The ASX 200 added roughly 3% last week and futures pointed higher again on Monday, with the market leaning on hopes the Middle East tension is easing. That is the index story. Underneath it, four ASX stocks to watch carry catalysts of their own this week, and in each case the obvious read is not the interesting one.

This is a heavy week for catalysts. The Reserve Bank hands down its cash-rate decision on Tuesday afternoon with the rate sitting at 4.35% after three increases this year. An activist campaign at the country’s biggest gold miner escalated over the weekend. Iron ore is wrestling with the US$100 line as new supply floods in. And the June index rebalance forces passive money into a clutch of new names on 22 June. Here is the scorecard before we take each one apart.

| Stock | The catalyst this week | What the market may be underrating |

|---|---|---|

| CBA Commonwealth Bank | RBA decision, Tue 16 Jun | The de-rating has already started; the rate call is the sideshow. |

| NST Northern Star | Elliott’s push for a strategic review | A break-up or bid is barely in the price. |

| FMG Fortescue | Iron ore testing US$100 on Simandou supply | It trades above the price the analysts give it. |

| EOS Electro Optic Systems | Joins the ASX 200 on 22 Jun | Inclusion day is often the top, not the launch. |

Commonwealth Bank: the RBA day that gets framed wrong

Every desk will trade CBA off the 2:30pm AEST decision on Tuesday. The cash rate is 4.35% after a third hike on 5 May, and the debate is whether the Bank pauses or goes again. NAB told clients on 9 June it now has “greater conviction that the next move in rates is down,” which tells you the hiking cycle is closer to its end than its start.

The framing everyone reaches for is margins: higher rates, fatter net interest margins, good for banks. That misses what the CBA share price has actually done. The stock changes hands near A$160 (12 Jun 2026), down from a 52-week high of A$192, a fall of roughly 17% while the cash rate kept climbing. So the rate-hike-equals-bank-bull reflex is already broken on the tape. CBA still trades around 28 times earnings, the richest multiple of any major bank in the world, on a dividend yield near 3%. That is a valuation built for a world of falling rates and scarcity of yield. As the RBA pushed the other way, the premium started leaking out. The decision that matters on Tuesday is not what it does to margins. It is whether a pause, or a dovish shift in the language, slows the unwind of the most expensive bank multiple on the planet. A hold could relieve CBA more than another hike would hurt it.

Northern Star: gold near records, and the miner that missed it

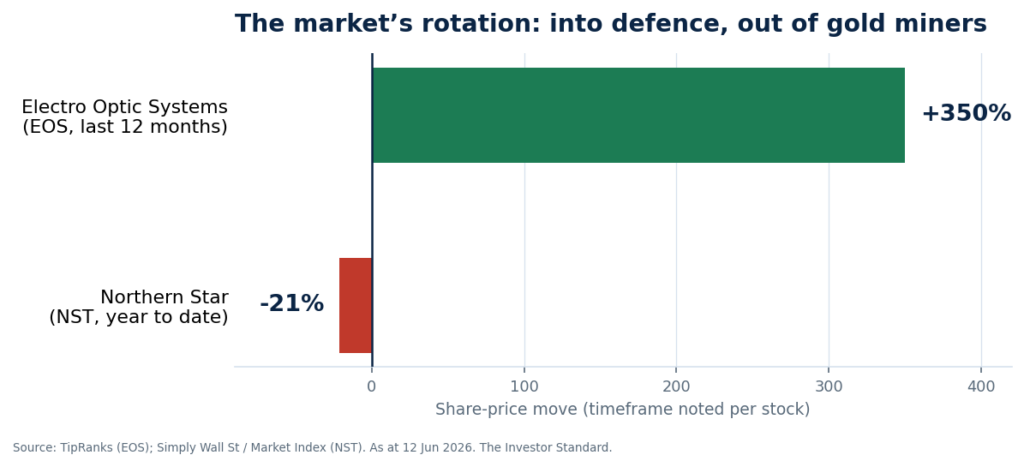

Gold has spent the year near record levels. Northern Star, the largest gold producer on the ASX, is down about 21% year to date at A$19.26 (mid-Jun 2026). That gap is the whole story. Over the past 12 months the stock has lagged the gold miners index by roughly 70 percentage points, an extraordinary miss in a bull market for the metal it digs up.

Elliott Investment Management has noticed. The activist escalated its campaign on 10 to 11 June, demanding a formal strategic review, a substantially strengthened board and a search for a “world-class CEO,” and pointing to seven outlook misses in four years. Northern Star has acknowledged operational problems but rejected calls for an immediate sale. The market is reading the share price as a gold story. Elliott is reading it as a governance and cost-control story, and the numbers back the activist: FY26 all-in sustaining cost guidance of A$2,300 to A$2,700 an ounce is high enough to swallow much of the gold-price tailwind. The second-order point is what a strategic review does to the asset base. A serious process puts Northern Star’s best mines in play, and prior takeover approaches have already been disclosed. Activist campaigns at ASX large caps are rare and they seldom end quietly. Very little of a break-up or a bid is in the current price.

Fortescue: trading above the people paid to value it

Iron ore is the quiet pressure point. The benchmark slipped to about US$101.65 a tonne in early June, a two-month low, as exports from the giant Simandou mine in Guinea jumped to 2.2 million tonnes in May from a record 1.3 million in April. That is new supply landing into a market already hovering at US$100. Fortescue is the purest iron-ore play among the majors, so it wears the price more directly than BHP or Rio.

Here is the oddity. Fortescue trades at A$20.64 (15 Jun 2026), above the analyst consensus target of A$19.34. The market is more bullish than the brokers who cover it, which is the reverse of the usual setup. The bull case rests on the dividend, with UBS pencilling in a FY26 payout near A$1.22 a share, around 7% grossed up for franking. The risk the market is underrating is supply, not demand. Simandou is not a one-off shipment; it is the front edge of a structural wall of tonnes aimed at the same Chinese steel mills. If iron ore drifts toward US$90, the dividend that anchors the register thins, and a stock already trading through its target has the furthest to fall. Income holders should watch the ore price, not the yield headline.

Electro Optic Systems: the index buy everyone can see coming

Electro Optic Systems joins the S&P/ASX 200 in the rebalance effective 22 June, alongside four other names. The defence and space-technology group, which builds directed-energy weapons and space-debris tracking systems, has run roughly 350% over the past year to a market value near A$2.3 billion. Index inclusion forces tracker funds to buy, which sounds like a guaranteed tailwind.

It is not free money, and the reason is timing. The inclusion was announced well ahead of the effective date, so active investors front-run the passive flows rather than waiting to be run over by them. Across markets, inclusion day often marks where the easy gains stop, not where they start. The real question for EOS is whether a defence re-rating at this valuation holds once the forced buying clears and the stock has to stand on orders and cash flow. The most recent broker rating sits at Buy with a A$14.00 target, so there is a case here, but treat the index event as a known catalyst, not an edge. The edge, if there is one, is in the earnings that have to follow the re-rate.

What to watch and in what order

Tuesday at 2:30pm AEST is the fixed point: the RBA decision and, just as important, the tone of the statement set the read on CBA and every rate-sensitive name. Through the week, watch for any board movement or fresh exchange between Elliott and Northern Star, since a concession on the review would move the stock before any deal is struck. Iron ore prints and Simandou shipment data are the live feed for Fortescue. Then 22 June brings the index rebalance, when EOS formally enters and the passive bid arrives on cue.

Investor Takeaway

The thread running through all four is the same. The visible catalyst (the cash-rate call, the gold price, the index buy) is priced and obvious. The move that matters sits one step behind it: a valuation unwind at CBA that a pause could ease, a governance unlock at Northern Star the share price ignores, a supply wall that threatens Fortescue’s dividend more than demand does, and a post-inclusion test for EOS once the forced buying is done. None of this is a recommendation to act, just where to point attention when the headlines hit. If CBA rallies on a pause rather than a hike, if Northern Star firms on review news rather than the gold price, if Fortescue cracks on supply rather than China demand, the framing here is working. If not, the obvious story was the right one after all.

Disclaimer: This article is general information only and does not constitute financial advice, personal investment advice, or a recommendation to buy, hold or sell any security. Share prices and figures are as at the dates shown and move constantly. Investors should conduct their own research and consider their personal circumstances before making investment decisions.