For decades, management consulting was one of the most prestigious industries in the corporate world.

A job offer from McKinsey, Bain or Boston Consulting Group was seen as a golden ticket, promising high salaries, rapid career progression, deep learning opportunities and a pathway into the executive ranks of global business. Governments, multinational corporations and investors routinely paid millions of dollars for their advice.

Today, that reputation is being tested.

Across the industry, consulting firms are cutting staff, growth has slowed and clients are increasingly questioning whether the value they receive justifies the cost. McKinsey has reportedly laid off thousands of employees, while firms across the Big Four have reduced headcount as demand weakens. At the same time, advances in AI are starting to automate many of the analytical tasks that once formed the foundation of consulting work especially among junior employees.

It would be easy to conclude that consulting is simply another victim of the AI revolution.

The reality is more complicated.

The challenges facing the industry today did not begin with ChatGPT. They are the result of a business model that has spent decades evolving, adapting and, in some cases, drifting away from the very problems it was originally created to solve.

To understand why consulting is under pressure, it is worth examining how the industry rose to prominence in the first place.

Why Consulting Was Essential

Despite the criticism often directed at the industry today, management consulting was not originally built on yes men, corporate jargon and PowerPoints.

At its peak, consulting solved genuine business problems during a period of a huge transition.

During the 1980s and 1990s, the US underwent a period of significant deregulation. Previously been constrained by regulation, industries now found themselves free to expand, consolidate and compete on a much larger scale.

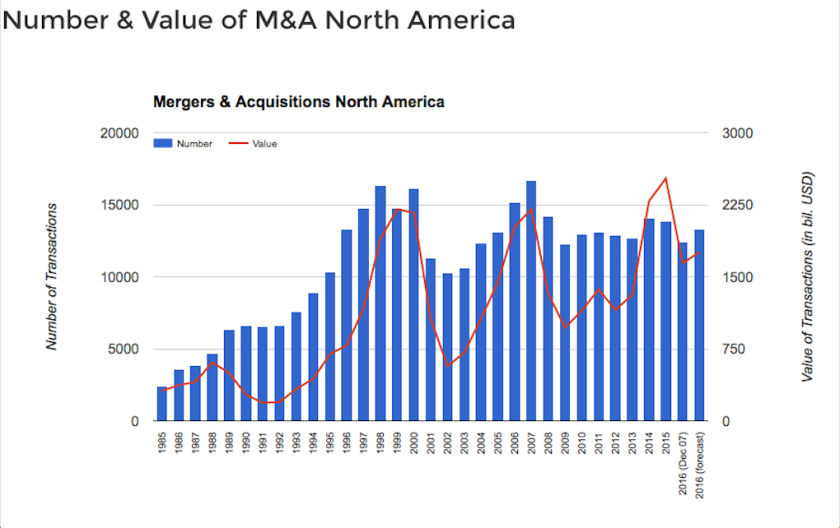

An M&A boom unlike anything seen before was born.

In less than a decade, annual M&A activity increased from US$200 billion to over US$1.7 trillion. Companies raced to acquire competitors, expand market share and achieve economies of scale.

While these deals often created stronger businesses, they also created enormous operational challenges.

A merged company could suddenly find itself with multiple finance departments, HR teams, marketing divisions and multiple overlapping structures. Eliminating unnecessary duplication could generate large savings, but cutting the wrong team could damage the entire organisation.

This was where consultants provided real value.

Consultants were often brought in to help management navigate complex integration processes. Identifying inefficiencies, streamline operations and determine which parts of the new intergrated business should remain or be removed.

In many cases, the value they created was both tangible and measurable.

Companies could directly compare the cost of a consulting engagement with the savings generated through restructuring, integration and operational improvements. The return on investment was often obvious.

As M&A accelerated throughout the 1990s, consulting firms became some of the most influential organisations in corporate America. Firms such as McKinsey, Bain and BCG established themselves as trusted advisers to, while the broader industry grew into a multi-billion-dollar business.

However, the very conditions that fuelled the industry’s rise would eventually begin to disappear.

The Shift To Consulting Governments

By the early 2000s, the environment that had fuelled consulting’s rise changed.

Scandals like Enron, triggered regulatory reforms that slowed M&A and increased scrutiny. The stream of integration projects that powered the industry was drying up.

This looked like a major threat to consulting firms.

Instead, they found new clients: governments.

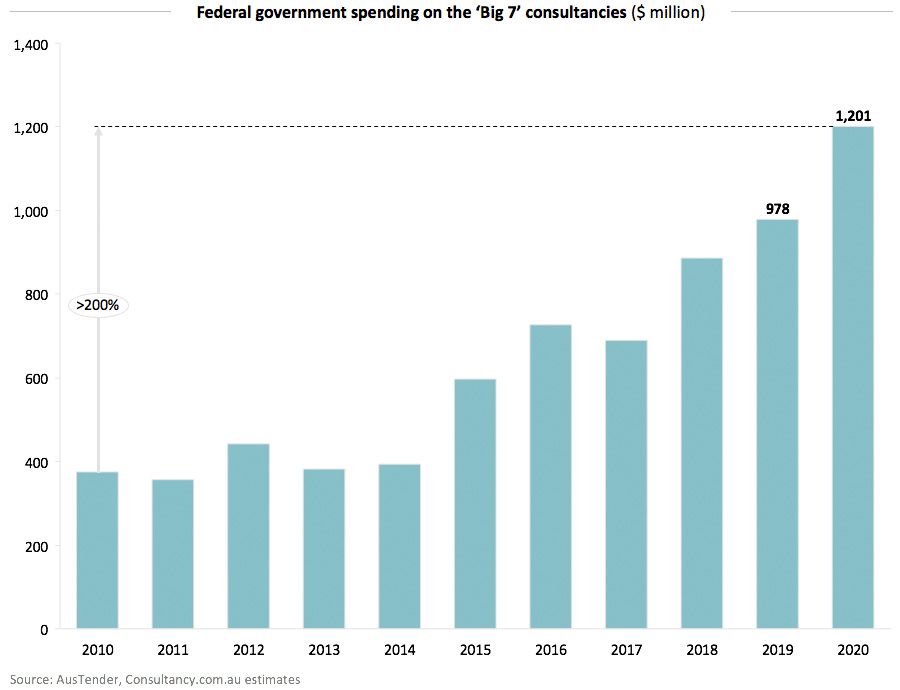

Governments were growing rapidly. Public sector workforces expanded, departments became increasingly complex and bureaucracies struggled to manage efficiently. Faced with mounting operational challenges, many turned to consultants.

Over the following years, spending on consultants increased dramatically. Firms that had built their reputation advising execs and management were now advising ministers, departments and agencies on everything from procurement and projects to restructuring and strategy.

One difference changed thing, private sector outcomes are more measurable.

If consultants recommended restructuring, management can determine whether profits improved. If a merger integration fails, shareholders bear the cost and executives held accountable.

Government projects often operate differently.

Large public-sector initiatives take years, involve multiple departments and pass through several layers of oversight. When a project succeeds, credit is shared. When it fails, responsibility can be difficult to assign, changing the industry.

Consultants could be receive enormous payouts without being judged on measurable outcomes. A failed recommendation rarely threatened reputation like it might have in the corporate world.

The result was a gradual shift away from consulting as a service tied to performance and towards consulting as insurance.

For executives and government officials alike, hiring consulting firms offered something valuable beyond advice: protection.

If restructuring or projects failed or departments overspent, decision-makers could point to consultants, arguing that recommendations had come from some of the most respected advisers in the world.

In many cases, consultants became less important for the quality of the advice and more important for credibility, leading to enormous consequences for the industry.

When Prestige Became The Product

As consulting firms expanded deeper into government and large corporations, something began to change.

The industry’s success became increasingly disconnected from measurable outcomes.

In the early days of consulting, value was relatively easy to demonstrate. A merger integration either reduced costs or it didn’t, improved profitability or it failed.

Over time, consulting engagements became more abstract.

Rather than solving a specific operational problem, firms were increasingly hired to advise on culture, strategy, transformation and stakeholder engagement. Projects that were far harder to measure.

As a result, the quality of the advice often became secondary to the reputation of the firm delivering it.

This was also the era that gave rise to corporate speak and yes men.

Terms like “strategic transformation”, “stakeholder alignment” and “value creation” became common features of consulting presentations. Long and nice looking PowerPoint presentations that at times offered little insight became common.

While these concepts and presentations were not necessarily meaningless, they often lacked the accountability associated with more traditional consulting work.

An executive could spend millions on a strategy review without ever having to answer a simple question: did it actually work?

Yet demand continued to grow.

Part of the reason was that consultants provided something beyond advice, they provided legitimacy.

For executives facing difficult decisions, hiring a prestigious consulting firm offered a form of protection and insurance.

Layoffs, restructurings, M&A and strategic pivots could all be justified by pointing to recommendations from McKinsey, Bain, BCG or one of the Big Four.

In effect, consultants at times became a form of outsourced decision-making, yes men and confirmation bias.

The advice still mattered, the brand attached to the advice often mattered just as much and at times more.

AI Didn’t Create The Problem, It Exposed It

It would be easy to blame AI for the consulting industry’s current struggles and layoffs.

After all, many of the tasks traditionally performed by junior consultants can now be completed in minutes.

Research can be automated, market analysis can be generated instantly, financial models can be built faster than ever before, presentations can be drafted with a simple prompt.

But AI did not create the consulting industry’s problems, it merely exposed them.

For years, clients were willing to pay premium fees because consulting firms had a unique expertise.

That expertise was valuable when information was difficult to obtain and process and analysis required significant time and manpower.

AI alters that equation.

When the same research can be completed internally in days rather than externally in weeks, clients naturally begin questioning what exactly are they paying for.

This is particularly problematic for the industry’s traditional pyramid structure.

Consulting firms rely on large numbers of junior employees performing research, analysis and modelling before that work is reviewed by more senior staff who also dealt with client relations.

Much of this work forms the economic foundation of the consulting business model.

Unfortunately for consultants, it also happens to be the type of work that AI performs best.

The result is an uncomfortable reality.

The technology that consulting firms are trying to sell to clients is simultaneously making some of their own services less valuable.

For an industry built around expertise, that creates a difficult question.

If technology can produce similar outputs at a fraction of the cost, where does the value proposition come from?

What Survives

None of this means consulting is disappearing, far from it.

Businesses will always face complex problems that require specialist expertise, outside perspectives and experienced operators.

Businesses integrating a major acquisition still needs help, manufacturers redesigning its supply chain still needs help, governments implementing a multi-billion-dollar infrastructure project still needs help.

The difference is that clients are becoming less willing and seeing less of a reason to pay premium fees for work that can increasingly be done internally and automated.

Research, analysis, information, advise are all becoming cheap.

As a result, the firms that survive will likely be those that provide something technology cannot easily replicate.

That means genuine expertise, industry knowledge, implementation and most importantly, accountability.

For decades, many consulting firms were able to sell recommendations.

Increasingly, clients want results.

This is already changing the competitive landscape.

The most successful firms are no longer just advising companies on how to adapt to technological change. They are helping businesses implement that change themselves.

Others are investing heavily in specialised capabilities that extend beyond PowerPoint presentations and strategy reports.

In many ways, the industry is being forced back to the roots that made it so successful in the first place.

The consultants who created the most value historically were not those who produced the most impressive slide decks, they were the ones who solved difficult problems and produced valuable outcomes.

AI has not eliminated the need for problem-solving, it has simply made it harder to charge clients for everything else.