SpaceX is preparing for what could become the largest IPO ever.

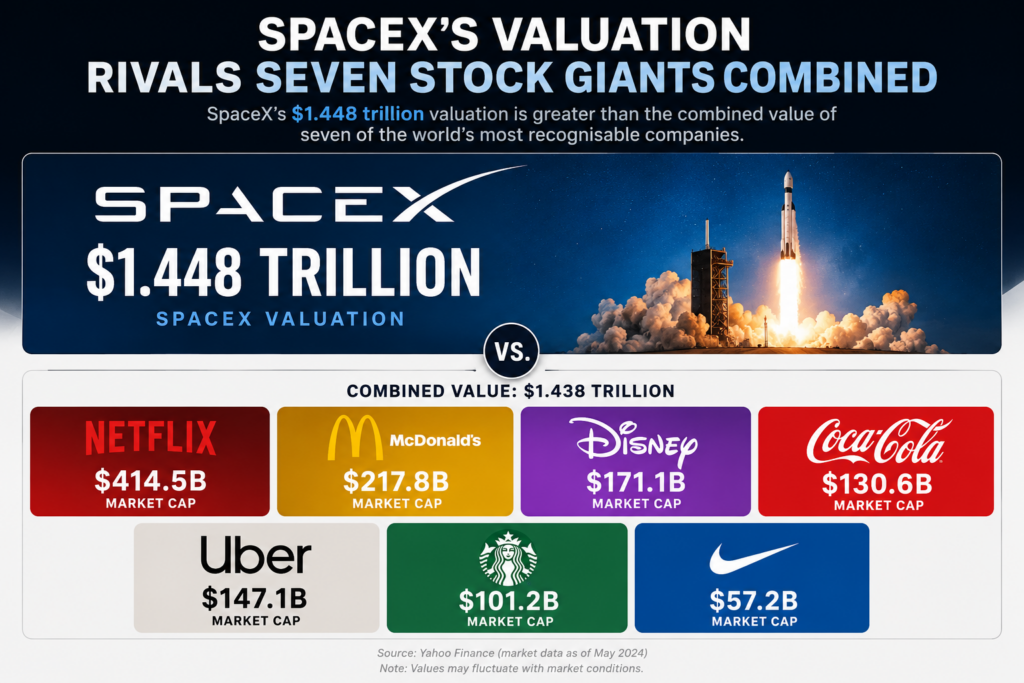

At a reported valuation of US$1.75 trillion and an expected raise of up to US$75 billion, the listing would dwarf Saudi Aramco’s record-breaking IPO and instantly become one of the most valuable companies on Earth.

Yet the significance of the SpaceX IPO extends far beyond rockets.

The listing represents a test of modern capital markets, investor appetite for ambitious growth stories and the increasingly blurred line between investing in a business and investing in a vision.

For decades, IPOs served a relatively straightforward purpose. Companies raised capital from public investors in exchange for ownership, using the proceeds to fund expansion and growth. Today, however, private capital markets have become so deep that many firms can and do remain private for far longer than in previous generations.

SpaceX is perhaps the most extreme example of this trend.

Founded in 2002, the company spent over 2 decades building rockets, launching satellites and developing one of the world’s largest broadband networks without ever accessing public markets. During that time, it raised billions of dollars from private investors while growing into a company generating more than US$18 billion in annual revenue.

Now, after years of insisting that SpaceX would remain private, Elon Musk appears ready to take the company public.

The question is why.

Why Is SpaceX Going Public Now?

Historically, Musk has argued that the long-term nature of SpaceX’s mission made public ownership undesirable.

Developing reusable rockets, building satellite constellations and pursuing interplanetary travel requires enormous capital investment and long development timelines. Public markets, by contrast, often reward short-term financial performance and quarterly earnings growth.

That logic appears to have changed.

SpaceX’s ambitions have expanded beyond rockets and satellites. The company is increasingly positioning itself as an AI infrastructure business, exploring the construction of data centres and computing capacity required to support future AI development after it acquired XAi earlier in February.

These ambitions come with an enormous price tag.

While SpaceX’s existing businesses generate substantial revenue, building global AI infrastructure, expanding Starlink and continuing Starship development could require tens of billions of dollars in additional capital. Public markets provide access to a pool of funding that even private investors may struggle to match.

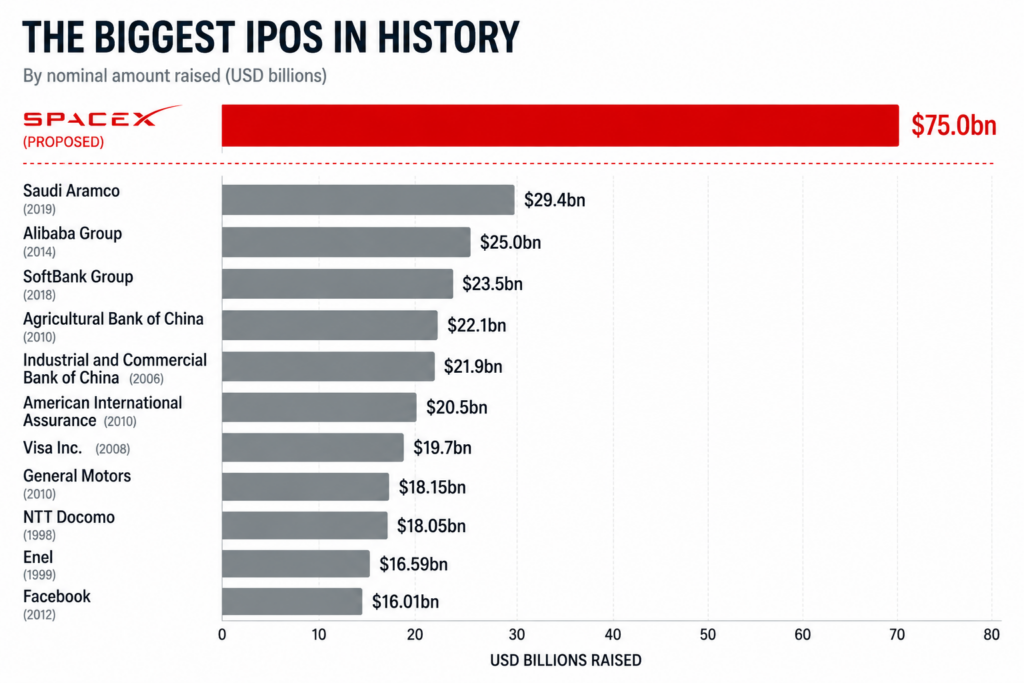

The Biggest IPO In History

The scale of the proposed SpaceX listing is difficult to comprehend.

The company is reportedly seeking a valuation of approximately US$1.75 trillion while raising as much as US$75 billion through its IPO. If completed, the listing would comfortably surpass Saudi Aramco’s US$29.4 billion IPO in 2019, currently the IPO in history.

The sheer size of the transaction highlights how dramatically markets have changed over the past 20 years.

Traditionally, companies went public much earlier in their development. Firms would often list while still relatively small, using public markets to fund future growth. Today, many companies remain private for years longer, raising capital from venture capital firms, private equity funds, sovereign wealth funds, private credit and institutional investors.

As a result, companies increasingly arrive on public markets already worth hundreds of billions of dollars.

SpaceX represents the ultimate example of this trend. Rather than going public as a growing company, it’s going public as already one of the largest companies in the world.

This shift raises an important question for investors: if much of the company’s growth has already occurred while private, how much upside remains for shareholders?

The Valuation Problem

While the size of the IPO is remarkable, the valuation is where the debate becomes far more contentious.

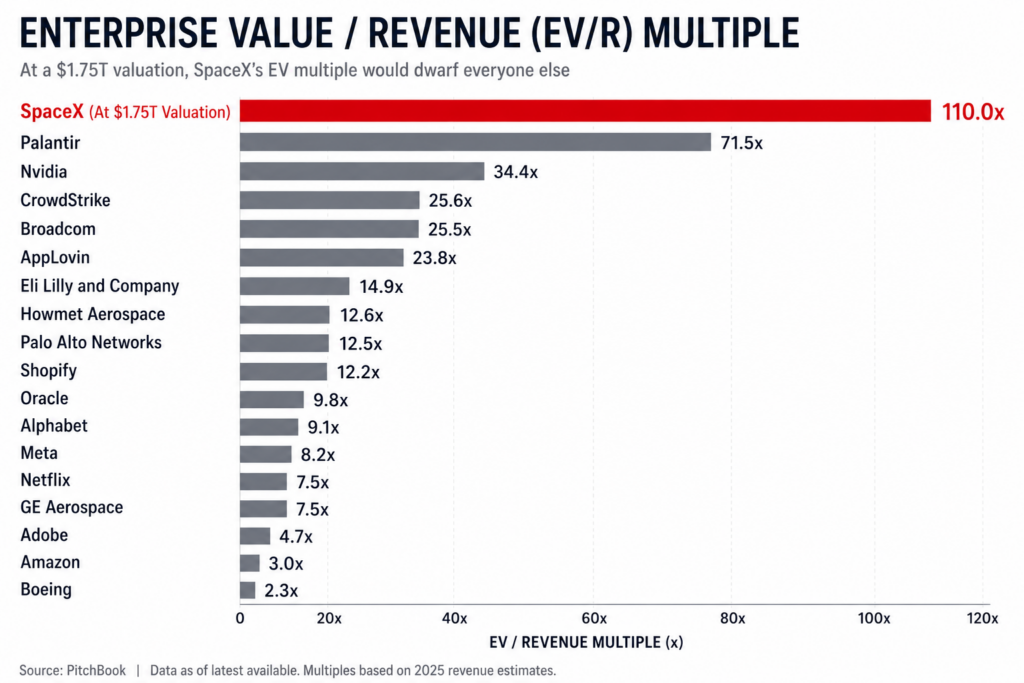

SpaceX generated approximately US$18.5 billion in revenue during 2025 and is projected to generate between US$22 billion and US$24 billion in the coming year.

At a US$1.75 trillion valuation, investors would be valuing the company at roughly 87 times annual revenue. By comparison, some of the market’s most highly valued technology companies, including Nvidia and Tesla, trade at revenue multiples closer to 15 times sales.

Viewed through traditional valuation metrics, the numbers appear extraordinary.

The discrepancy highlights a crucial reality: investors are not valuing SpaceX based solely on its current earnings power.

They are valuing what they believe the company could become.

Supporters point to Starlink’s dominance in satellite broadband, SpaceX’s leadership in commercial launch services and the potential of Starship to dramatically reduce the cost of access to space. More ambitious investors see future opportunities in global communications networks, defence contracts, lunar missions, Mars colonisation and artificial intelligence infrastructure.

Critics counter that much of this value remains speculative. While Starlink and launch services are established businesses, many of the company’s most ambitious projects remain years away from commercial viability.

The result is a valuation that depends as much on future possibilities as present realities.

Starlink: The Real Business

Much of the hype and talk surrounding SpaceX focuses on Mars colonisation, Starship and futuristic technologies. However, the company’s most important business today is far more grounded.

It’s Starlink.

Starlink is a satellite broadband network consisting of thousands of satellites operating in low-Earth orbit. The service provides internet access to households, businesses, governments and remote communities across the world, including areas where traditional broadband infrastructure is either unavailable or prohibitively expensive.

Over the past several years, Starlink has evolved from an experimental project into one of the largest satellite operators in the world. The business now generates billions of dollars in recurring revenue and has become a critical source of cash flow for SpaceX.

Unlike many of the company’s long-term ambitions, Starlink is not a speculative future opportunity. It is an operating business with paying customers, reliable profits and cash flow, established infrastructure and significant barriers to entry.

While investors often associate SpaceX with rockets, launch services alone may not justify a multi-trillion-dollar valuation. Starlink, however, provides a scalable and recurring revenue stream that more closely resembles a telecommunications company than an aerospace contractor.

For many investors, Starlink is the foundation upon which the broader SpaceX investment case rests.

Without Starlink, the valuation would largely depend on technologies that remain years from commercialisation. With Starlink, investors can at least point to a dominant business generating substantial revenue today while helping finance the company’s more ambitious projects.

Investors Are Buying The Dream

The challenge with valuing SpaceX is that much of its potential lies in businesses that do not yet fully exist.

Investors are not simply purchasing exposure to satellite broadband or launch services. They are buying into a vision of what SpaceX could become over the coming decades.

That vision is both exciting and terrifying.

Supporters argue that SpaceX has already transformed the economics of spaceflight through reusable rockets, built the world’s largest satellite internet constellation and established itself as the dominant player in commercial launch services. If the company could achieve those milestones, they argue, it would be foolish to dismiss its future plans.

Many of those plan remain highly speculative.

Starship, SpaceX’s next-generation launch vehicle, is designed to be fully reusable and dramatically reduce the cost of access to space. The rocket is central to many of the company’s long-term plans, including lunar missions, large-scale satellite deployment and eventually human settlement on Mars.

However, Starship remains under development and has experienced several high-profile failures during testing. Most recently, a vehicle exploded during preparations for a ground test, highlighting both the complexity and risks associated with the programme.

Beyond spaceflight, investors are increasingly focused on another opportunity: artificial intelligence.

Reports suggest SpaceX is exploring the development of AI infrastructure and data centres, potentially leveraging its broader ecosystem alongside xAI. If successful, this could position the company to benefit from one of the fastest-growing sectors in the global economy.

The result is a valuation that relies heavily on future possibilities.

Bulls see a company that could dominate multiple trillion-dollar industries. Bears see a valuation that already assumes much of that success has occurred.

In many ways, the SpaceX IPO is less a bet on current financial performance and more a bet on Elon Musk’s ability to turn science fiction into reality.

Why The IPO Matters Beyond SpaceX

The significance of the SpaceX IPO extends far beyond a single company.

In many respects, the listing represents the culmination of a broader transformation that has been taking place across capital markets for decades.

Historically, fast-growing companies usually went public relatively early in their development. Public markets provided access to capital, while investors gained the opportunity to participate in a company’s growth journey from an earlier stage. A sort of “shareholder democracy.”

Today, that model has changed.

The growth of venture capital, private equity, sovereign wealth funds and institutional private markets has allowed companies to remain private for much longer. Rather than listing at valuations of hundreds of millions or a few billion dollars, many firms now wait until they are worth tens or even hundreds of billions before accessing public markets and in this case over a trillion.

SpaceX represents the most extreme example of this trend.

Instead of entering public markets as a growth company, it is entering as a potential multi-trillion-dollar giant.

This shift raises important questions for investors.

If companies spend most of their highest-growth years in private markets, public investors may increasingly be left purchasing mature businesses at significantly higher valuations. The traditional pathway where retail investors could participate in a company’s early growth may become increasingly rare.

SpaceX is unlikely to be the last example.

Companies such as OpenAI and Anthropic have already reached valuations that would have been unimaginable for private businesses just a decade ago. If current trends continue, future IPOs may increasingly resemble the SpaceX listing: massive companies entering public markets at enormous valuations with global investor attention.

The SpaceX IPO therefore represents more than a milestone for Elon Musk. It may provide a glimpse into what the future of public markets looks like.

Bubble Or Revolution?

Whether the IPO proves successful depends on whether investors are paying for what the company is today, or what they believe it could become.

Bull Case

SpaceX has already achieved what many considered impossible. It revolutionised rocket launches through reusable launch vehicles, built the world’s largest satellite broadband network and established itself as the dominant player in commercial spaceflight. Few companies can point to such a transformative track record.

Supporters argue that betting against Elon Musk’s ambitions has historically been an expensive mistake. Tesla was once dismissed as a niche electric vehicle manufacturer. SpaceX itself was repeatedly written off during its early years. In both cases, the company ultimately exceeded expectations.

From this perspective, today’s valuation reflects the possibility that SpaceX could eventually dominate multiple industries simultaneously, including satellite communications, launch services, artificial intelligence infrastructure and perhaps even entirely new markets that do not yet exist.

Bear Case

At roughly 87x annual revenue, SpaceX trades at a valuation far above even the most richly valued technology companies. Much of the investment thesis relies on projects that remain years away from commercial viability, while some of the company’s most ambitious initiatives continue to face significant technological and operational risks.

Starship remains under development. AI infrastructure ambitions remain largely conceptual. Mars colonisation remains firmly in the realm of long-term aspiration.

Critics therefore argue that investors may be paying today’s prices for tomorrow’s success.

Ultimately, the SpaceX IPO represents one of the largest and most ambitious bets in financial history.

If SpaceX successfully executes on even a portion of its long-term vision, today’s valuation may one day appear conservative. If those ambitions fail to materialise, the IPO may instead serve as a reminder that even the most revolutionary companies are not immune to the laws of valuation.

For now, investors face a choice.

They can focus on the company’s current financials and conclude the valuation is hard to justify.

Or they can do what many SpaceX investors have done for more than two decades: bet that Elon Musk will once again achieve what others consider impossible.