If you stand at the Port of Los Angeles, you can see thousands of shipping containers stacked as far as the eye can see.

Inside them are the products that power the global economy and global trade. Smartphones, televisions, clothing, furniture, car parts and industrial machinery all move around the world inside these standardised steel boxes.

They’re so common that most people never stop to think about who builds them.

Yet if you walk up to almost any shipping container and see the small metal identification plate attached to its doors, you will notice something remarkably consistent.

Despite the dozens of different logos painted on the side, most containers originate the same 3 manufacturers.

One of 3 Chinese companies, CIMC, Dongfang and CXIC, combined they build well over 80% of the world’s shipping containers. China alone accounts for 96% of global dry cargo container production and effectively 100% of refrigerated containers.

In other words, the physical infrastructure of global trade is overwhelmingly manufactured in 1 country and just 3 companies.

This raises an obvious question, how did 3 companies come to dominate one of the most important industries on Earth?

The Physical Shape Of Globalisation

The modern shipping container is one of the most important inventions of the last century.

Before containers, cargo was loaded and unloaded manually by hand. Goods arrived at ports in boxes, barrels, sacks and crates, each requiring individual handling. The process was slow, expensive and prone to damage.

That changed in 1956 when Malcolm McLean launched the Ideal X, the first commercially successful container ship. By standardising cargo into steel boxes that could be transferred seamlessly between ships, trains and trucks, McLean dramatically reduced shipping costs and helped lay the foundations for modern globalisation.

Today, about 90% of world trade moves by sea, with the vast majority travelling inside shipping containers.

As global trade expanded, container manufacturing followed the world’s industrial centres.

Production initially began in the US before gradually shifting to Japan during the 1960s. By the 1970s and 1980s, South Korea had become a major manufacturing hub. Eventually, by the 1990s, container production had migrated almost entirely to China.

At first glance, this appears to be a familiar story of manufacturers chasing lower labour costs.

The reality is far more interesting.

China’s dominance is not simply the result of cheaper workers. It is the result of an industrial ecosystem so large and efficient that competing elsewhere has become extraordinarily difficult.

Why No One Else Can Compete With Chinese Shipping Monopoly

It’s easy to attribute China’s dominance to cheap and vast labour.

But shipping containers aren’t labour-intensive products.

A standard 40-foot container is just a large steel box. Roughly 60% of production cost comes from the steel itself, meaning the economics of container manufacturing are heavily influenced by access to raw materials rather than labour costs.

This is where China’s advantage becomes overwhelming.

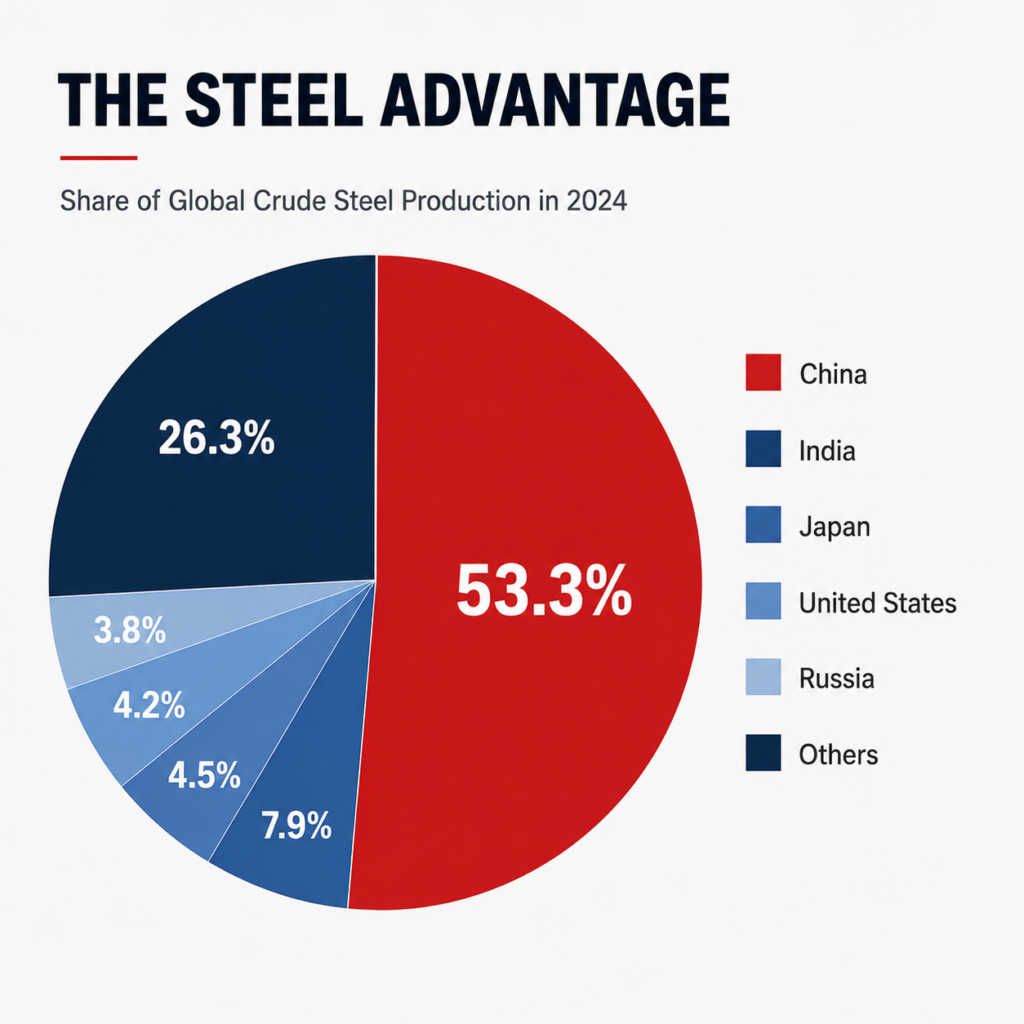

Source: World Steel

In 2024, China produced more steel than the rest of the world combined, accounting for over half of global output. Its steel industry is larger than US, Japan and Russia combined. The sheer scale of this production allows Chinese manufacturers to source materials more efficiently and at lower cost than competitors almost anywhere else in the world.

The challenge for potential rivals extends beyond steel.

Imagine a manufacturer attempting to build containers in Europe or North America. In many cases, they would first need to import Chinese steel, potentially pay tariffs, manufacture the container, and then ship the finished box back to Asia, where most global manufacturing activity occurs.

The economics quickly become difficult to justify.

After all, containers exist to transport goods, and China remains the world’s largest manufacturing centre and largest exporters. Producing containers close to where those goods are made creates a powerful advantage that is difficult for overseas competitors to replicate.

In many ways, the geography of container manufacturing is dictated by the geography of industrial production itself.

The result is a self-reinforcing cycle. China produces the steel, manufactures the goods, builds the containers and exports the products. Every stage of the supply chain strengthens the next.

This is why China’s position has proven so resilient.

Competing with Chinese container manufacturers is not simply a matter of building a better box. It requires replicating an industrial ecosystem that has been developing for decades.

Meet The Big Three

While thousands of companies operate within the global shipping industry, container manufacturing is remarkably concentrated.

Today, three firms sit at the centre of the industry: CIMC, Dongfang and CXIC. Together, they account for more than 80% of global container production and effectively dictate the capacity of the industry.

CIMIC: The Industry Titan

The undisputed leader is China International Marine Containers (CIMC).

Founded in Shenzhen in 1980 as a joint venture involving Chinese and Danish interests, the company has grown into one of the world’s largest industrial manufacturers. In 2024, CIMC reported record revenue of more than US$24 billion while selling nearly 3.5 million containers as global trade rebounded.

Its scale is difficult to comprehend.

If two shipping containers are sitting side-by-side in a port anywhere in the world, there is a good chance that one of them was built by CIMC. The company controls roughly half of the global market, making it the dominant force in container manufacturing.

Dongfang: The Quiet Giant

The second-largest player is Dongfang International Container.

While far less well known outside the shipping industry, Dongfang controls an estimated 25% to 30% of the global market. The company has become a major supplier to some of the world’s largest shipping lines and plays a critical role in maintaining global container supply.

CXIC: Completing The Oligopoly

The third major player is CXIC.

Although smaller than its two larger rivals, the company still commands an estimated 10% to 15% of the market. Together, the three firms form an oligopoly that few industries can match.

For prospective competitors, the challenge is obvious.

They are not competing against a single dominant company. They are competing against three highly scaled manufacturers operating within the world’s largest industrial ecosystem.

And those companies are becoming more efficient every year.

The Regulation That Strengthened The Shipping Monopoly

Perhaps the most surprising factor behind the industry’s consolidation was an environmental regulation.

In 2017, the Chinese government mandated a transition from traditional oil-based paints to water-based alternatives in an effort to reduce air pollution and volatile organic compound emissions. While the policy was primarily designed to improve environmental outcomes, it had an unintended consequence for the container industry.

The switch required manufacturers to invest heavily in new equipment, drying systems and humidity-controlled production facilities. For smaller container producers, the cost of upgrading proved prohibitive.

Many simply could not afford it.

The industry’s largest players, however, faced a very different reality. Backed by greater scale, stronger balance sheets and easier access to financing, companies such as CIMC, Dongfang and CXIC were able to modernise their facilities and continue operating. As smaller rivals disappeared, market share became increasingly concentrated in the hands of the industry’s dominant firms.

In effect, a regulation intended to reduce pollution also accelerated consolidation.

The result was an industry that became even more difficult for new entrants to challenge.

Ironically, the same scale that had allowed the largest manufacturers to dominate production also allowed them to adapt to changing regulations more easily than their smaller competitors. The barriers to entry grew higher, while the number of meaningful competitors continued to shrink.

By the end of the decade, the dominance of the big three had become even more entrenched.

But to think of these companies as mere container manufacturers would be a mistake.

The container business is only one part of a much larger industrial empire.

More Than Container Companies

The dominance of the big three becomes even more remarkable when you realise that containers are only one part of their business.

Take CIMC.

While it is best known for manufacturing shipping containers, the company has evolved into a sprawling industrial conglomerate with operations spanning transportation, logistics, energy and infrastructure.

The next time you board an aircraft, there is a good chance the passenger boarding bridge connecting the terminal to the plane was manufactured by CIMC Tianda, one of the group’s subsidiaries. The company is one of the world’s largest suppliers of airport equipment and operates in airports across the globe.

Its reach extends far beyond aviation.

During the COVID-19 pandemic, CIMC helped construct modular quarantine facilities in Hong Kong using prefabricated building systems. Entire rooms arrived with plumbing, electrical systems and fittings already installed, allowing large-scale facilities to be assembled in a matter of weeks rather than months.

The company also manufactures offshore oil and gas infrastructure, owns the German fire truck manufacturer Ziegler, and operates across a range of industrial sectors that most consumers never associate with the CIMC name.

This diversification provides an important advantage.

While container demand can fluctuate alongside global trade, these broader industrial businesses generate additional revenue streams and allow the company to invest through economic cycles.

In many ways, container manufacturing is merely the foundation upon which a much larger industrial empire has been built.

And that raises one final question.

If global manufacturing continues to expand into countries such as Vietnam and India, could container production eventually follow?

Could Anyone Challenge The Big Three?

As manufacturing expands into countries such as Vietnam and India, it is tempting to assume container production will eventually follow.

But scale remains the decisive advantage.

Building a container factory is relatively straightforward. Replicating China’s steel production, supply chains, logistics infrastructure and decades of manufacturing expertise is not. While emerging manufacturing hubs continue to grow, the gap remains enormous.

That does not mean China’s dominance will last forever. Container manufacturing has already migrated from the United States to Japan, South Korea and eventually China. History suggests future shifts are possible.

For now, however, the industry’s centre of gravity remains firmly in China.

The next time you see a shipping container, there is a very good chance it was built by one of just three companies.

Few monopolies are as hidden.

And few are as important.