The dot-com bubble is often remembered as the ultimate example of market excess and speculative crash.

Companies with no profits raised billions. IPOs doubled or tripled on their first day of trading. Investors poured money into businesses whose entire strategy seemed to revolve around adding “.com” to their name and hoping for the best.

When the bubble finally burst, over US$5 trillion in market value disappeared, indexes plummeted and hundreds of companies collapsed.

But what if the dot-com crash wasn’t actually that bad?

Though that might sound like a strange claim. After all, the collapse of internet stocks remains one of the most famous market crashes in modern financial history.

Yet the dot-com bubble also possessed several characteristics that made it surprisingly survivable.

The speculation was largely concentrated in a relatively small segment of the market. Most of the excess was funded by equity instead of debt. The broader economy remained healthy. And perhaps most importantly, the infrastructure built during the boom eventually proved genuinely useful.

Today’s AI boom looks different.

The amount of capital being committed is larger, the market exposure is broader, the financing is more leveraged. And unlike the late 90s, the rest of the economy may not be strong enough to comfortably absorb a major shock.

If the dot-com bubble serves as a warning from history, the lesson may not be that today’s AI boom looks similar.

It may be that today’s AI boom looks significantly harder to contain.

The Scale Of The AI Boom

If the dot-com era was defined by optimism, the AI boom is being defined by scale.

Between 1997 and 2000, about US$344 billion (inflation adjusted) of venture capital was invested into internet-related businesses in today’s dollars. At the time, it represented an extraordinary amount of money chasing a single technological trend.

Today, AI startups are attracting similar sums in a fraction of the time.

In 2025 alone, AI companies absorbed approximately US$222 billion in venture funding. And that figure excludes the enormous infrastructure spending taking place alongside it.

Amazon, Microsoft, Google and Meta are expected to collectively spend more than US$600 billion on capital expenditure in 2026 alone, much of it directed toward AI infrastructure.

The comparison to the late 1990s is obvious. Then, companies raced to build fibre-optic networks. Today, they’re racing to build data centres.

The difference is that modern AI infrastructure is significantly more expensive to maintain. Data centres require constant power, cooling and hardware upgrades as newer chips rapidly replace older systems.

That raises a difficult question.

Are investors funding the foundations of the next tech revolution, or are they building far more capacity than the market wants or needs?

History suggests both can be true at the same time.

The Leverage Problem

Scale alone does not make a bubble dangerous.

What made the dot-com crash relatively contained was that most of the speculation was funded through and thus the losses contained to largely equity. Investors bought stakes and shares in internet companies knowing they could lose money if the bets failed.

Today’s AI boom looks different.

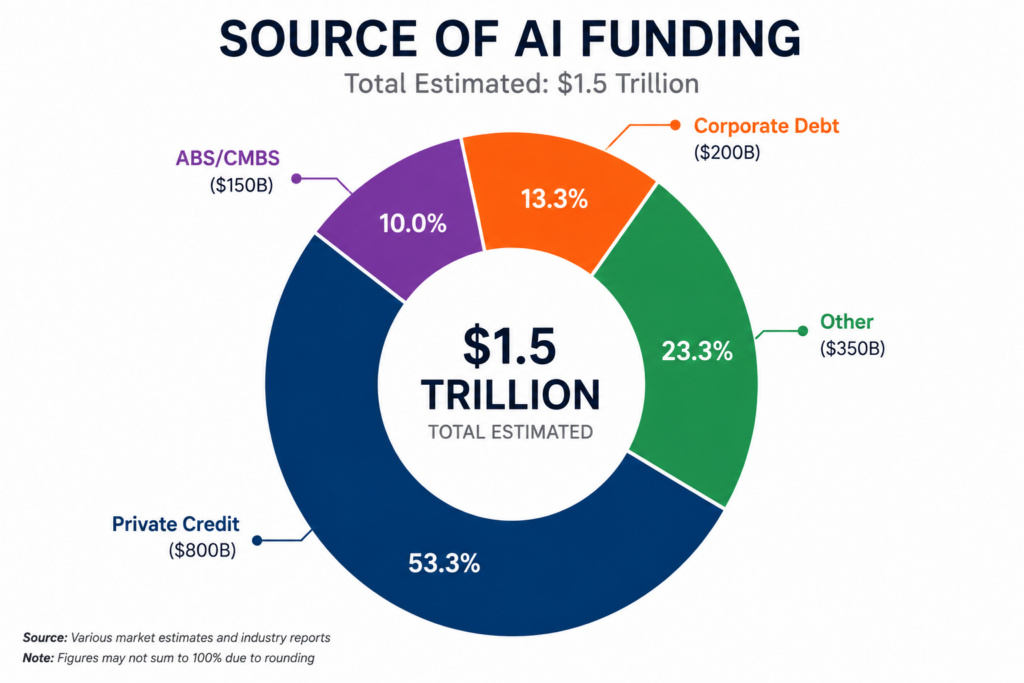

OpenAI alone has reportedly committed to spending more than US$1 trillion on data centres and computing infrastructure over the coming decade. Across the industry, spending on AI infrastructure is expected to reach trillions dollars within just a few years.

Much of that investment is not being funded by equity investors willing to absorb the losses.

Instead, an increasing share is being financed through debt and private credit.

This difference is key as when an equity investor loses money, the damage is largely contained to the investor. When heavily leveraged firms fail, the losses can spread through lenders, credit markets and the broader financial system.

There are already signs of circular financing emerging within the industry. Companies invest in AI developers, AI developers purchase computing infrastructure, infrastructure providers book the revenue, and rising revenues help justify ever higher and stretched valuations.

The same dollar can begin moving around the system in ways that make growth appear stronger than it really is.

None of this means AI is destined to fail. The internet ultimately changed the world despite the dot-com crash.

But history shows that genuinely revolutionary and transformative technologies and speculative bubbles can exist simeltanously.

The problem is not whether AI will prove useful. The problem is whether the financial system is underwriting more demand than will ultimately materialise.

Why This Time Is Harder To Avoid

The dot-com bubble was surprisingly easy to opt out of and avoid.

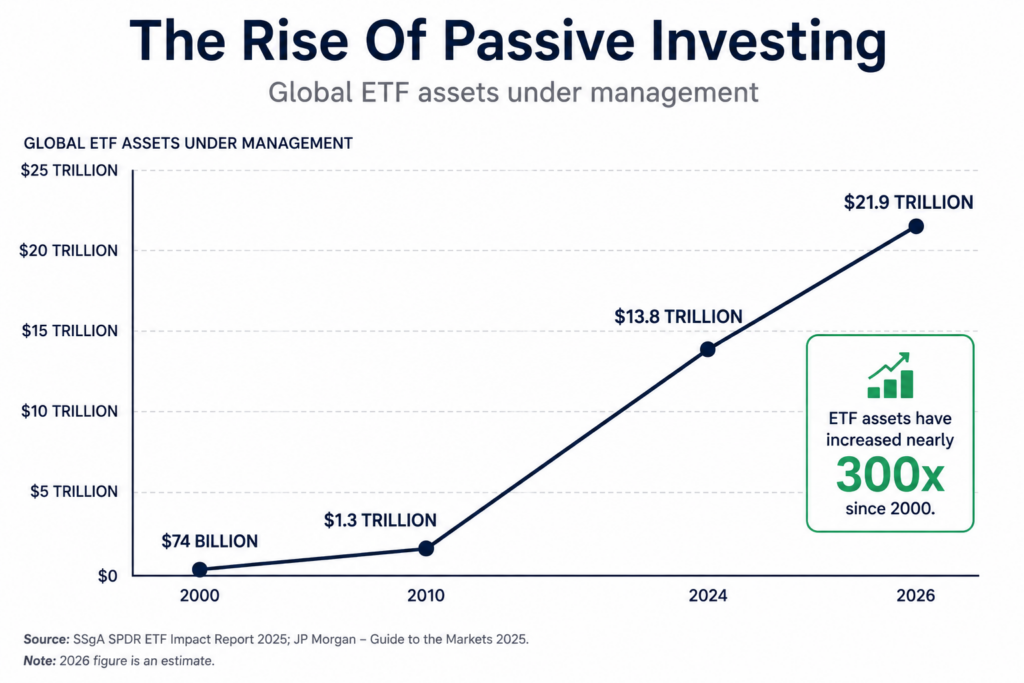

If you thought internet stocks were wildly overvalued, you could simply avoid buying them. Most of the speculation was concentrated in newly listed companies, and index investing and ETFs were still far from the dominant force it is today.

The AI boom changes things.

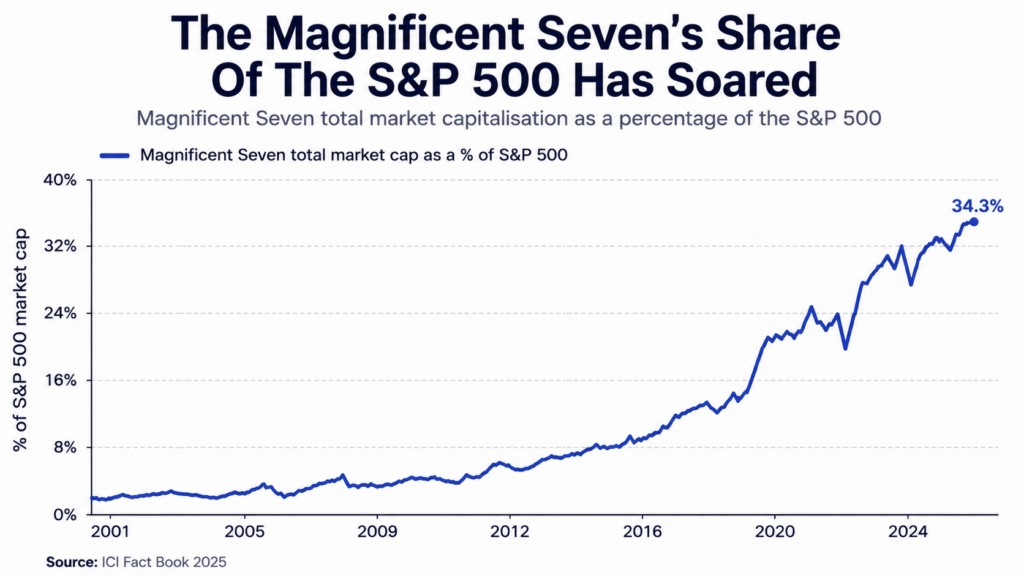

The companies making the largest bets on AI are also the largest companies in the market. Microsoft, Amazon, Google, Meta, Nvidia, Apple and Tesla collectively represent a significant share of major equity indices and retirement portfolios. The AI trade may become even harder to avoid with the likes of OpenAI, Anthropic and SpaceX eventually going public. And given their size, many would likely become major index constituents from the start.

In practical terms, that means investors often have exposure to the AI trade whether they intend to or not.

To avoid it entirely requires deliberately moving away from the very index funds that have become the default investment vehicle for millions of people.

That does not mean the risks are the same.

Unlike many dot-com companies, today’s technology giants generate enormous cash flows from established businesses. Even if their AI ambitions fall short, Microsoft is still Microsoft and Google is still Google.

But that also means a future correction could affect a much broader group of investors.

In 2000, many people chose to participate in the internet boom.

Today, many people will participate in the AI boom without even realising it.

That makes any potential downturn harder to isolate and harder to contain.

The Economy Has Less Room For Error

Another reason the dot-com crash proved surprisingly manageable was the condition of the broader economy.

During the late 1990s, the United States was running budget surpluses, household debt was relatively contained, unemployment was near historic lows, inflation was relatively low and overall growth was strong. Outside of technology stocks, there was plenty of productive economic activity supporting growth.

When the bubble burst, the economy still had legs to stand on.

Today’s environment looks very different.

Governments are running persistent deficits, debt ratio has exceeded GDP, the economy is more leveraged and economic growth has become increasingly concentrated in a small number of technology companies. Strip out the performance of the largest firms and much of the broader market looks far less impressive.

The concentration extends beyond financial markets.

The wealthiest households now account for an increasingly large share of consumer spending, much of which is influenced by the performance of investment portfolios and asset prices.

That creates a feedback loop.

If AI-related investments continue to drive market gains, spending remains strong. If those same investments suffer a significant correction, the impact may extend well beyond shareholders and technology companies.

Restaurants, retailers, contractors and countless other businesses ultimately depend on consumer spending generated elsewhere in the economy.

In that sense, the AI boom is not simply a technology story.

It has become increasingly intertwined with the broader economic system.

What Actually Pops A Bubble?

One of the most persistent myths about financial booms is that they end always end with a bust and with a single dramatic event.

In reality, they usually die from a thousand small disappointments.

The dot-com bubble did not collapse because investors suddenly realised internet companies were overvalued. Most people already knew valuations had become detached from reality. Alan Greenspan had warned of “irrational exuberance” years before the peak.

What changed was the flow of capital.

As interest rates rose and early investors began selling shares, funding became harder to obtain. Companies that had been relying on a steady stream of fresh capital suddenly found themselves unable to finance losses. One failure led to another, confidence evaporated and the bubble began to unwind.

The same pattern could emerge in AI.

It may not require a dramatic catalyst. A few quarters of disappointing returns on AI investments, a slowdown in data-centre construction or tighter lending standards from private credit markets and rate hikes from the fed could be enough to change sentiment.

The greatest risk facing speculative booms is rarely the technology itself.

It is the assumption that capital will always be available.

Once investors begin questioning whether the returns justify the spending, the flow of money that sustained the boom can disappear surprisingly quickly.

A Good Technology Is Not Always A Good Investment

The internet ultimately changed the world.

Yet that did not prevent a speculative bubble from forming around it. Investors correctly identified a revolutionary technology, but dramatically overestimated how quickly it would generate returns.

AI may follow a similar path.

The technology itself may prove transformative. Productivity could improve, industries could be reshaped, labour markets may change and entirely new business models could emerge. None of that guarantees that the trillions of dollars currently being invested will generate acceptable returns.

That is ultimately the lesson of the dot-com era.

Transformative technologies and speculative bubbles are not mutually exclusive. In fact, history suggests they often arrive together.

Whether today’s AI boom ends with a gentle correction or a more painful unwind remains impossible to predict. What is easier to observe is that the scale, leverage and concentration underpinning today’s market are significantly greater than they were a quarter-century ago.

The dot-com bubble left behind a digital economy.

The question investors must answer is whether today’s AI boom will leave behind something equally valuable.