Australia is one of the richest nations on Earth with its resources. Beneath its soil lie vast deposits of iron ore, coal, natural gas, oil, gold, copper and uranium that have helped generate trillions of dollars in economic activity. Yet a fundamental question sits at the centre of every debate surrounding mining taxation: who should benefit from the extraction of these resources? And how much should each party reap the rewards?

- The Problem With Royalties

- What Is A Resource Rent Tax?

- Why Economists Prefer A Resource Rent Tax

- They Encourage More Investment

- The Most Efficient And Least Distortive Tax Base

- They Deliver A Better Return To Taxpayers

- They Tax Economic Rents Rather Than Effort

- They Can Support Broader Tax Reform

- The Trade-Offs Of Resource Rent Tax

- What Now?

Unlike factories, machinery or IP, non-renewable resources are not created by private firms. They are natural assets that legally belong to the community and the crown until the rights to extract them are granted. As the Henry Tax Review noted, the community should receive an appropriate return for allowing private companies to exploit these finite resources.

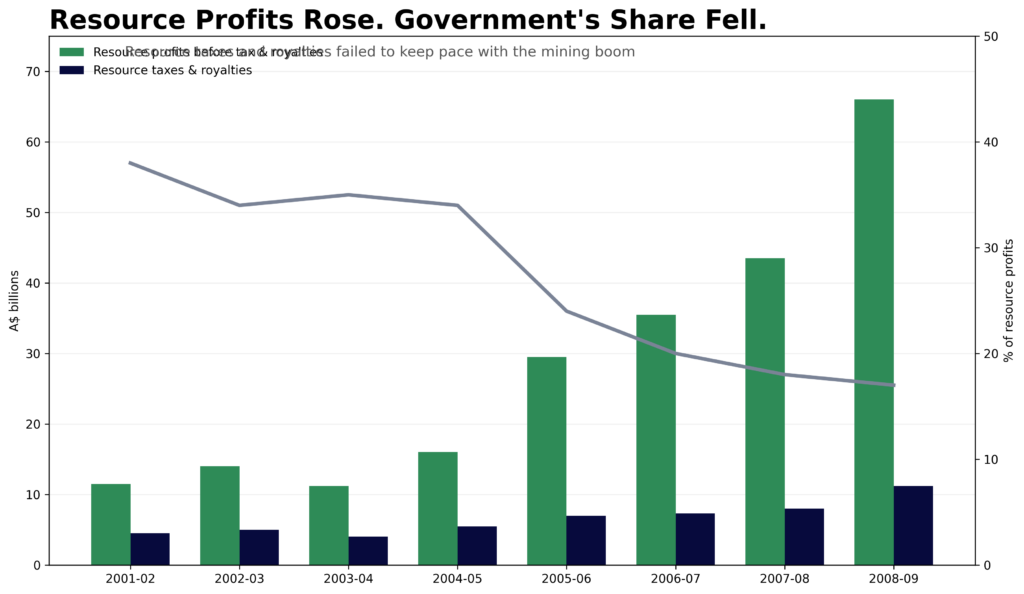

For decades, Australia has heavily relied on state-based royalty systems to generate that return. Under these arrangements, mining companies pay the state based on the volume or value of resources extracted. While royalties provide a stable, reliable and predictable source of revenue, many economists argue they suffer from a critical flaw: they tax production rather than the profit. As a result, royalties can discourage investment, reduce production, hurt marginal projects disproportionately and actually lower the value generated from Australia’s natural resources.

This has led to growing interest in an alternative approach: resource rent taxation. Rather than taxing every tonne extracted, a resource rent tax targets the “super profits” earned from exploiting publicly owned resources. Proponents argue this allows governments to secure a larger share of mining windfalls while preserving incentives for investment and production.

This article examines the economic case for replacing traditional mining royalties with resource rent taxes, drawing on the findings of Australia’s Future Tax System Review and the broader economic literature surrounding the taxation of non-renewable resources.

The Problem With Royalties

Most Australian states charge royalties on the extraction of natural resources.

While the exact structure varies by commodity and jurisdiction, royalties are typically levied on either the volume or value of production.

At first glance, this appears sensible. If a company extracts publicly owned resources, it seems reasonable that taxpayers should receive a share of the proceeds.

The issue is that royalties are payable regardless of whether a project is highly profitable, marginally economic or even making a loss.

A mining company earning hundreds of millions of dollars in profit may face the same royalty rate as a project generating only a modest return.

As a result, royalties tax production itself instead of profitability.

This distinction is important because it can alter investment decisions.

Projects that may have been commercially viable before royalties can become uneconomic after royalties are applied. Existing mines may reduce production, while some future projects may never proceed at all as they are simply unviable and provide untenable returns.

Economists argue that Australia’s existing royalty arrangements distort investment and production decisions, reducing the return ultimately generated from the nation’s natural resources.

What Is A Resource Rent Tax?

A resource rent tax takes a fundamentally different approach.

Rather than taxing production itself, it taxes the economic rents generated from a resource project.

Resource rent are the excess profits earned after a company has recovered its exploration, development, operating costs and a normal return on capital.

In other words, a “super profit.”

A resource rent tax only begins to apply once a project has become sufficiently profitable.

This distinction is important.

Unlike royalties, a resource rent tax does not increase the cost of extracting each additional tonne of ore or barrel of oil. Instead, it targets the surplus profits generated from exploiting a finite public resource.

As a result, projects that are only marginally profitable face little or no additional tax burden, while highly profitable projects contribute a larger share of their profits to the community.

This allows governments to capture a portion of resource windfalls without discouraging economically viable investment and production.

Why Economists Prefer A Resource Rent Tax

They Encourage More Investment

One of the main criticisms of royalties is that they can discourage investment in marginal projects.

Because royalties are levied regardless of profitability, it discourages investment and production even when a project would otherwise be commercially viable.

While R\royalties can make projects that create value for society never happen at all, rent taxes operate differently.

As they only apply once a project has recovered its costs and earned a normal return on capital, they are less likely to influence decisions about whether a mine should be developed, expanded, or kept operating.

More projects remain commercially viable and thus can encourage additional exploration, investment, production and projects that may not have occurred under a royalty-based system.

This allows governments to capture a share of the windfall profits generated from publicly owned resources without directly penalising production itself.

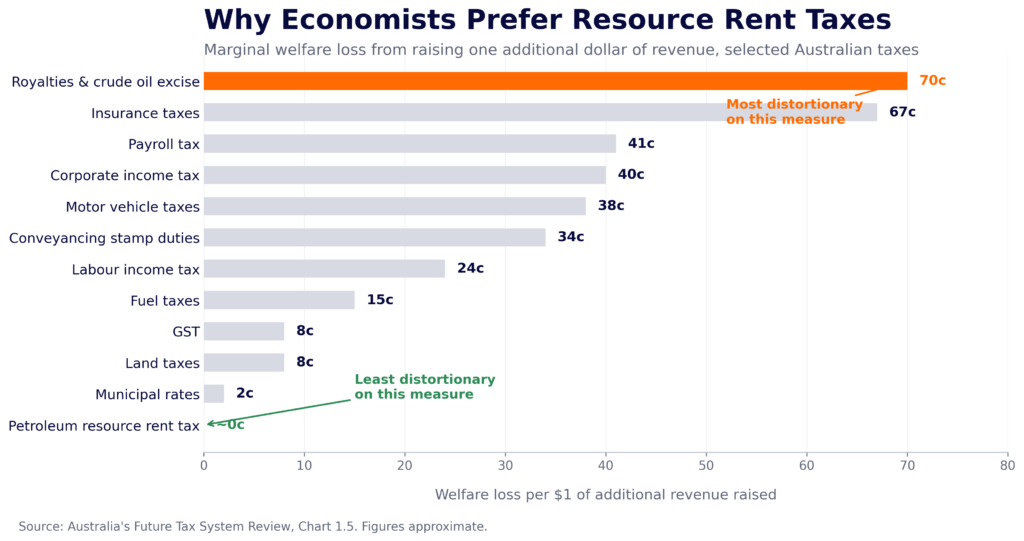

The Most Efficient And Least Distortive Tax Base

These are one of the best tax bases because they are inherently immobile.

Labour can move overseas and its supply controlled, capital can be invested elsewhere, and companies can shift operations across jurisdictions. Iron ore deposits, however, remain in the Pilbara regardless of Australia’s tax settings.

For this reason, the Henry Tax Review identified economic rents from natural resources as one of the four key pillars of an efficient long-term tax system.

A tax on excess profits therefore has the potential to raise revenue with far fewer distortions than taxes on work, investment, or production.

They Deliver A Better Return To Taxpayers

Resource rent taxes allow the public to share more directly in the value generated from publicly owned resources.

Unlike royalties, which are largely unresponsive to profitability, resource rent taxes rise and fall alongside project profits, global commodity prices and terms of trade.

This means governments receive a larger share of revenue during booms or when companies benefit from particularly valuable resource deposits that “print rent.”

A well-designed resource rent tax could generate a greater return for the community over time while still attracting private investment and not posing as a huge sovereign risk.

They Tax Economic Rents Rather Than Effort

A significant portion of mining profits often comes from factors outside a company’s effort.

Commodity prices are largely determined by global supply and demand, while the quality of a mineral deposit is determined by geology rather than effort.

If iron ore prices double due to increased demand from overseas markets, mining companies will experience a substantial increase in profits despite it not coming out of their changes or effort.

Resource rent taxes are designed to capture a share of these windfall gains while leaving normal returns to investment untouched by it.

They Can Support Broader Tax Reform

Rents are one of the least distortionary tax bases available to governments.

Unlike labour or capital, natural resources cannot be relocated to another country and rents are generally not produced from effort.

As a result, revenue raised from resource rents can potentially reduce reliance on taxes that have a greater impact on economic activity, such as company tax or income tax.

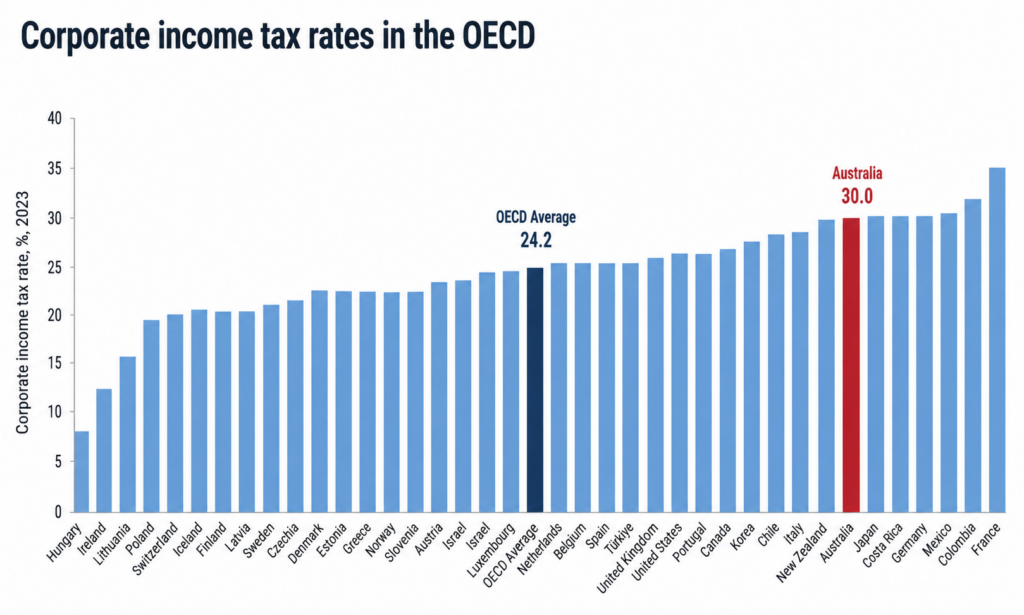

An example of this was in the 2010-11 Federal Budget, where the Rudd Government proposed the Resources Super Profit Tax (RSPT) and would use the proceeds to help fund a company tax cut from 30% to 28%.

This shifts the tax base from more distortionary bases to less distortionary bases. Company tax influences investment decisions across the broader economy, resource rents arise from the exploitation of finite natural resources and are generally considered less responsive to taxation.

Australia’s rate is fairly above the OECD average of 24% and reducing it would increase competitiveness and attract additional investment.

The Trade-Offs Of Resource Rent Tax

Complexity

Unlike royalties, resource rent taxes require governments to monitor costs, deductions, depreciation schedules, transfer pricing arrangements and carried-forward losses.

This increases administrative complexity for both industry and government.

Design Matters

Resource rent taxes may be theoretically economically attractive , but poorly designed systems can fail to deliver expected revenues.

Australia’s experience with the PRRT demonstrates how generous deductions and uplift rates can significantly delay tax collections, even when projects are highly profitable.

The effectiveness of a resource rent tax ultimately depends on its design.

Revenue Volatility

Royalties tend to provide a relatively stable revenue stream because producers pay them based directly on production levels.

Resource rent taxes are more sensitive to profitability and prices.

During downturns, revenues may fall significantly as profits decline or disappear altogether. As a result, revenue from the rent tax and company tax fall.

Another issue may be the governments temptation to use temporary surges in revenue to fund permanent spending or tax cuts.

Under the Howard Government, the government used the surge in revenue generated by the mining boom to fund large permanent tax cuts, concessions, and spending.

This created structural deficits after the boom ended with receipts as a % of GDP falling by over 12% from 2007-08 to 2013-14.

As summed up by Chris Richardson: “Temporary boom, permanent promises.”

Political Challenges

Resource rent taxes often face strong opposition from industry because they directly target their profits.

The proposed RSPT became a massively contentious reform, highlighting the difficulty of implementing major changes to resource taxation.

State Government Opposition

Australia’s states particularly WA and QLD heavily rely on royalties as a significant source of revenue.

Unlike the Commonwealth, the Constitution largely barrs state governments from levying broad-based taxes such as income and company tax. Therefore, depend heavily on payroll taxes, stamp duties and royalties for revenue.

As a result, proposals to replace royalties with resource rent taxes have often faced resistance from state governments concerned about losing a stable and predictable revenue source.

The Commonwealth would have to compensate the relevant states by increasing GST distribution or sharing the rent tax receipts.

This creates a political challenge even when economists argue that resource rent taxes are more efficient in theory.

What Now?

Resource companies should pay tax, but the key question is how governments should structure that tax.

While many economists favour resource rent taxes in principle, Australia no longer faces the question of whether to impose such taxes; instead, policymakers must decide how to design and implement them.

Recent reforms to the PRRT represent one attempt to improve the balance between taxpayer returns and investment certainty. However, debates over mining royalties, gas taxation and broader resource tax reform are unlikely to disappear.

As demand for critical minerals, LNG and other resources continues to evolve, questions surrounding how Australians share in the value of their natural resources will remain at the centre of economic policy discussions.

Disclaimer: The views expressed in this article are solely those of the author and do not necessarily reflect the views of any employer, organisation, or affiliated entity.