What actually happened

On 12 June 2026, Monash IVF (ASX:MVF) told the market it now expects FY26 underlying net profit of A$17m to A$18m. That is down from the A$20m it reaffirmed at the half-year in February, and from the A$20-23m it set at the FY25 result last August. Three guidance points, each lower than the last. The cause was the same each time: Australians are starting fewer IVF cycles. Stimulated cycle volumes across the market fell 4.7% on a rolling three-month basis to the end of April.

The reaction did not match the words. Monash IVF shares rose 2.2% to A$0.68 on the day and have since drifted to around A$0.73 (17 Jun 2026). A roughly 12-15% cut to forecast profit, met with a green candle. The first job of an earnings reaction note is to explain that gap, because the gap is where the information sits.

Read the announcement past the headline and two things sit side by side. Profit guidance fell. Market share rose a full point to 20.1%, with international operations still growing. Monash is taking share while the pool shrinks. A buyer of a fertility network does not pay for one soft year of cycle volumes. It pays for the clinics, the doctors, the brand and the position in a consolidating market. That asset got better in June, not worse.

What the market may be missing

Start with the corporate history, because it sets the floor everyone is half-assuming. In November 2025 a consortium of Genesis Capital, a healthcare-focused private equity firm, and Washington H. Soul Pattinson (ASX:SOL) lobbed an indicative 80 cents a share, valuing Monash at about A$311.7m. The board rejected it as opportunistic. In April 2026 the same pair came back at 90 cents, around A$350m. The board rejected that too, and the consortium withdrew on 20 April.

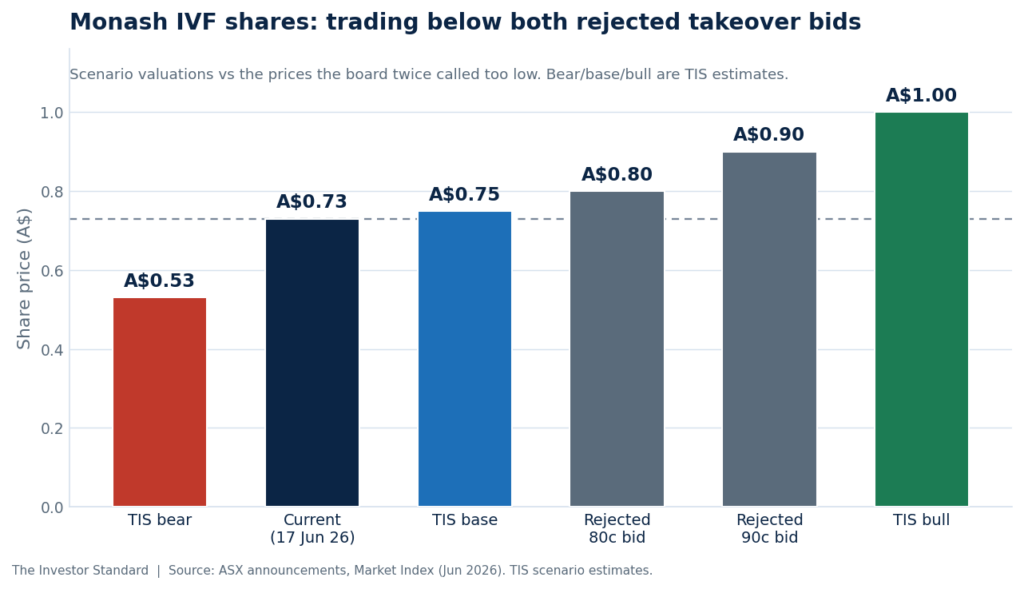

So the stock now trades at A$0.73, below the 80c the board waved away and well below the 90c it called inadequate. The market is not pricing in a bid. It is pricing in the absence of one. That is the disconnect. Specialist money looked at this business twice, with full diligence access, and decided it was worth at least 90 cents. The earnings have softened since, but the share count, the clinics and the 20.1% share have not evaporated. If you believed the board in April, the stock is now cheaper than the price it said was too low.

The precedent matters here. When Australia’s other listed fertility group, Virtus Health, went into play in 2022, it drew a bidding war between BGH Capital and CapVest and was taken private at around A$8 a share, valuing it near A$683.5m. Australian IVF assets get bought, and they get bought in contested processes. Monash is the larger of the two networks that remain. The market is treating a withdrawn bid as the end of the story. The sector’s history says it is more often an interval.

The numbers

The reported figures are not pretty, and pretending otherwise would miss the point. The first half of FY26 (to 31 Dec 2025) showed revenue of A$137.9m, down 1.8%, and underlying EBITDA of A$30.2m, down 15.3%. The margin fell 3.5 points to 22.0%. Underlying NPAT dropped 34% to A$10.4m. This is operating deleverage in action: when a fixed-cost clinic network sees volume dip, profit falls faster than revenue.

| Metric | 1H26 31 Dec 2025 |

vs 1H25 | FY25 Full year |

|---|---|---|---|

| Revenue | A$137.9m | -1.8% | A$271.9m (+6.7%) |

| Underlying EBITDA | A$30.2m | -15.3% | A$66.3m (+5.6%) |

| Underlying EBITDA margin | 22.0% | -3.5pp | 24.4% |

| Underlying NPAT | A$10.4m | -34.0% | A$27.4m (-8.1%) |

| Reported NPAT | A$7.5m | -56.4% | A$25.7m |

| Free cash flow | A$5.0m | vs -A$6.2m | n/a |

| Net debt | ~A$95m (~2.0x) | n/a | n/a |

Source: Monash IVF 1H26 results, 26 February 2026, and FY25 results, 22 August 2025, for the year ended 30 June 2025. Underlying figures are as reported by the company.

Now the valuation, anchored on the post-downgrade picture. At A$0.73 across roughly 389.6m shares, the market cap is about A$284m. Add net debt of around A$95m (31 Dec 2025, which the company expects to be similar at June year-end) and enterprise value is roughly A$379m. The full year underlying NPAT guide of A$17-18m implies forward earnings of about 4.5 cents a share, so the stock is on roughly 16 times forward earnings. On the headline P/E, it is not cheap. That is the optical trap that keeps casual buyers away.

The picture flips on cash earnings. We estimate FY26 underlying EBITDA near A$57m (our estimate, bridging the first-half A$30.2m to the lowered full-year profit guide; the company did not guide to an EBITDA figure). That puts the enterprise on about 6.6 times forward EBITDA, and on the FY25 actual of A$66.3m, about 5.7 times. The 80c bid implied roughly 7.1 times our FY26 estimate; the 90c bid about 7.8 times. The board characterised the first approach at around 7.7 times. Whichever base you use, the current price sits a clear step below where two buyers were willing to transact.

Re-basing the cases on the result gives a clear shape. The bear sits near A$0.53: cycle volumes keep falling, the multiple compresses toward 5.5 times a lower FY27 EBITDA, no bidder returns, and the stock drifts back to its 52-week low. The base lands near A$0.75, roughly where it trades: the market clears Monash at about 6.5 times forward EBITDA as a fairly-valued standalone earner, with the takeover optionality worth little until proven. The bull reaches about A$1.00: FY27 efficiency programs and a volume recovery lift EBITDA back toward A$66m, the market pays a control-style 7.5 times, or a fresh bid simply arrives at or above the rejected 90c. Current price A$0.73. The downside cushion is thin at around 27%; the upside on a re-rate or a bid is roughly 37%.

Catalysts & Risks

FY26 full-year result on 24 August 2026. The market needs the A$17–18m guidance to hold and a credible FY27 bridge from the efficiency program. A renewed approach from Genesis or another buyer would reset the whole frame.

A turn in Australian cycle volumes, continued market-share gains above 20%, and a return to dividends, which the company has tied to hitting its targets. Net debt moving below 2x would widen the strategic buyer pool.

Guidance has now been cut three times, so management’s forecasting credibility is thin. Leverage near 2x EBITDA and no dividend leave little room if volumes fall further.

Margins are sliding, and share gains in a price-competitive, shrinking market can come at the expense of profitability. Reputational risk from the 2025 embryo incidents also remains.

The bidders have already walked once. There is no guarantee another offer arrives, and a value trap that keeps downgrading remains a realistic outcome.

Investor takeaway

The market read the cut correctly on the day and for a reason most commentary missed. A 12-15% profit downgrade that lifts the share price is the market telling you it has repriced Monash IVF from an earnings stock to a special situation. The value no longer rests on this year’s profit. It rests on a share-gaining clinic network that two buyers chased to 90 cents, now available at 73, in a sector with a live take-private precedent. That is a coherent reason to look, not a reason to chase.

Treat it as what it is: an asset-and-optionality call, not a recovering-earnings call. The thesis strengthens if the 24 August result holds the line and the efficiency program shows up in FY27 numbers, or if a bidder reappears. It breaks if cycle volumes keep sliding, margins keep leaking, and the board’s twice-stated belief that the company is worth more than 90 cents quietly becomes a story shareholders tell themselves while the price grinds lower. The calm on 12 June was rational. Whether it proves right depends entirely on the next two prints.