Former Prime Minister Paul Keating has urged Labor to resist pressure for major carve-outs to its proposed capital gains tax (CGT) reforms, arguing the reforms are needed to improve housing affordability and to fix a distortion in the tax system.

Keating described the reforms as “structurally sound” and criticised what he called the “howls” of wealthy investors seeking to preserve their concessions and preferential tax treatment.

But Keating’s support for the reforms is not simply about tax policy.

It reflects a broader economic philosophy that he used to shape much of Australia’s modern tax system during his time as Treasurer and Prime Minister from 1983 to 1996.

Keating’s comments carries particular weight as he was the architect of Australia’s CGT system. As Treasurer in the Hawke Government, Keating introduced the Capital Gains Tax in 1985 as part of a broader program of economic reform designed to improve the efficiency and fairness of the tax system.

The aim was to reduce reliance on income tax, increasing the breadth of the tax system and tax avoidance through shifting and to restore fairness into the tax system, as he said in a 1989 question in parliament, “Why should somebody who gets his income from buying or selling property or shares pay no tax while millions of ordinary wage and salary earners automatically pay their tax each week?… (There was) a whole tax avoidance industry which tried to turn all forms of income into capital gains type income so as to escape taxation.”

More than forty years later, many of the same arguments continue to underpin the debate surrounding Labor’s proposed reforms.

What Are The Tax Reforms?

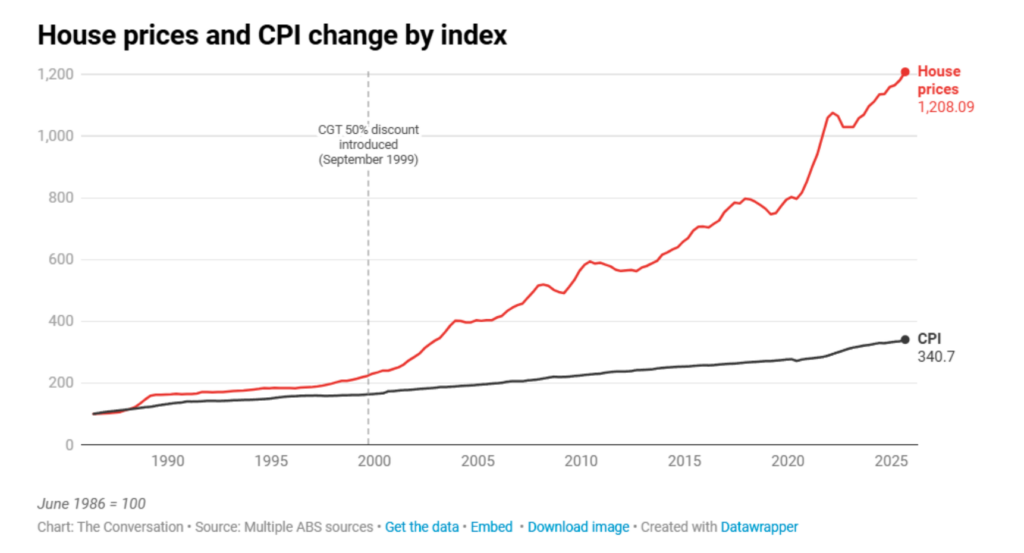

Under the current system, individuals who hold an asset for more than 12 months receive a 50 per cent discount on any capital gain, halving their taxable income. The Howard–Costello Government introduced the discount in 1999, replacing the original indexation system introduced under Keating.

Labor’s proposed reforms would move away from the blanket 50 per cent discount and instead return to Keating’s system based on indexation. Instead of automatically exempting half of a capital gain from tax, the government would tax investors only on gains above inflation.

Another aspect of the reform is a 30% minimum tax on CGT, knocking off the tax-free threshold and the currently 16% bracket.

Critics, however, argue the changes could reduce investment, discourage entrepreneurship and lower after-tax returns for investors.

Why Keating Supports The Tax Changes

Keating’s support for the reforms stems from the same principles that motivated the introduction of the CGT 4 decades ago: economic efficiency, tax neutrality and fairness.

In Keating’s view, tax systems should minimise distortions and allocate capital toward productive investment rather than encouraging speculation.

He has argued that the current CGT disproportionately benefits existing asset holders while encouraging investment into housing and other capital assets over more productive areas of the economy.

Housing Affordability

One of Keating’s primary concerns is housing affordability.

Critics of the current system argue that the combination of negative gearing and the 50% discount has incentivised investors to purchase existing housing stock. By increasing investor demand, these policies may contribute to higher house prices and make it more difficult for first-home buyers to enter the market.

Keating has argued that tax settings should not unnecessarily favour existing asset ownership at the expense of younger Australians attempting to purchase a home.

Keating has argued that the changes contributed to a dramatic increase in housing prices relative to incomes. He recently noted that house prices rose from roughly nine times income to sixteen times income over the following decades, arguing the tax system increasingly favoured existing asset owners over prospective homebuyers.

Productive Investment

Keating has also long argued that capital should flow toward productive investment rather than speculative gains.

Supporters of the reforms argue that preferential treatment of capital gains can distort investment decisions by making asset appreciation more attractive than investment in businesses, innovation and productive enterprise as well as incentivise people to shift income into capital gains type income to minimise tax.

From this perspective, reducing the preferential treatment of capital gains may improve the allocation of capital throughout the economy.

Tax Fairness

Finally, Keating views the reforms as a question of tax fairness.

The original rationale for capital gains tax was that individuals earning income through capital appreciation should not enjoy substantially different tax treatment to those earning income through wages and salaries.

While the current debate centres on the appropriate level of taxation, Keating’s position remains broadly consistent with the argument he made when introducing the tax in the 1980s: similar forms of economic gain should be treated similarly by the tax system.

Critics Remain Concerned

Despite Keating’s support, the changes have attracted criticism from startup founders, VC investors, property groups and sections of the broader business community. Critics argue the changes could reduce incentives to invest in early-stage companies, lower after-tax returns and make Australia a less attractive destination for entrepreneurial capital.

Keating has pushed back strongly against these claims. He argues that genuinely productive investment is driven primarily by the quality of the underlying opportunity.

In his view, the reforms do not remove the ability to generate strong returns from successful investments, but instead reduce a distortion that has encouraged capital to flow towards existing assets and tax-advantaged gains.

Supporters of the reforms make a similar argument. They note that Australia operated under an indexed capital gains tax system from 1985 until 1999 while continuing to attract investment, entrepreneurship and economic growth and in fact seeing a boom in all 3.

From this perspective, the debate is not whether investment should be rewarded, but whether the tax system should continue to provide preferential treatment to one particular form of income.