In the recent past, Thailand was one of Asia’s great economic success stories.

Between the late 1980s and mid-1990s, the country transformed from an agrarian economy into a regional manufacturing powerhouse. Annual GDP growth regularly exceeded 8%, foreign investment poured in and millions were lifted out of poverty.

Many believed Thailand would become the next developed Asian economy and a leader in south east Asia.

Instead, it stalled.

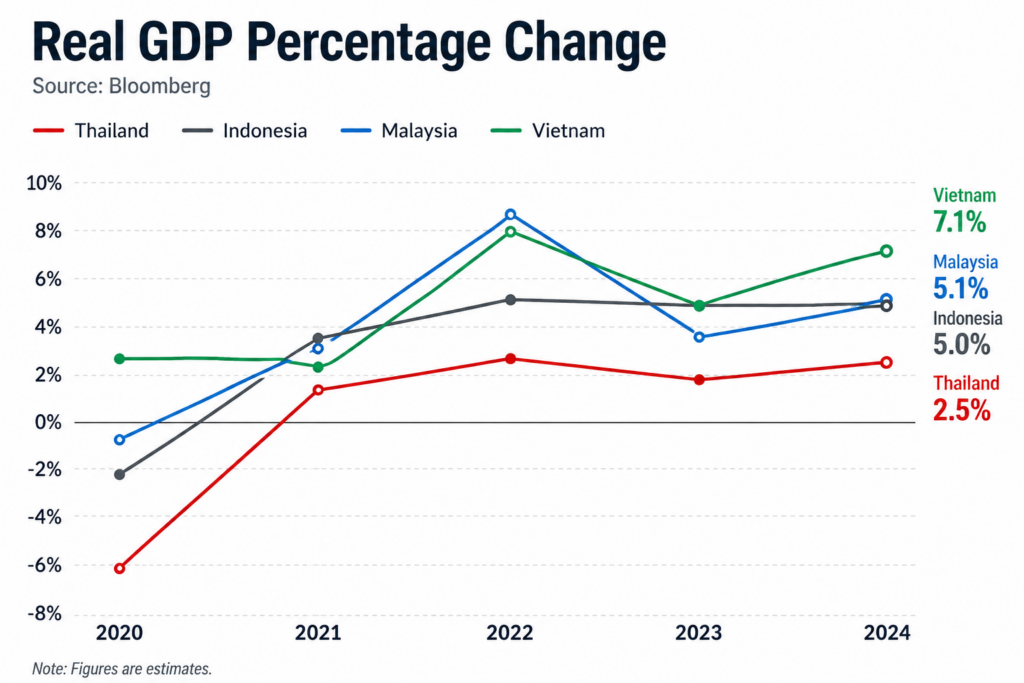

While neighbours such as Vietnam, Malaysia and Indonesia have continued accelerating over the past decades, Thailand has struggled to sustain growth, with its economy expanding by only around 2% annually in recent years. Foreign investment has weakened, productivity has stagnated and the country now faces one of the fastest-ageing populations in Asia and one of the lowest fertility rates.

The slowdown cannot be explained by a single recession, global pandemic or trade dispute.

Rather, it is the result of several structural problems that have built up over decades.

To understand why Thailand has fallen behind, we need to go back to the crisis that changed everything.

The Crisis That Changed Thailand’s Economy

Thailand’s modern economic challenges can largely be traced back to the 1997 Asian Financial Crisis.

During the late 1980s and early 1990s, the country experienced an extraordinary period of growth. The economy expanded by around 8% to 9% annually as banks aggressively extended credit, foreign capital flowed into the country and investment surged. Thailand appeared well on its way to becoming one of Asia’s next high-income economies.

Beneath the surface, however, serious vulnerabilities were beginning to emerge.

Financial institutions accumulated excessive risk, corporate debt rose rapidly and Thailand developed a large current account deficit. Much of the country’s economic expansion had become dependent on continuous capital inflows and a stable Thai baht.

When investor confidence evaporated in 1997, that model quickly unravelled.

Speculators attacked the baht, forcing Thailand to abandon its currency peg. The baht lost more than half of its value, banks collapsed, businesses failed and millions of people lost their jobs. What had been one of the fastest-growing economies in the world entered one of the deepest recessions in Asian history.

While Thailand eventually returned to growth, the economy never fully regained the momentum it had enjoyed before the crisis.

The financial shock left more than economic scars.

It fundamentally reshaped Thailand’s political landscape, setting in motion decades of instability that would prove just as damaging as the crisis itself.

Political Instability Has Come At A Cost

The aftermath of the 1997 crisis extended well beyond the economy.

In 2001, telecommunications billionaire Thaksin Shinawatra was elected Prime Minister after campaigning on policies aimed at revitalising growth and expanding opportunities outside the nations capital Bangkok. Under his administration, Thailand’s economy recovered strongly, but his growing popularity also deepened divisions within the country’s political establishment.

In 2006, a military coup ousted Thaksin.

It marked the beginning of nearly two decades of recurring political instability. Governments repeatedly dissolved, prime ministers were ousted by courts or coups, and prolonged periods of protests became a recurring feature of Thai politics. Since becoming a constitutional monarchy in 1932, Thailand has experienced numerous successful military coups and multiple constitutional rewrites, creating an environment of persistent political uncertainty.

For investors, stability matters.

Large-scale investments in manufacturing, infrastructure and technology are often planned decades in advance. Frequent changes in government and uncertainty over future policy make those long-term commitments more difficult to justify.

The result is an economy where political uncertainty has increasingly become an economic headwind.

While many Southeast Asian economies have focused on attracting new industries and foreign investment with stability and low to moderate and simple taxes and regulations, Thailand has often found itself distracted by domestic political conflict, resulting in deep instability which shakes investor confidence.

Thailand’s Economy Dominated By A Handful Of Conglomerates

Political instability is only part of the story.

Thailand’s economy is also characterised by a high concentration of wealth and corporate power.

Today, the country’s richest 10% control nearly 70% of national wealth, one of the highest levels of wealth inequality in the Asia-Pacific region. Much of Thailand’s corporate landscape is dominated by a small number of powerful family-owned conglomerates with interests spanning retail, telecommunications, banking, property and manufacturing.

This concentration has important economic consequences.

Highly concentrated markets tend to reduce competition, making it more difficult for new businesses to succeed against and challenge established firms. Over time, this can discourage innovation, investment, slow productivity growth and limit the development of entirely new industries.

It also creates a feedback loop between economic and political power.

Large businesses often possess significant political influence, while political stability can help preserve existing market positions. The result is an environment where meaningful structural reforms including measures to increase competition can be difficult to implement.

At the same time, many Thai households remain burdened by high levels of debt. Household debt has climbed to around 90% of GDP, among the highest in Asia. As a larger share of household income is directed towards servicing debt, consumer spending weakens, leaving less money available for investment, education and entrepreneurship.

Together, these factors have made it increasingly difficult for Thailand to generate the productivity gains needed to return to the rapid growth it had before the Asian Financial Crisis.

An Ageing Population Is Creating Another Challenge

Even if Thailand were able to resolve its political and structural issues, it faces another long-term challenge that is far more difficult to reverse.

Its workforce is shrinking.

Like many developed economies, Thailand is ageing rapidly. The difference is that it is growing old before it has become truly wealthy. The country’s working-age population began slowing in the mid-2010s and has been declining since around 2019, a trend that is expected to continue for decades.

This has significant economic implications.

A smaller workforce means fewer people producing goods and services, fewer taxpayers supporting public finances, lower consumption and greater pressure on healthcare and pension systems. At the same time, businesses face increasing difficulty finding skilled workers to support higher-value industries.

Though many countries look to offset the decline through immigration, Thailand also struggles in bringing in immigrants with net migration below 30,000.

The challenge is particularly acute as Southeast Asia competes to attract investment in sectors such as semiconductors, AI and advanced manufacturing.

While countries such as Vietnam have rapidly expanded their manufacturing capabilities and attracted multinational investment, Thailand has struggled to develop the same pipeline of highly skilled workers needed to support these industries.

Combined with slower productivity growth and persistent political uncertainty, demographic decline has become another structural headwind weighing on Thailand’s long-term economic outlook.

Taken together, these challenges help explain why an economy that once appeared destined to become one of Asia’s success stories has struggled to regain its former momentum.

Can Thailand Turn Things Around?

Thailand’s challenges are significant, but they are not insurmountable.

The country still possesses many of the ingredients that once made it one of Southeast Asia’s most successful economies. It has a well-developed manufacturing base, world-class tourism industry, strategic location and strong integration into regional supply chains.

The challenge is ensuring those advantages remain relevant in a rapidly changing global economy.

As neighbouring countries compete for investment, Thailand will need to improve productivity, develop a more highly skilled workforce and create an environment that encourages long-term investment and revitalises confidence.

None of those goals will be easy to achieve without greater political stability.

Investors are generally willing to tolerate short-term economic weakness if they have confidence in a country’s long-term direction. Political uncertainty, however, makes that confidence far more difficult to establish.

Thailand’s economy has overcome major challenges before.

Whether it can do so again will depend not only on global economic conditions, but also on its ability to implement the structural reforms needed to restore productivity, attract investment and regain the momentum that once made it one of Asia’s fastest-growing economies.