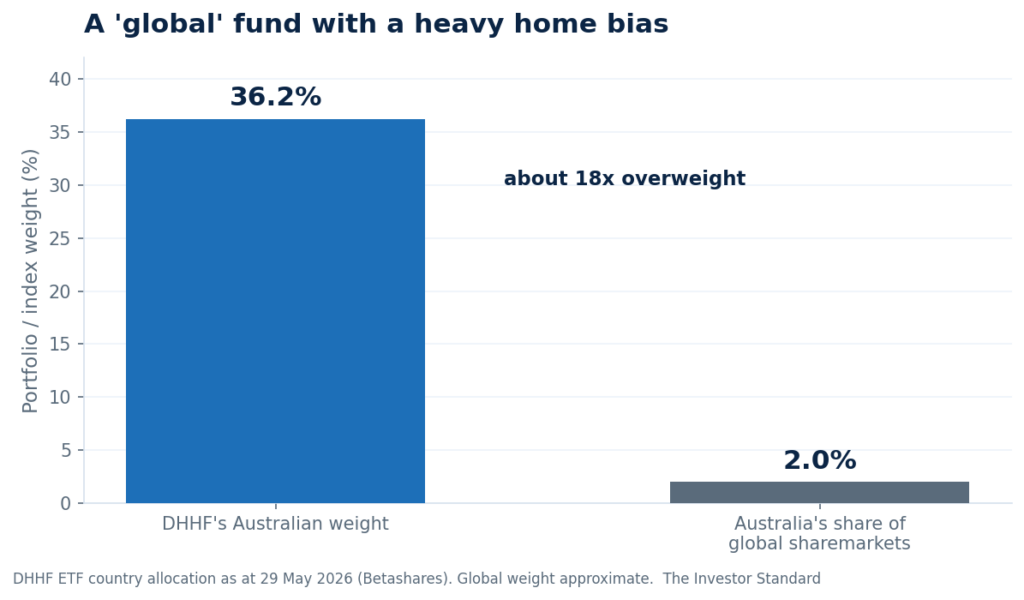

One ticker, around 8,000 companies, more than 60 exchanges. The DHHF ETF is pitched as the entire world bought in a single ASX trade. Then you check the map. As at 29 May 2026, 36.2% of the fund was invested in Australia, a market worth roughly 2% of global shares. That is not a rounding error. It is the whole story.

Where the money actually sits

The Betashares Diversified All Growth ETF (ASX: DHHF) is the cheapest all-in-one growth fund on the local market, charging 0.19% a year. It holds nothing directly. Instead it blends four underlying index funds: Betashares’ Australia 200 ETF, a Vanguard total US sharemarket fund, and two SPDR funds covering developed markets outside the US and emerging markets. Stack them together and you get exposure to about 8,000 stocks, 100% in equities, no bonds, no cash. The pitch writes itself. Buy the planet, set, forget.

The geography is where the pitch and the portfolio part ways. The United States takes 42.4% of the fund. Australia takes 36.2%. After that the drop is a cliff: Japan 3.7%, then Taiwan, South Korea, China, Canada and Britain, each under 2%. So two countries hold nearly four-fifths of a fund whose selling point is breadth. The Australian slab is set deliberately. Betashares runs a strategic target near 37% for domestic shares and reviews it once a year. This is a house decision, not a quirk of market weights.

What DHHF ETF is really betting on

Start with the gap. A portfolio that simply matched global market values would put about 2% in Australia. DHHF puts 36%. That is close to an eighteen-fold overweight, and it is the single largest active position in the fund. Nobody markets it that way, because “diversified” and “all-world” do the talking.

Now look through to the stocks. The Australian sleeve tracks the ASX 200, where Commonwealth Bank alone is around 12% of the index and the big four banks plus BHP dominate the top. Run the arithmetic: 12% of a 36% Australian weight puts CBA at roughly 4% of the entire DHHF ETF. That is an estimate, not a published figure, but it is hard to avoid. It very likely makes a single Australian bank the largest holding in a fund sold as the whole world, ahead of Nvidia, Apple or Microsoft. The reason is structural. The US sleeve uses a total-market index of about 3,500 names, which spreads the American mega-caps thin, while the Australian sleeve funnels a third of the fund into a top-heavy index of 200.

Then there is the price of that bet. CBA traded on about 28 times trailing earnings in mid-June 2026, against a five-year average closer to 22 times, an unusually rich multiple for a mature bank in a low-growth economy. So the home tilt does not just concentrate you in Australia. It concentrates you in Australian banks at the top of their valuation range. Pair that with a US sleeve dominated by mega-cap technology and DHHF starts to look like two of the most crowded trades on earth, stitched together and sold as neutrality.

The numbers

| Metric | DHHF | Why it matters |

|---|---|---|

| Management fee | 0.19% p.a. | Cheapest all-in-one growth ETF locally |

| Australian equities | 36.2% | Versus roughly 2% global weight: the active bet |

| US equities | 42.4% | Mega-cap technology does the heavy lifting |

| Holdings | ~8,000 via 4 ETFs | Genuine breadth at the stock level |

| 12-month distribution yield | 2.2% (2.7% franked) | Franking is part of the home-bias case |

| 1-year total return | 14.50% | Recent performance, net of fees |

| 5-year total return (p.a.) | 10.36% | The long-run record |

Allocation and yield as at 29 May 2026. Performance as at 30 April 2026. Source: Betashares. CBA index weight and valuation as at mid-June 2026 from Market Index and Investing.com. Past performance is not indicative of future performance.

Why BetaShares tilts to Australia

The home bias is not lazy, it is a choice with a rationale. Franking credits are the first reason: the fund’s yield lifts from 2.2% to 2.7% once franking is counted, and those credits only have value to Australian taxpayers, so a global-neutral fund would leave them on the table. The second is currency. Holding 36% in Australian dollars softens the swing a local investor feels when the Aussie moves against the US dollar. The third is plain behaviour. Investors stay the course more easily in names they recognise. None of that is wrong. It is just active asset allocation wearing a passive badge.

Where it bites

A domestic shock, a housing wobble, a bank earnings reset, a resources downturn, lands on more than a third of the fund at once. The concentration in CBA and the banks means a single richly priced sector carries outsized weight. And there is the overlap problem. Most Australians already own these same banks, through direct holdings, through their super, sometimes through both. Buy DHHF on top and you may be tripling down on Australia without ever deciding to.

Investor takeaway

For a young accumulator who wants franking, earns and will retire in Australian dollars, and holds little else, a 36% home weight is defensible. It might even be the right call. The mistake is not the tilt. The mistake is not knowing it is there, and reading “all-world” as “market-neutral”. DHHF is a house view: heavy Australia, heavy US, light on everything in between.

What would change the read. If Betashares trimmed the Australian target toward global weights, or if the ASX broadened beyond banks and miners, the home-bias critique would soften. Neither looks close. Until then, treat the DHHF ETF as an active allocation decision in passive clothing, and before you buy more, check how much Australia, and how much CBA, you already own everywhere else.