Days after NOVONIX delivered the most important sample in its history, NOVONIX share price fell about 25 percent. The company did both to itself, and the order matters more than the headline. A falling price tells you the tape moved. It does not tell you why, and the why is the whole game.

Market context: a hawkish Fed and three different sell-offs

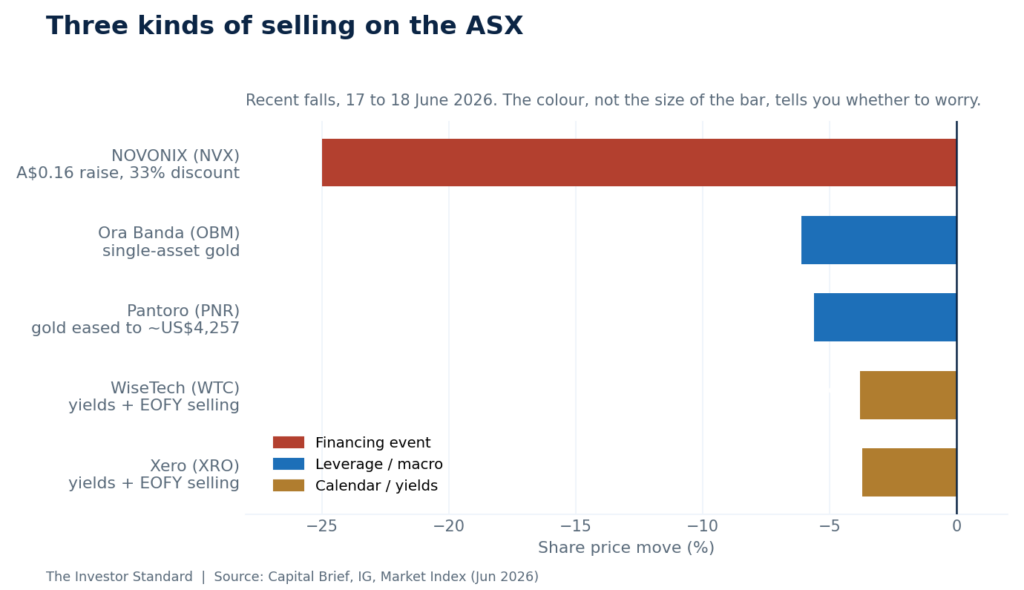

The S&P/ASX 200 dropped 0.62 percent to 8,911.1 on Thursday 18 June 2026, snapping a four-day winning streak after the US Federal Reserve surprised markets with a hawkish hold and US rate futures moved to price a hike by October. Higher offshore yields did the damage at home. Gold eased 1.7 percent to about US$4,257 an ounce, dragging gold miners lower. Technology names fell as long-duration valuations took the yield hit. But the sharpest single-stock fall came a day earlier, from a microcap almost no index investor owns. NOVONIX (ASX: NVX) shares slid about 25 percent to roughly A$0.18 on Tuesday 17 June after a deeply discounted capital raise (Capital Brief, 17 Jun 2026).

NOVONIX share price: the market read a 33% discount as distress

The terms were ugly on their face. NOVONIX raised about A$20.7m through an institutional placement at A$0.16 a share, a 33 percent discount to the prior close of A$0.24, alongside a share purchase plan of up to A$3m at the same price. A one-third discount on a thinly traded name reads as a company taking whatever the market will give it, and it punishes existing holders who do not tip in fresh cash. The tape sold first and asked questions later.

Here is what the 25 percent fall skipped over. Six days earlier, on 11 June 2026, NOVONIX delivered a mass-production qualification sample, a “C-sample”, of synthetic graphite anode material to its lead customer Panasonic Energy. The company says it is the first such sample made in North America, and it is the gate to a four-year, 10,000-tonne offtake once Panasonic signs off. The business also sits behind a US$754.8m conditional loan from the US Department of Energy, a US$100m DOE grant and a US$103m investment tax credit for its American plants. Against that backing, a A$20.7m equity top-up is a bridge to keep building while the DOE loan stays conditional. It is not the act of a company running out of road.

So the discount is the wrong thing to anchor on. It reflects a small, retail-heavy register where moving any size means cutting price, not a collapse in the value of the asset behind the shares. The market treated a financing decision as a verdict on the business, and the two are not the same.

The honest counter sits in the cash flows. NOVONIX has consumed capital for years. It booked a US$84.5m net loss in FY2025 and held US$81.3m of cash at 31 December 2025 (NOVONIX FY2025 results). Qualification with Panasonic is not signed, mass production for that contract is not expected until the second half of 2027, and “milestone, then discounted raise” has become a familiar pattern for this register. Each cut-price placement hurts holders who cannot keep following their money. This is a binary, government-backed development story, not a value stock, and it should be sized that way.

The numbers behind NOVONIX

| Metric | Figure (as at) | Why it matters |

|---|---|---|

| Placement price vs last close | A$0.16 vs A$0.24, a 33% discount (17 Jun 2026) | The dilution the market fixated on |

| Raise size | ~A$20.7m placement plus up to A$3m SPP (Jun 2026) | Small against the project backing |

| Cash on hand | US$81.3m (31 Dec 2025) | Runway while the DOE loan remains conditional |

| FY2025 net loss | US$84.5m (FY2025) | The cash burn that forces further raises |

| DOE conditional loan | US$754.8m (offered Dec 2024) | Strategic backing the market largely ignored |

| Panasonic offtake | 10,000t over 4 years, post-qualification | The demand anchor the C-sample could unlock |

The gold miners did exactly what they’re built to do

The second sell-off looks scarier than it is. Gold slipped 1.7 percent overnight, and the local miners fell several times harder. Ora Banda Mining (ASX: OBM) dropped 6.1 percent to A$1.31, Pantoro (ASX: PNR) lost 5.6 percent to A$2.89, and Westgold Resources (ASX: WGX) eased 3.9 percent to A$5.22 (IG, 18 Jun 2026). A small move in the metal became a large move in the equities, and that is the point.

A producer earns the gold price minus its costs, so a 1.7 percent dip in the price is a much bigger dip in the margin, and a bigger one again in the share. This is operating leverage running in reverse, sharpened by a crowded gold-miner trade unwinding on a single hawkish meeting. Nothing in these businesses changed on Thursday. What to watch is whether gold holds near US$4,300. If it does, the highest-cost, highest-leverage names are the ones that snap back hardest.

The tech sell-off has a deadline

The third fall is the most mechanical. WiseTech Global (ASX: WTC) dropped 3.8 percent to A$36.87, Xero (ASX: XRO) lost 3.7 percent to A$71.87 and Seek (ASX: SEK) fell 3.4 percent to A$13.46 (IG, 18 Jun 2026). Two forces are at work, and only one is a thesis. Higher US yields genuinely compress the value of profits dated far in the future, and that pressure can persist. The second force is the calendar. Australia’s financial year ends on 30 June, and investors sell this year’s losers to bank tax losses before the line is drawn. Tax-loss selling targets the names that already had a poor year, it is forced rather than considered, and it fades once the deadline passes. The tell will come in July. If the hardest-sold names recover into the new financial year, a chunk of this week’s fall was a calendar, not a downgrade.

What to Watch

Watch whether NOVONIX’s SPP clears at A$0.16 and whether Panasonic advances the qualification process. For the miners, the key signal is gold holding around US$4,300. For technology names, watch for a July rebound in the end-of-financial-year losers.

The real NOVONIX catalyst is the US Department of Energy loan moving from conditional approval to funded debt. Without it, equity remains the main source of capital and dilution continues to compound.

NOVONIX is a cash-burning microcap with unsigned qualification milestones and conditional funding. Sized incorrectly, it can become a capital sink.

Gold miners carry the same operating leverage on the way down as they do on the way up. Technology names also remain exposed to a rate path that may not turn, regardless of any calendar-driven rebound.

Investor Takeaway

Read the cause before the candle. Of this week’s three falls, only the NOVONIX share price move carried fresh information about a company, and even there the information cut both ways, a milestone and a dilution in the same week. The gold miners did what leverage always does. The tech names are partly being sold by a calendar that resets on 1 July. The instinct is to treat the biggest red bar as the worst news. This week, the biggest bar is the one with the most going on underneath it, good and bad, and the smaller ones are mostly the market repricing the cost of money and clearing its tax books. Price the reason, not the colour.