AUM Growth

Over the past eight years, Blackstone has fundamentally reshaped its capital base. Total assets under management have expanded from $439 billion to approximately $1.3 trillion, nearly tripling in size over the period.

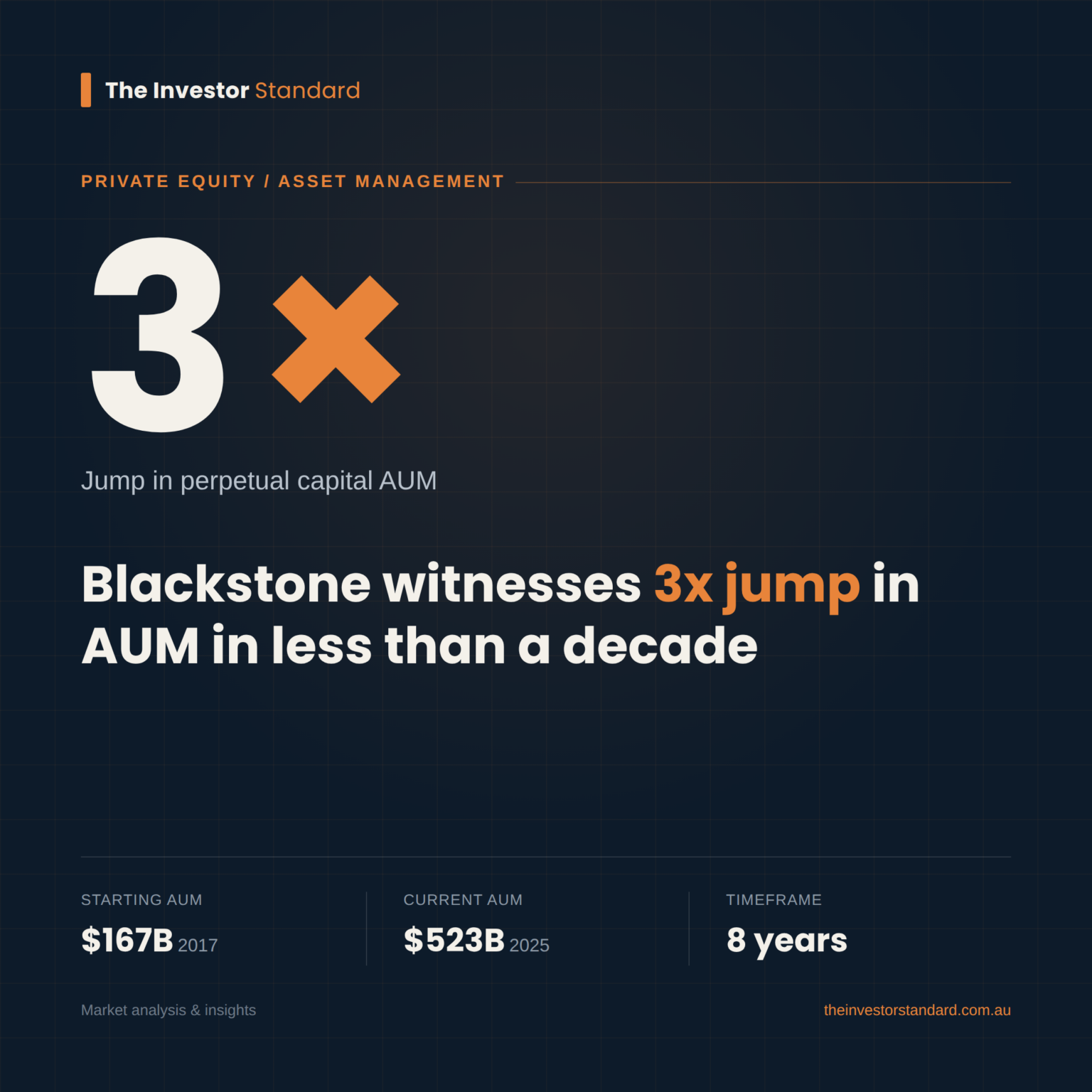

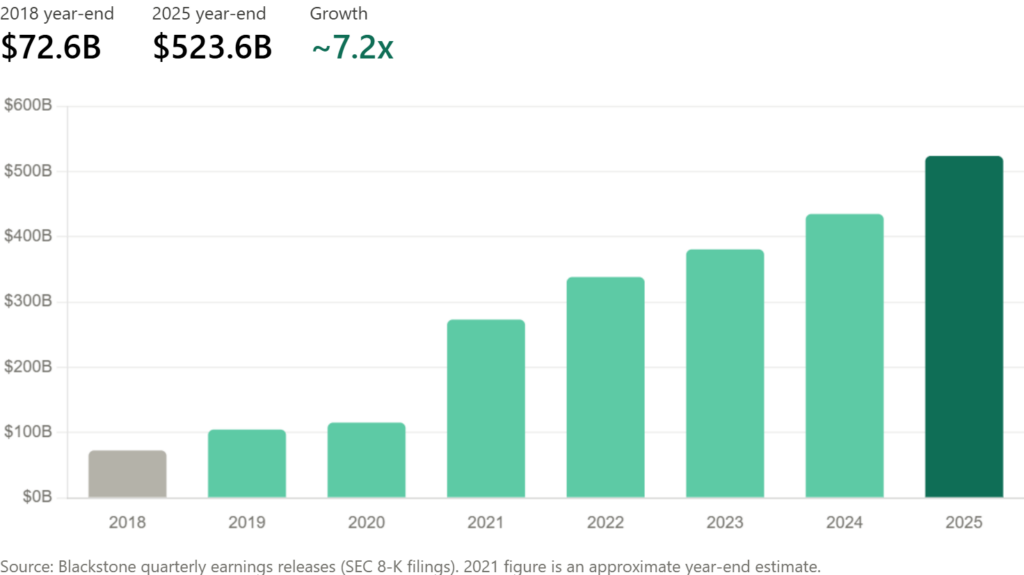

The more significant development, however, has been the rapid growth of its perpetual capital platform. Assets in these vehicles have increased from $64 billion to $539 billion, representing an impressive eightfold expansion.

This stark difference in growth rates reflects a deliberate strategic evolution. While Blackstone has continued to grow its overall platform, it has increasingly focused on attracting long-duration, permanent sources of capital that provide greater stability, flexibility, and the ability to remain invested across market cycles.

What is Perpetual Capital?

Perpetual capital refers to investment vehicles that are designed to operate without a predetermined end date, unlike traditional private equity funds, which typically return capital to investors after a fixed investment period of seven to ten years.

Rather than following the conventional cycle of raising a fund, deploying capital, exiting investments, and launching a new vehicle, perpetual capital structures allow assets to remain invested indefinitely. This enables managers to generate recurring fee income, reinvest proceeds without the need to liquidate holdings, and pursue opportunities with a longer-term horizon.The result is a fundamentally different business model, one that provides greater stability, more predictable earnings, and increased flexibility in how capital is allocated and managed over time.

Why Blackstone is Doubling Down

The appeal of perpetual capital is both straightforward and compelling.

1. A more stable and predictable fee base

Unlike traditional private equity funds that reset after each lifecycle and require continual fundraising, perpetual capital provides an ongoing pool of assets under management. This creates a more consistent and predictable stream of management fees over time.

2. Reduced fundraising burden, greater investment focus

Fundraising is resource-intensive and inherently uncertain. By expanding perpetual capital, Blackstone reduces its reliance on repeated capital raises and can dedicate more attention to its core strengths: sourcing opportunities and managing investments.

3. Greater flexibility over long-term holdings

Closed-end fund structures often require asset sales based on predefined timelines rather than optimal timing. Perpetual capital removes this constraint, allowing managers to hold high-quality assets for longer periods, navigate market cycles more effectively, and maximise long-term value creation.

In essence, it better aligns the capital base with long-duration investment strategies.

Structural Shift in the Business Mix

Perpetual capital now accounts for 41% of Blackstone’s total assets under management, up sharply from just 15% in 2018. This is far more than a gradual shift; it reflects a structural transformation in the firm’s overall business model.

By strategy, the breakdown is as follows:

- Credit & Insurance: approximately 55% of assets are in perpetual capital vehicles

- Real Estate: around 54%

- Private Equity: historically the lowest exposure, but now accelerating quickly

Even within private equity, traditionally dependent on closed-end fund structures, adoption has been rising rapidly. The share of perpetual capital has increased from 13% in 2022 (about $37 billion) to 27% today, or roughly $116 billion. Taken together, this trend highlights how even the most conventional segments of the business are steadily evolving toward more permanent capital structures

Industry-Wide Trend

Blackstone is not the only firm undergoing this shift. Other leading alternative asset managers, including Apollo, Brookfield, KKR, and Blue Owl, have also been actively scaling their perpetual capital platforms.

This points to a broader industry-wide recognition: as asset managers grow into trillion-dollar-scale platforms, the future increasingly lies in permanent capital structures that provide stability, scalability, and long-term alignment with investment horizons.

The Trade-Off: Liquidity Risk

Despite its advantages, perpetual capital also introduces a distinct set of challenges—particularly around liquidity management.Many perpetual investment vehicles, especially those open to retail investors, include scheduled redemption windows that are often subject to limits, such as quarterly withdrawal caps. Under normal market conditions, this structure functions effectively. However, during periods of market stress, vulnerabilities can emerge:

- Investors may seek to redeem capital at the same time

- Withdrawal requests can become heavily concentrated within a short period

- Managers may be forced to source liquidity quickly under unfavourable conditions

This can create a structural tension between relatively illiquid underlying assets—such as real estate and private credit, and the expectation of periodic liquidity from investors. Balancing this mismatch remains one of the most important and complex risks as perpetual capital strategies continue to scale.

Conclusion

Blackstone’s evolution over the past decade is not simply a story of scale but of structural refinement.By increasing its perpetual capital share from 15% to 41% of assets under management, the firm has been steadily reshaping itself into a more stable, scalable, and resilient organisation.

This transition enables Blackstone to:

- Generate more consistent fee income

- Deploy capital with greater efficiency

- Take a longer-term approach to investment decisions

Although liquidity risks have not disappeared, the overall trajectory is clear. Perpetual capital is moving beyond a niche allocation strategy and increasingly forming the structural backbone of modern alternative asset management.