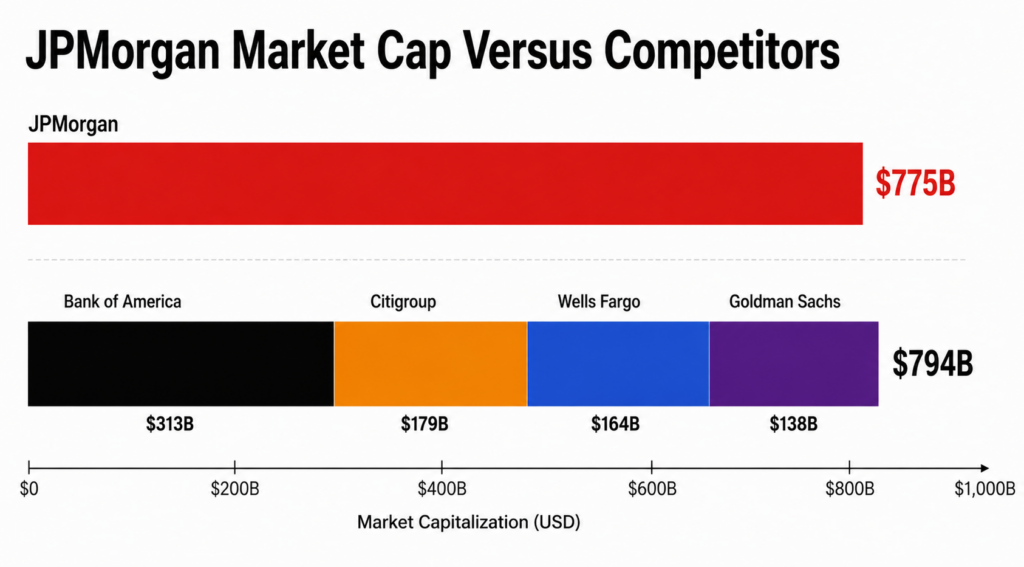

The name of the game in finance is scale, and no institution embodies that better than JPMorgan Chase.

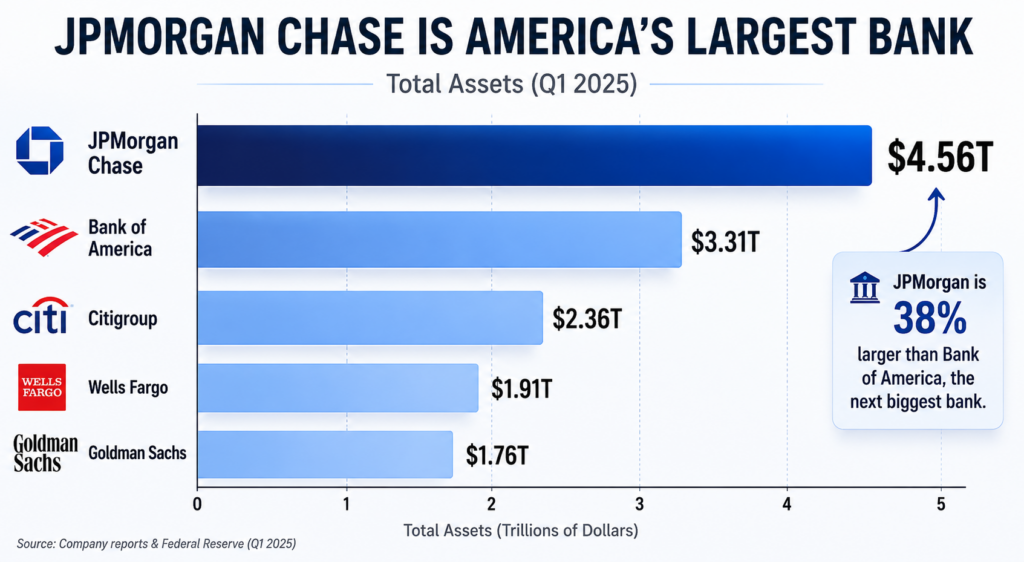

With a balance sheet of over $4.5 trillion, JPMorgan is the largest bank in the US and one of the most powerful financial institutions in the world. The bank holds around 20 per cent of all of the money in the American banking system and is more valuable than many of its largest rivals combined.

Its influence extends far beyond traditional banking and lending. JPMorgan advises on some of the world’s largest mergers and acquisitions, underwrites debt and equity offerings, manages trillions of dollars on behalf of clients and provides banking services to millions of households and businesses.

Last year, JPMorgan became the first bank in American history to beat $50 billion in profit. Yet its dominance cannot simply be explained just its size.

The bank’s rise has been driven by a combination of disciplined risk management, opportunistic acquisitions and over two decades of leadership under one of Wall Street’s most influential figures: Jamie Dimon.

So how did JPMorgan become the king of Wall Street?

The Power Of Scale

In banking, size is not just a measure of prestige. It is a competitive advantage.

A larger balance sheet allows a bank to make lend more and lend bigger, underwrite larger transactions and serve a broader range of clients. It also provides access to cheaper funding, stronger economies of scale and the ability to invest heavily in technology and infrastructure.

JPMorgan has spent decades building this advantage.

Today, the bank operates across consumer banking, investment banking, commercial banking, asset management and trading. Its clients range from households and small businesses to some of the world’s largest corporations and governments.

This diversification provides JPMorgan with a level of stability that many of its competitors lack. When one business line experiences a downturn, another can often offset the weakness.

For example, investment banking revenues may decline during periods of weak dealmaking activity, while consumer banking, credit card operations or wealth management can continue to generate substantial income.

The result is a financial institution that is not only larger than its rivals, but also more resilient.

Size alone does not explain JPMorgan’s dominance. One man led the bank’s rise, spending more than two decades transforming it into Wall Street’s undisputed heavyweight.

The Jamie Dimon Era

While JPMorgan’s history stretches back more than two centuries, much of its modern success is tied to one man whose name echoes Wall Street and global finance: Jamie Dimon.

Dimon became CEO in 2006 and has since become one of the most respected and influential figures in global finance. He has overseen JPMorgan’s transformation into the dominant force on Wall Street.

Unlike many banking executives, Dimon built a reputation not only for growing the bank, but for avoiding the kinds of mistakes that have brought down competitors.

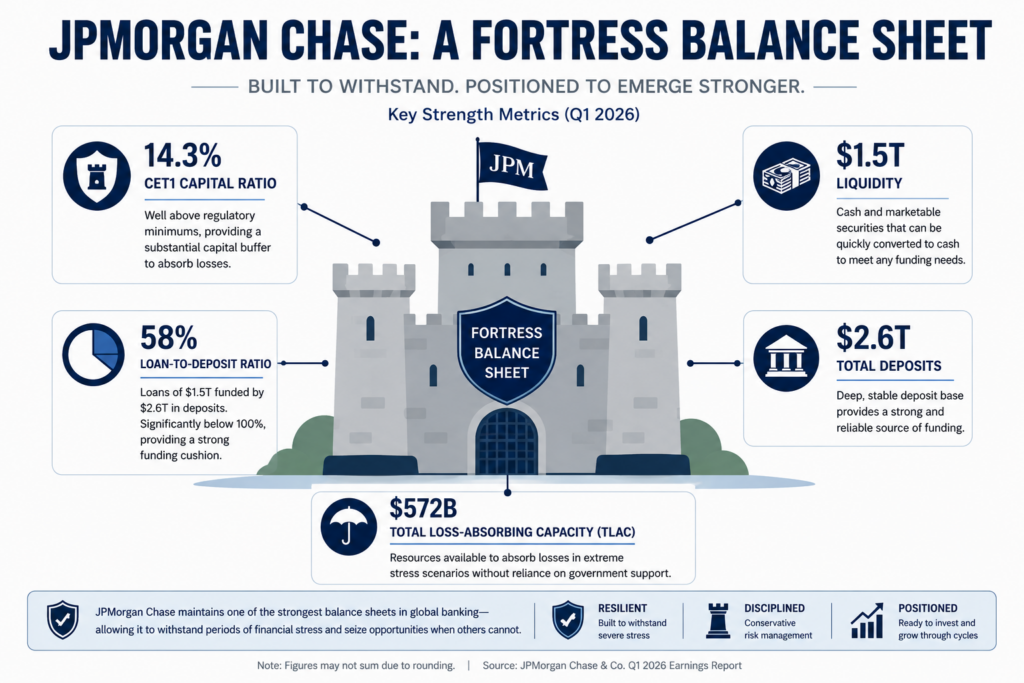

At the centre of his philosophy is what he often refers to as a “fortress balance sheet”, maintaining sufficient capital, liquidity and risk controls to ensure the bank can withstand even the most severe economic shocks.

This focus on resilience has helped JPMorgan navigate everything from the GFC and COVID-19 to the regional banking crisis of 2023.

Dimon has also become one of the most influential voices in American business. Investors, policymakers and executives closely read his shareholder letters, and his views on economic policy, regulation and geopolitics frequently generate headlines.

Over time, he has evolved beyond the role of bank CEO and into something closer to a statesman of American finance.

Yet perhaps the most impressive aspect of Dimon’s time is not that JPMorgan survived periods of turmoil.

It is that the bank often emerged from them larger and stronger than before.

The JPMorgan Secret: Winning Crises

One of the most remarkable aspects of JPMorgan’s rise is that many of the events that damaged its competitors, strengthened the bank.

While financial crises are typically associated with bankruptcies, bailouts and market panic, JPMorgan has repeatedly used periods of turmoil to expand its business and increase its market share.

Bear Stearns (2008)

The first major example came during the GFC.

In March 2008, investment bank Bear Stearns faced a liquidity crisis that threatened its survival. Fearing broader contagion throughout the financial system, US regulators helped facilitate a takeover by JPMorgan.

Acquiring Bear Stearns expanded JPMorgan’s investment banking and trading operations, strengthening its position on Wall Street. What began as a financial rescue ultimately became a transformative acquisition for the bank.

Washington Mutual (2008)

Later that same year, JPMorgan acquired Washington Mutual after it declared insolvency, resulting in the largest bank failure in American history.

The transaction dramatically increased JPMorgan’s retail banking footprint and deposit base, giving the bank greater scale across consumer banking and helping cement its position as America’s leading financial institution.

Together, the Bear Stearns and Washington Mutual acquisitions reshaped JPMorgan. The bank that emerged from the Global Financial Crisis was significantly larger and more diversified than the one that entered it.

First Republic (2023)

JPMorgan benefited from another crisis more than a decade later.

In 2023, First Republic Bank collapsed amid turmoil in the US regional banking sector. Despite existing rules designed to limit further concentration in the banking system, regulators once again approved a JPMorgan acquisition.

The deal added billions of dollars in deposits and loans while strengthening JPMorgan’s position among affluent clients and private banking customers.

Coming Out Stronger

A clear pattern emerges from these episodes.

While weaker institutions scrambled for emergency mergers, accepted bailouts or collapsed altogether, JPMorgan leveraged its financial strength to become a buyer of last resort.

Rather than simply surviving crises, the bank often used them as opportunities to acquire valuable assets, expand its customer base and increase its market share.

In many ways, JPMorgan’s dominance was not built despite financial crises. It was built through them.

The Fortress Balance Sheet

At the centre of JPMorgan’s success is a philosophy that Jamie Dimon has championed throughout his career: the fortress balance sheet.

The concept is simple. Rather than optimising solely for short-term profits, JPMorgan prioritises maintaining sufficient capital, liquidity and risk controls to withstand shocks and crises. The goal is not merely to survive periods of stress, but to emerge from them in a position of strength.

This approach has shaped the bank’s culture for nearly two decades.

The bank regularly conducts extensive stress testing, modelling scenarios ranging from deep recessions and market crashes to geopolitical shocks and financial crises. By preparing for worst-case outcomes, the bank seeks to ensure it can continue operating even when competitors come under pressure.

The strategy has not made JPMorgan immune to mistakes.

The bank suffered a multi-billion-dollar trading loss during the 2012 “London Whale” incident and has faced various controversies throughout Dimon’s tenure. Yet these setbacks have generally been viewed as manageable because of the institution’s sheer financial strength.

This resilience helps explain why JPMorgan has so often emerged as a consolidator and helper during periods of turmoil. While other institutions focus on survival, JPMorgan is frequently in a position to help the US Government and acquire assets, customers and entire businesses.

The fortress balance sheet has therefore become more than a risk management strategy. It has become one of JPMorgan’s most important competitive advantages.

The Biggest Question Facing JPMorgan

Despite its size, profitability and dominance, JPMorgan faces a challenge that no balance sheet can solve.

Dimon will eventually step down.

After over two decades as CEO, the noe 70-year old Dimon has become synonymous with JPMorgan itself. His leadership has guided the bank through the GFC, COVID-19 and banking crises, while helping transform it into the most powerful financial institution in the United States.

As a result, many investors believe JPMorgan benefits from the “Jamie Dimon premium”, the confidence that comes from having one of the world’s most respected figures as its leader.

This creates what investors often refer to as key-man risk.

While JPMorgan’s management team is widely regarded as one of the strongest in corporate America, replacing a CEO who’s so iconic and has shaped the organisation for over 20 years is no easy task. Several potential successors have come and gone over the years, while current contenders continue to be closely watched by investors and analysts.

1 man remains the same. Source: WSJ.

The challenge is not simply finding someone capable of leading a bank.

It’s finding someone capable of running the biggest bank JPMorgan.

Whoever eventually succeeds Dimon will inherit an empire with trillions of dollars in assets, operations spanning the globe and a central role in the stability of the American financial system.

The story of JPMorgan has been inseparable from Jamie Dimon’s for over 20 years.

The question facing Wall Street isn’t will the now 70-year old Dimon step down soon.

It’s whether the bank can maintain its dominance once the man who built it finally steps aside.