile cohort.

Temporary Wealth Tax Won’t Fix Structural Problems

The wealth tax proposal is often framed as a temporary measure designed to fill a one-off budget hole.

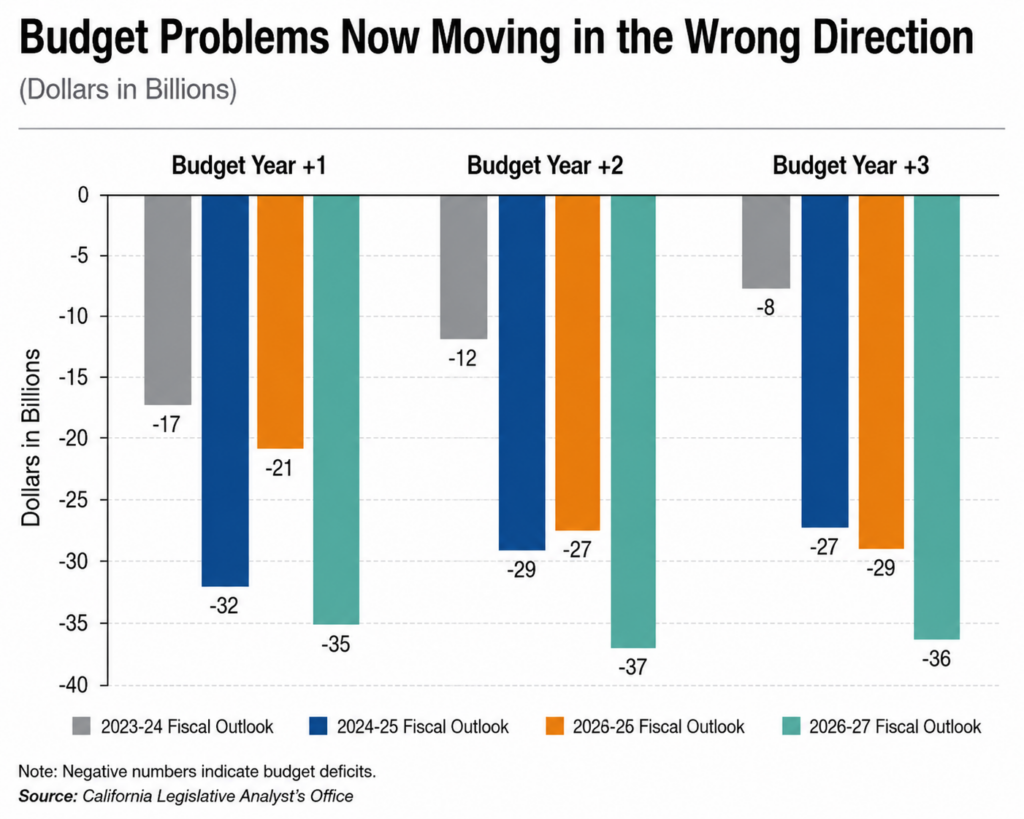

However, California’s own Legislative Analyst’s Office paints a different picture.

The state has faced budget deficits for three consecutive years, including shortfalls of US$27 billion, US$55 billion and US$15 billion. More importantly, the Legislative Analyst’s Office projects ongoing structural deficits of between US$15 billion and US$25 billion annually through 2028-29.

In other words, California’s challenge may not simply be a temporary revenue shortfall. It may be a recurring mismatch between government spending and government revenue.

This distinction matters. A one-time tax can help close a one-time gap. It cannot permanently solve a problem that reappears year after year.

And the office points this out, they write that the budget problems were addressed mostly with temporary fixes, such as reducing one-time spending, using budgetary borrowing, withdrawing reserves, and temporarily increasing revenue.

The fact California has repeatedly relied on temporary measures to balance its budget or bring down its deficit suggests the problem is more likely cyclical not structural. If expenditures continue to grow faster than revenues, a one-time wealth tax may simply postpone rather than solve the state’s fiscal challenges.

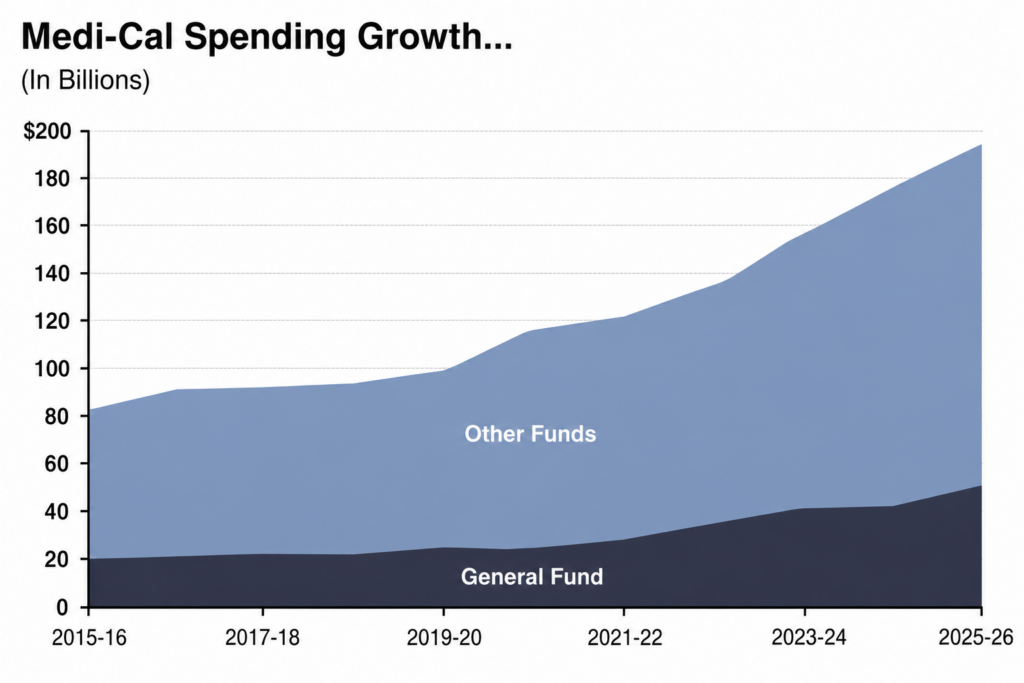

Medi-Cal Is Consuming A Growing Share Of The Budget

One reason California’s budget challenges appear structural rather than temporary is the rapid growth of Medi-Cal spending.

Medi-Cal, California’s version of Medicaid, is one of the largest programmes in the state budget. On a total spending basis, it is the largest, accounting for almost 40 per cent of state spending.

The programme’s cost has increased dramatically over the past decade. Total Medi-Cal spending has risen from roughly US$80 billion in 2015 to almost US$200 billion in 2025. During the same period, enrolment has increased from approximately 12 million people to 15 million. This represents an 80% increase in real spending on just Medi-Cal.

However, the increase is not solely due to a larger number of recipients but actually driven by an increase spending per enrolee. Spending per enrolee has also increased, reflecting both rising healthcare costs and expansions in the scope of benefits provided by the programme.

This does not necessarily mean the spending is unjustified. Healthcare is an essential public service, and these expenditures provide critical coverage to millions of Californians.

However, it does highlight a broader challenge. If major spending programmes continue to grow faster than government revenues, fiscal pressures are likely to persist regardless of whether California implements a one-time wealth tax.

The Mobility Problem

The strongest criticism of wealth taxes is that they may be difficult to collect.

Unlike land, buildings or natural resources, wealthy individuals can often change their place of residence. California therefore faces a challenge that national governments do not. It is not competing just against foreign countries, but against other US states.

States such as Florida, Texas and Nevada impose no state income tax and have increasingly become destinations for high-net-worth individuals seeking a lower tax burden. A billionaire who relocates from California to one of these states can potentially save hundreds of millions of dollars in future taxes.

Supporters of the proposal argue this risk is overstated. Economists Emmanuel Saez and Gabriel Zucman contend that the tax would apply to California residents as of 1 January 2026, making it difficult for a significant number of billionaires to relocate in time to avoid the levy.

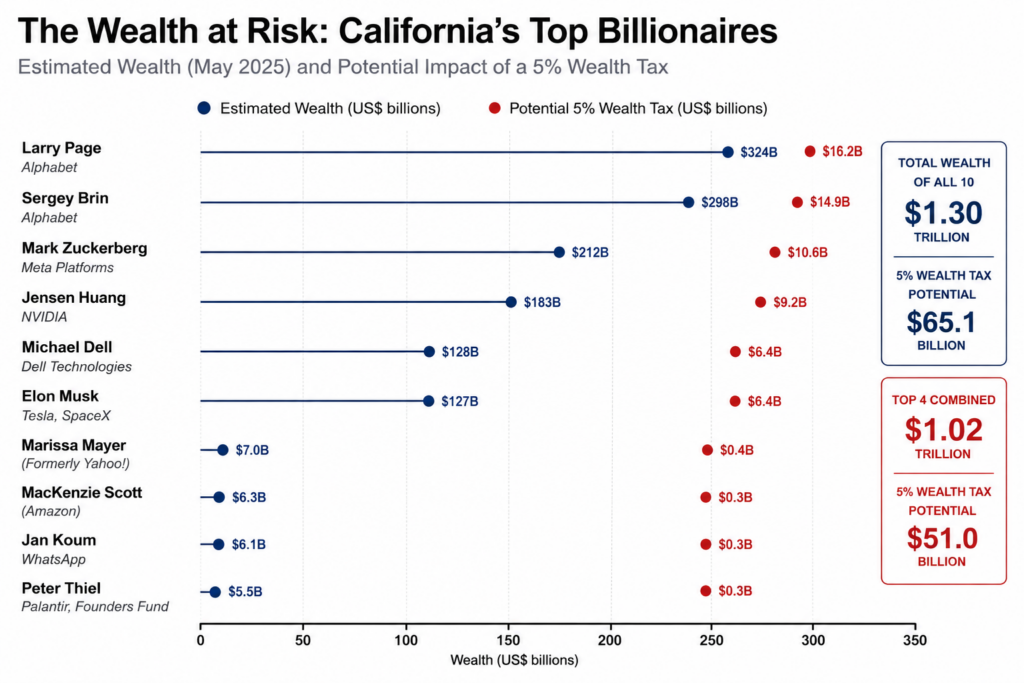

Critics, however, point to reports that several prominent technology billionaires, including Mark Zuckerberg, Larry Page and Sergey Brin, 3 of Californias richest billionaires, purchased property in Florida following the proposal’s announcement and another billionaire Peter Thiel has already moved out. While purchasing property does not necessarily establish legal residency, it raises questions about how mobile California’s tax base may be if such policies become permanent.

California’s 3 richest leaving along with Peter Thiel takes over $760 billion of wealth out of the state.

The issue is not whether every billionaire will leave. The issue is whether enough leave to materially reduce the revenue the tax is expected to generate.

California’s Real Asset

Lost amid the debate over tax revenue is a more fundamental question: what made California wealthy in the first place?

California is home to some of the most valuable companies ever created, Alphabet, Meta, Nvidia, Broadcom etc. These firms have generated trillions in market value, employed hundreds of thousands of workers, paid tens of billion in state corporate and payroll tax and helped establish California as one of the world’s leading centres of innovation.

The billionaires targeted by the proposed wealth tax didn’t accumulate their wealth in isolation. Their fortunes are largely tied to companies that were founded, built and scaled within California’s economic ecosystem.

This matters because the economic contribution of successful entrepreneurs extends well beyond their personal tax payments. The companies they create employ workers, attract investment, generate corporate profits and contribute substantial income, payroll, company, sales and property tax revenue.

From this perspective, California’s greatest asset may not be billionaire wealth itself, but its ability to attract and retain the people and businesses responsible for creating that wealth.

Critics of the proposal therefore argue that policymakers should be cautious about targeting a group that plays a disproportionately large role in the state’s economy. Even if only a small number of entrepreneurs and investors choose to relocate, the long-term economic impact could extend far beyond the revenue collected from the tax itself.

The Bigger Question

Ultimately, the debate over California’s wealth tax is not really about billionaires.

It is about whether governments can solve structural spending challenges through one-off taxes on a highly mobile tax base.

Supporters view the proposal as a matter of equity and fiscal necessity, while critics view it as an attempt to address a recurring budget problem with a temporary source of revenue while risking the departure of some of the state’s most economically productive residents.

California may yet succeed in collecting billions through a wealth tax. But if the state’s fiscal challenges are structural rather than temporary, policymakers will eventually face a more difficult question: should the focus be on finding new sources of revenue, or addressing the spending pressures that created the deficits in the first place?

Disclaimer: The views expressed in this article are solely those of the author and do not necessarily reflect the views of any employer, organisation, or affiliated entity.