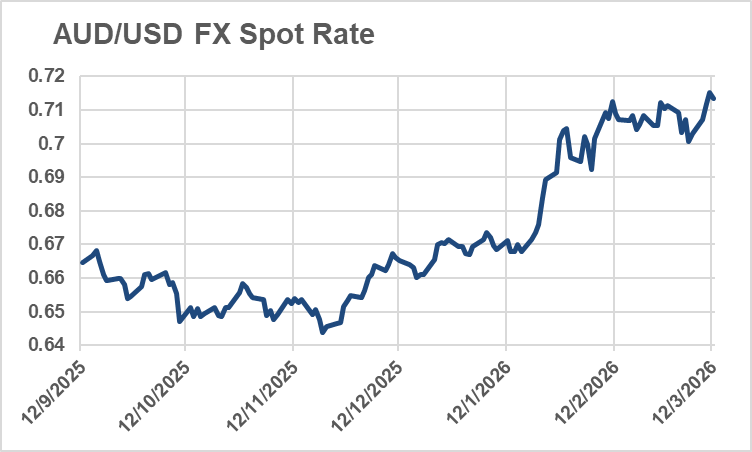

The Australian dollar has quietly become one of the strongest currencies in global markets. After several years of relative weakness, the currency is now trading near multi-year highs, climbing toward US72¢ as investors increasingly bet that Australia’s interest rates will move higher while much of the world prepares for cuts.

The move highlights a growing divergence in global monetary policy and reflects how quickly geopolitical events, commodity prices and central bank expectations can reshape currency markets.

For investors, the rise of the Australian dollar is more than a foreign exchange story. It is a signal about inflation risks, the outlook for interest rates and the relative strength of the Australian economy.

Interest Rate Expectations Are Driving the Currency

Currency markets are heavily influenced by interest rate expectations. When investors expect higher rates in a country, capital tends to flow toward its assets as global investors chase higher returns.

That dynamic is currently working in Australia’s favour.

Markets are increasingly convinced that the Reserve Bank of Australia will raise interest rates again in the coming months. Bond traders are now pricing an approximately 80 per cent probability of a rate increase at the next RBA meeting, with further tightening possible later in the year.

If those expectations are realised, the cash rate could rise to around 4.35 per cent, significantly higher than many investors expected just a few months ago.

This outlook stands in contrast with other major economies where central banks are still debating when they will begin cutting rates.

The result is widening interest rate differentials, a key driver of currency movements.

Australian two-year government bond yields have already climbed to roughly 4.5 per cent, opening a meaningful gap over comparable US and European bonds. Higher yields make Australian assets more attractive for global investors, which in turn supports demand for the currency.

Oil Prices Have Changed the Inflation Outlook

The catalyst for the shift in expectations has been the recent surge in oil prices.

Escalating conflict in the Middle East pushed crude prices toward US$120 per barrel earlier in the week as markets worried about potential disruptions to shipping through the Strait of Hormuz. The passage accounts for roughly 20 per cent of global oil supply, making it one of the most strategically important energy routes in the world.

Even though prices have eased since the initial spike, the shock has already altered the inflation outlook.

Higher energy prices quickly flow through to transportation costs, logistics and consumer goods. For central banks already concerned about inflation persistence, this creates a fresh policy dilemma.

Economists now expect the oil shock could push Australian inflation closer to 5 per cent, significantly above the RBA’s target of around 2.5 per cent.

That prospect has forced markets to reconsider the trajectory of monetary policy.

The RBA Is Becoming an Outlier Among Central Banks

Another factor strengthening the Australian dollar is the increasingly unusual position of the RBA within the global central banking landscape.

Many major central banks spent the past year discussing rate cuts as inflation eased and economic growth slowed. Australia has taken a different path.

The RBA already raised the cash rate earlier this year to 3.85 per cent, responding to an unexpected pickup in inflation during late 2025. If additional increases occur in the coming months, Australia could remain one of the few advanced economies still tightening monetary policy.

That divergence matters for currency markets.

Higher interest rates attract global capital flows into government bonds, bank deposits and other interest-bearing assets. When a central bank is moving in the opposite direction from its peers, the currency often benefits.

The current rally reflects precisely that dynamic.

The Aussie Is Rallying Across Multiple Currencies

The strength of the Australian dollar is not limited to its performance against the US dollar.

The currency has climbed to levels not seen in decades against the Japanese yen, reflecting the enormous gap between Australia’s interest rates and Japan’s near-zero policy settings.

It is also trading at multi-year highs against the euro, the British pound and the New Zealand dollar.

This broad-based strength suggests the rally is not simply about US dollar weakness. Instead, it reflects a shift in global capital flows toward Australian assets.

What a Stronger Dollar Means for Investors

A rising currency has mixed implications for the Australian economy and equity markets.

For consumers, a stronger dollar can be positive. Imported goods, overseas travel and foreign services become cheaper, which helps offset domestic inflation pressures.

Exporters, however, face the opposite dynamic. When the currency rises, Australian products become more expensive in global markets, potentially squeezing margins for companies that generate significant revenue overseas.

For investors, the impact depends largely on portfolio exposure.

Companies heavily exposed to international earnings may face headwinds from currency translation effects. On the other hand, sectors tied to domestic demand or benefiting from global capital flows could see support.

Currency strength also influences investment returns from international assets. When the Australian dollar rises, returns from overseas investments can decline once translated back into local currency

The Path Ahead for the Australian Dollar

Currency markets are notoriously difficult to predict, but the outlook for the Australian dollar will likely depend on three key variables.

The first is the trajectory of oil prices. If geopolitical tensions continue to disrupt energy markets, inflation risks could remain elevated and reinforce expectations of tighter monetary policy.

The second is the RBA’s policy response. If the central bank delivers multiple rate hikes, the yield advantage supporting the currency could strengthen further.

The third factor is global risk sentiment. The Australian dollar is often considered a “risk currency” due to its links to commodity demand and global economic growth.

If global markets stabilise and commodity demand remains strong, the currency could continue to climb.

Some strategists now believe the Australian dollar could reach US75¢ later this year if interest rate expectations remain firm.

For investors watching global macro signals, the message from the currency market is clear. Inflation risks are still shaping policy decisions, and Australia’s monetary stance is increasingly diverging from the rest of the developed world.

That divergence is now showing up in one of the most visible places in financial markets: the exchange rate.