In March 2016, Japanese ice cream manufacturer Akagi Nyugyo did something extraordinary.

For the first time in 25 years, the company raised the price of its popular Garigari-kun ice cream by just 10 yen—around six US cents.

Rather than quietly updating the price tag, the company’s executives appeared in a televised advertisement, bowed deeply and apologised to customers.

In almost any other country, a six-cent price increase would barely warrant a second thought.

In Japan, it became national news.

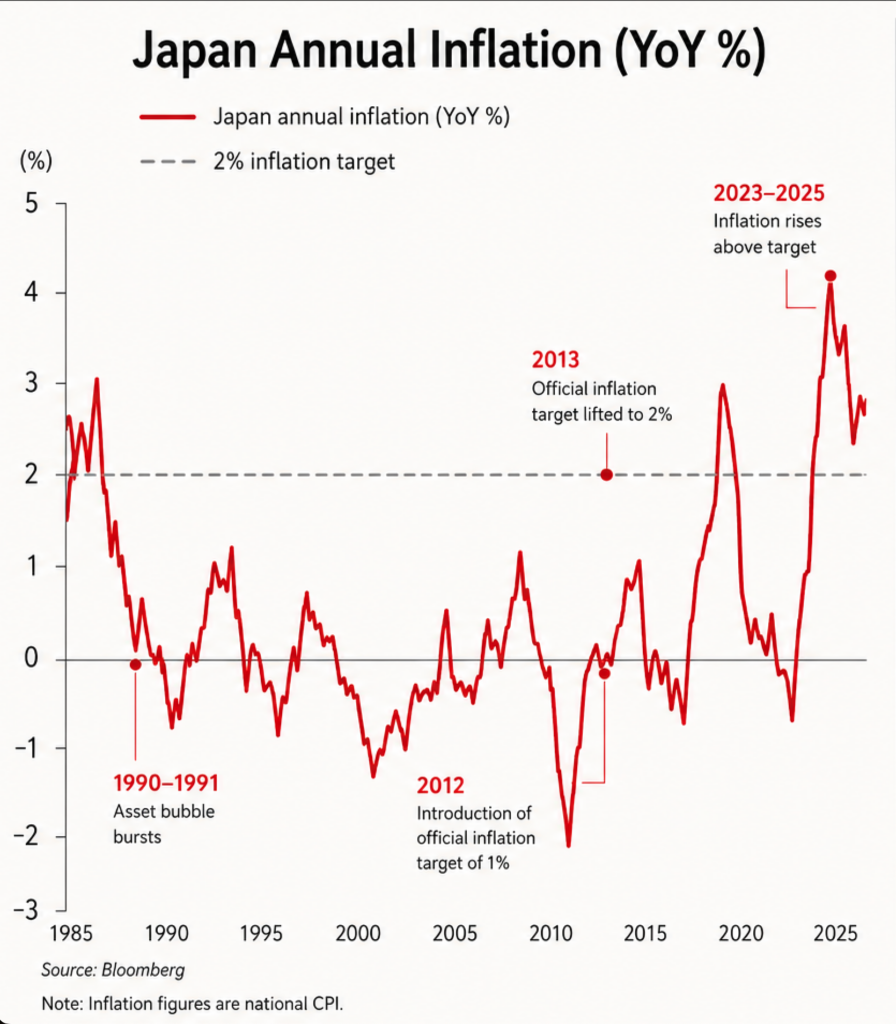

For over 30 years, inflation was virtually absent from the world’s previously second now fourth-largest economy. Consumers became accustomed to prices staying the same or even falling from one year to the next. Businesses hesitated to raise prices, workers rarely expected significant pay rises and deflation became deeply embedded in the country’s economic culture.

Today, that era is over.

A sharply weaker yen, supply chain disruptions following COVID and rising global energy prices have pushed inflation to levels Japan has not experienced for decades. Rice, groceries, electricity and transport have all become noticeably more expensive, forcing households and businesses to adapt to something many younger Japanese have never experienced before: a genuine cost-of-living crisis.

The irony is that this is exactly what policymakers and the BoJ had spent decades trying to achieve.

So how did Japan go from fighting deflation to fighting inflation? And can the world’s fourth economy learn to live with rising prices once again?

Japan’s Lost Decades

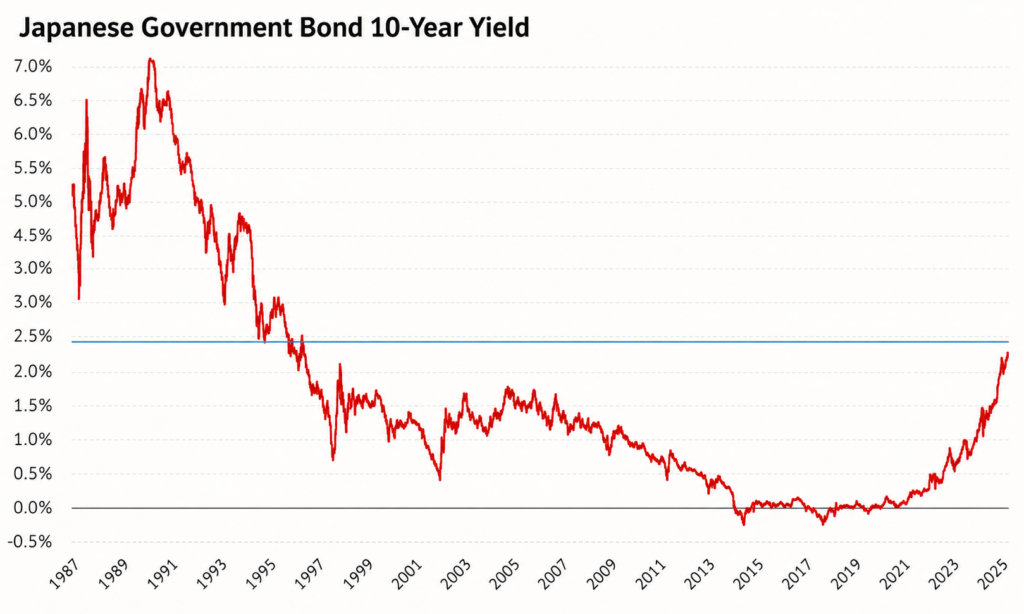

To understand Japan’s inflation story, you first have to rewind to the late 1980s.

At the time, Japan appeared unstoppable. Following decades of rapid industrialisation and export-led growth, it had become the world’s second-largest economy behind the US. Japanese companies dominated industries ranging from consumer electronics to automobiles, while many economists believed Japan would eventually overtake the United States as the world’s largest economy.

Behind the optimism, however, a dangerous asset bubble had formed.

Easy credit and speculation pushed stock prices and real estate valuations to extraordinary levels. At its peak in 1989, the land beneath Tokyo’s Imperial Palace was famously said to be worth more than the entire state of California.

The boom could not last forever.

As the bubble burst in the early 1990s, the stock market collapsed, property prices fell for more than a decade and businesses began aggressively cutting costs to survive. Banks were left holding enormous volumes of bad loans, investment slowed and consumer confidence deteriorated.

The economic consequences proved remarkably persistent.

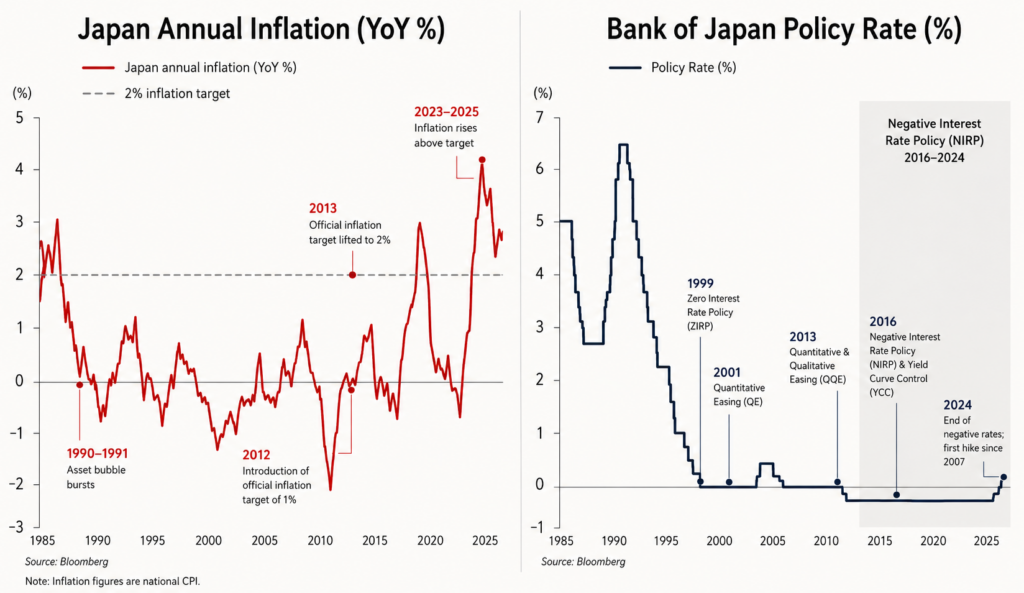

Instead of experiencing a sharp recession followed by a rapid recovery, Japan entered what became known as the “Lost Decades”, a prolonged period of weak economic growth, stagnant wages and deflation.

While lower prices may sound attractive to consumers, persistent deflation can become deeply damaging. If households expect prices to be lower in the future, they delay purchases. Businesses become reluctant to invest, companies avoid raising wages and economic activity gradually slows.

Breaking that cycle would become one of the BoJ’s greatest economic challenges over the next three decades.

The Bank of Japan’s Radical Experiment

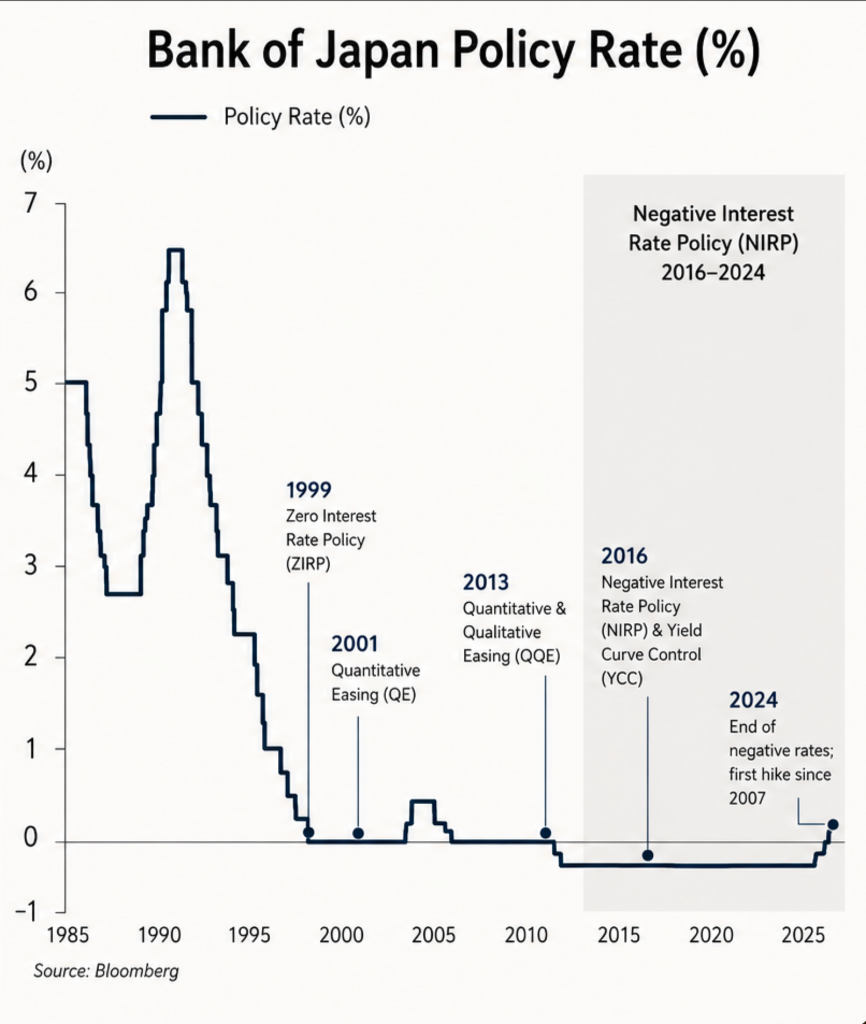

As Japan’s economy stagnated through the 1990s and early 2000s, the country’s central bank turned to increasingly unconventional policies in an effort to revive growth.

The BoJ steadily cut interest rates until they reached almost zero, making borrowing as cheap as possible in the hope that households would spend more and businesses would invest. When that failed to generate enough inflation, policymakers went even further.

Beginning in 2001 and dramatically expanding the program in 2013 under what became known as Quantitative and Qualitative Monetary Easing (QQE), the BoJ launched one of the largest quantitative easing programs ever attempted. Rather than simply lowering interest rates, the central bank created new money to purchase massive quantities of Japanese government bonds and other financial assets, including ETFs. The goal was to inject liquidity into the financial system, encourage lending, push investors towards riskier assets and finally lift inflation towards the 2% target.

The Bank also introduced negative interest rates in 2016 and adopted Yield Curve Control, a policy that kept long-term government borrowing costs artificially low by purchasing whatever quantity of government bonds was necessary to maintain its yield target. Together, these measures represented one of the most aggressive monetary policy experiments ever undertaken by a major central bank.

For years, however, effect of these policies weren’t as strong as policymakers expected. Though inflation exceeded 1% for the first time since the 90s, prices barely moved, wage growth remained subdued and inflation was still under the 2% target. While other central banks spent much of the 2010s trying to prevent inflation from rising too quickly, Japan was struggling to create any meaningful inflation at all.

Everything Changed

For years, the BoJ’s struggled to generate inflation.

Then, almost unexpectedly, it arrived.

The first catalyst came in 2020, when the COVID pandemic disrupted global supply chains and triggered a sharp increase in shipping costs, raw material prices and manufacturing bottlenecks. Businesses around the world suddenly faced higher costs for everything.

The second shock followed Russia’s invasion of Ukraine in 2022.

Global energy prices surged as oil and natural gas markets were thrown into turmoil as Russia faced sanctions. For a country that imports the vast majority of its energy, the impact was immediate. Higher import costs flowed through to electricity bills, transport costs and ultimately supermarket shelves. Japan wasn’t creating inflation at home; it was importing it from abroad.

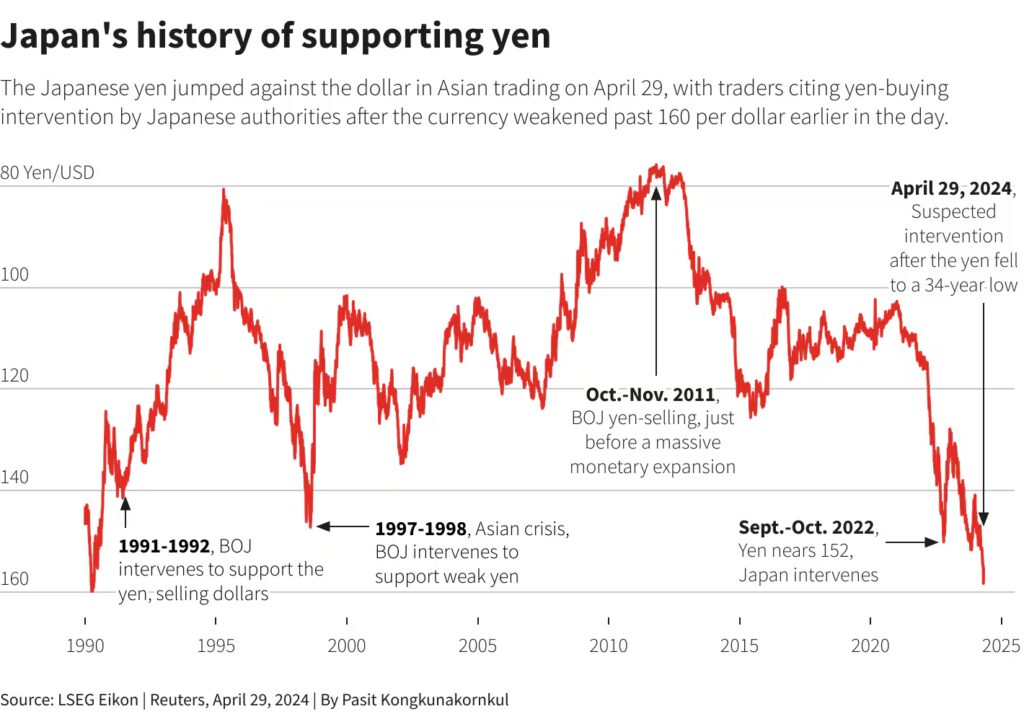

At the same time, the BoJ chose to maintain its ultra-loose monetary policy even as central banks like the Fed, ECB, RBA and elsewhere began rapidly raising interest rates.

The widening gap in interest rates caused the Japanese yen to weaken sharply against the US dollar, falling to levels not seen since the early 1990s. While a weaker currency benefits exporters by making Japanese goods cheaper overseas, it also makes imports weaker. Imported goods including food, fuel and raw materials more expensive.

The result was a dramatic shift in an economy that had become accustomed to stable prices.

Inflation exceeded the BoJ’s long-standing 2% target, reaching more than 4% in 2023. For the first time in decades, Japanese consumers were confronted with rapidly rising prices, forcing businesses to reconsider pricing strategies that had remained virtually unchanged for a generation.

Ironically, after spending more than 30 years trying to create inflation, Japan had finally succeeded.

The problem was that wages were struggling to keep pace.

Japan Wanted Inflation, Just Not Like This

At first glance, Japan’s return to inflation appears to be a success.

For decades, the BoJ had argued that moderate inflation was essential for a healthy economy. Rising prices encourage consumers to spend rather than delay purchases, businesses gain confidence to invest and workers have greater bargaining power to negotiate higher wages.

In theory, this creates a virtuous cycle.

Prices rise, wages increase, households spend more, businesses expand and economic growth strengthens.

But Japan’s recent inflation has been different.

Rather than being driven by strong consumer demand, investment and rising incomes, much of the price growth has been caused by higher import costs, a weaker yen and more expensive energy. As companies faced rising costs, many had little choice but to pass them on to consumers.

The problem is that wages have struggled to keep pace.

Although nominal wages have increased in recent years, inflation has risen faster, causing real wages to fall.

This helps explain why inflation, despite being a long-standing policy objective, has become politically unpopular.

For many households, it does not feel like economic recovery, instead like a cost-of-living crisis.

Japan’s Impossible Balancing Act

Japan’s inflation challenge has left policymakers facing a difficult trade-off.

On one hand, higher interest rates can help slow inflation by reducing borrowing and supporting the value of the yen. A stronger currency lowers the cost of imports, easing pressure on households and businesses that rely on overseas energy, food and raw materials.

On the other hand, raising interest rates creates a new problem.

Japan has the highest level of public debt in the developed world, with government debt exceeding 250% of GDP. After decades of ultra-low interest rates, even modest increases in borrowing costs can significantly raise the government’s interest bill. As debt servicing becomes more expensive, less money is available for other public priorities without higher taxes or additional borrowing.

This leaves the BoJ in a difficult position.

Move too slowly, and inflation could remain elevated while the yen continues to weaken.

Move too quickly, and higher borrowing costs could weigh on economic growth while placing greater pressure on the government’s already stretched finances.

In 2024, the BoJ ended its negative interest rate policy and later raised rates to their highest level in decades, signalling that the era of ultra-loose monetary policy was coming to an end.

But unlike many other central banks, Japan is not simply trying to bring inflation down.

It is trying to find the narrow path between ending decades of deflation without triggering another prolonged period of economic stagnation.

Can Japan Make Inflation Work?

For most developed economies, bringing inflation down is the primary objective.

Japan faces the opposite challenge.

After spending more than three decades battling deflation, policymakers are now attempting to preserve the benefits of moderate inflation while preventing it from becoming a prolonged cost-of-living crisis.

The key lies in wages.

If salaries continue to rise alongside prices, households should gradually regain purchasing power, consumer spending could strengthen and the economy may finally enter the virtuous cycle the Bank of Japan has pursued for decades.

If wages fail to keep pace, however, inflation will continue to erode living standards and place increasing pressure on households, businesses and policymakers alike.

There are encouraging signs.

Japan’s largest companies have agreed to some of the strongest wage increases in decades, corporate profits remain resilient and the country’s stock market has reached record highs as investors become more optimistic about Japan’s long-term prospects.

Whether that momentum spreads across the broader economy, particularly to smaller businesses that employ the majority of Japanese workers, remains one of the country’s biggest economic questions.

The irony is difficult to ignore.

For decades, Japan searched for inflation but could never quite create it.

Now that inflation has finally returned, the challenge is no longer creating it.

It is learning how to live with it.