After years of underwhelming performance, hedge funds are undergoing a meaningful revival, with 2025 and early 2026 representing their most robust period of alpha generation since the rebound following the Global Financial Crisis. A range of independent industry surveys indicates that hedge funds are once again producing double-digit returns, benefiting from renewed allocator confidence and a broader shift toward market conditions that favour active management outperformance.

- A Structural Break From the QE Era

- The “Reset” That Bolstered Alpha

- Double‑Digit Returns and Real Alpha

- Why Alpha Is Back

- Higher volatility and dispersion

- Crowded-trade unwinds are creating fresh opportunity

- Rising interest rates have restored the economics of shorting

- The investable universe has expanded significantly

- Institutional demand and new fund formation are both accelerating

- Conclusion

- Disclaimer

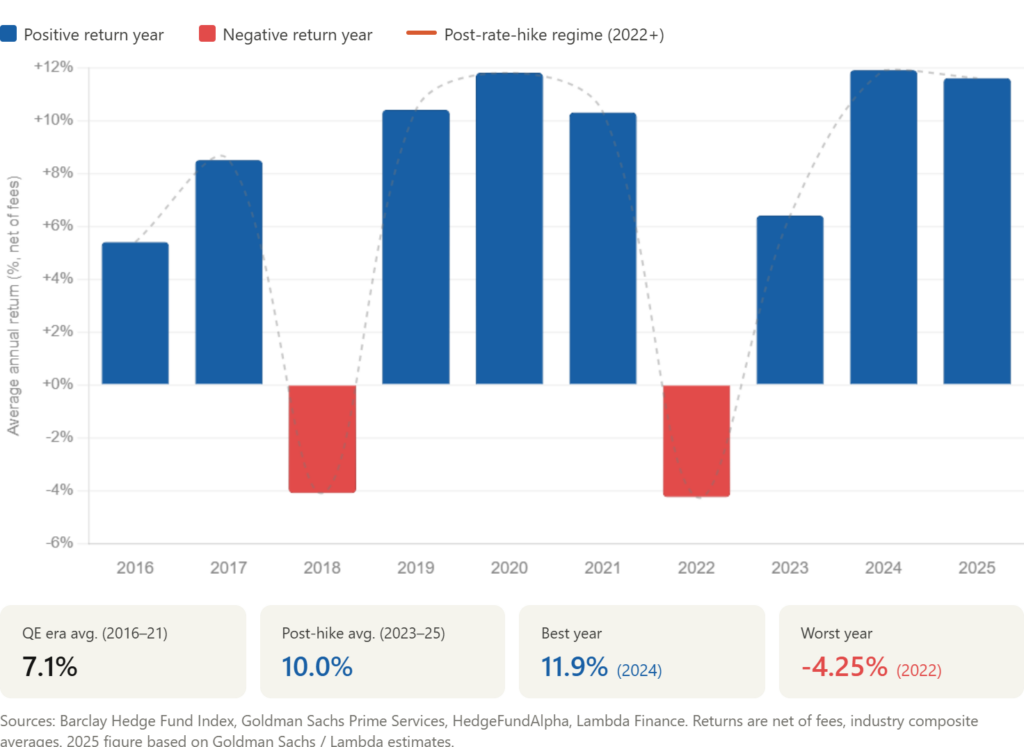

A Structural Break From the QE Era

For much of the 2010s, hedge funds found themselves in a difficult environment. Ultra-low interest rates, central bank liquidity injections, and broadly synchronised market rallies suppressed dispersion and compressed correlations, conditions that made generating stock-specific alpha exceptionally challenging. As Goldman Sachs has observed, the QE era’s persistently low rates muted hedge fund alpha generation, with many strategies producing returns that were largely indistinguishable from plain beta exposure.

The macro backdrop has since changed materially. The U.S. rate-hiking cycle, elevated inflation volatility, and rolling sector rotations have collectively widened the opportunity set for relative-value strategies, allowing skilled managers to reassert a meaningful performance edge.

The “Reset” That Bolstered Alpha

A pivotal inflection point arrived in March 2026, when a sharp and disorderly repricing swept across global markets, driven by rate volatility, sector rotation, and the unwinding of crowded positions, producing what hedge fund managers have termed a “violent reset.” That reset effectively restored the conditions in which hedge funds have historically thrived: elevated dispersion, lower cross-asset correlations, widespread mispricing across sectors, and a level of volatility that rewards disciplined, active risk-taking.

Analysts at HedgeCo also confirm this as April 2026 is on course to be the strongest month for long-short equity in nearly a decade, with the strategy posting gains of approximately 7.7%. For the first time in several years, markets have become sufficiently inefficient for skilled active managers to exploit in a meaningful way.

Double‑Digit Returns and Real Alpha

The outperformance has been broad-based rather than concentrated in a handful of strategies. Discretionary equity led the way with returns of 17.1% and alpha of 5.7%, while quantitative equity produced 5.8% alpha, consistent with its post-2020 trend. Market-neutral and low-beta strategies added further depth, generating alpha in excess of 8.5%. Taken together, this across-the-board strength points to a genuine industry-wide resurgence, not a narrow rally driven by isolated pockets of the market. Institutional allocators are taking notice, and acting on it. According to Goldman Sachs, 91% report that their hedge fund portfolios met or exceeded expectations, while nearly half plan to increase their allocations in 2026, the highest proportion ever recorded.

Why Alpha Is Back

Higher volatility and dispersion

Has returned the market conditions that historically underpin alpha generation. Stock-to-stock correlations are lower, sector performance is increasingly divergent, and macro uncertainty continues to persist. It seems that the current environment closely resembles the 2000s, one of the most productive decades on record for hedge fund alpha.

Crowded-trade unwinds are creating fresh opportunity

The March 2026 reset forced broad deleveraging across AI-related mega-cap positions, producing mispriced assets and compelling new entry points for long-short managers willing to act quickly.

Rising interest rates have restored the economics of shorting

Short books now generate meaningful carry once again, materially improving the return profile of long-short strategies that were structurally disadvantaged during the near-zero rate era.

The investable universe has expanded significantly

Global equity and bond markets have grown considerably faster than hedge fund AUM over the past decade, meaning the industry is not running into capacity constraints, a structural tailwind for future alpha generation.

Institutional demand and new fund formation are both accelerating

With intelligence reports that 2026 is on track for the strongest inflows since 2017, with 344 new funds currently in development, there is a further signal that the broader ecosystem is in good health.

Conclusion

The evidence is compelling: alpha has made a decisive comeback, and hedge funds are flourishing in a way not seen since the early 2000s. The confluence of sustained macro volatility, widening sector dispersion, and a sweeping reset across crowded trades has created an environment in which active management can genuinely thrive. If these conditions endure, and the weight of allocator conviction suggests they will, then 2026 may well mark the opening chapter of a multi-year renaissance in hedge fund performance, capital inflows, and industry-wide growth.

Disclaimer

The Investor Standard provides general information for education and research only. It is NOT personal advice, a recommendation, or an offer to buy/sell any security. This content has been prepared without taking into account your objectives, financial situation or needs. Past performance is not indicative of future results. Before acting on any information, consider its appropriateness and seek independent advice from a licensed financial adviser.