CEO of Pershing Square Capital Management Bill Ackman has spent years trying to increase his exposure to Universal Music Group (UMG).

Now, the world’s largest music company has formally rejected his latest attempt.

On Friday, UMG unanimously declined an unsolicited takeover proposal from Ackman’s Pershing Square Capital Management that valued the company at US$65 billion. UMG’s board arguing that the proposal undervalued the business and wouldn’t deliver superior value for shareholders.

But the more interesting question is not why the deal failed.

It is why one of the world’s most prominent investors wanted to buy the world’s largest music company in the first place.

What Is Universal Music Group?

UMG is the world’s largest music company.

The company represents some of the biggest artists on eatth, including Taylor Swift, Drake, Kendrick Lamar, Billie Eilish and many others. Through its labels, publishing operations and music catalogues, UMG controls more than one-third of the music industry globally.

This makes UMG one of the “Big Three” labels along side Sony Music Entertainment and Warner Music Group.

Source: Universal Music Publishing Group

While many investors associate technology companies with recurring revenue and strong IP, the modern music industry increasingly possesses many similar characteristics.

Why Music Has Become Such An Attractive Business

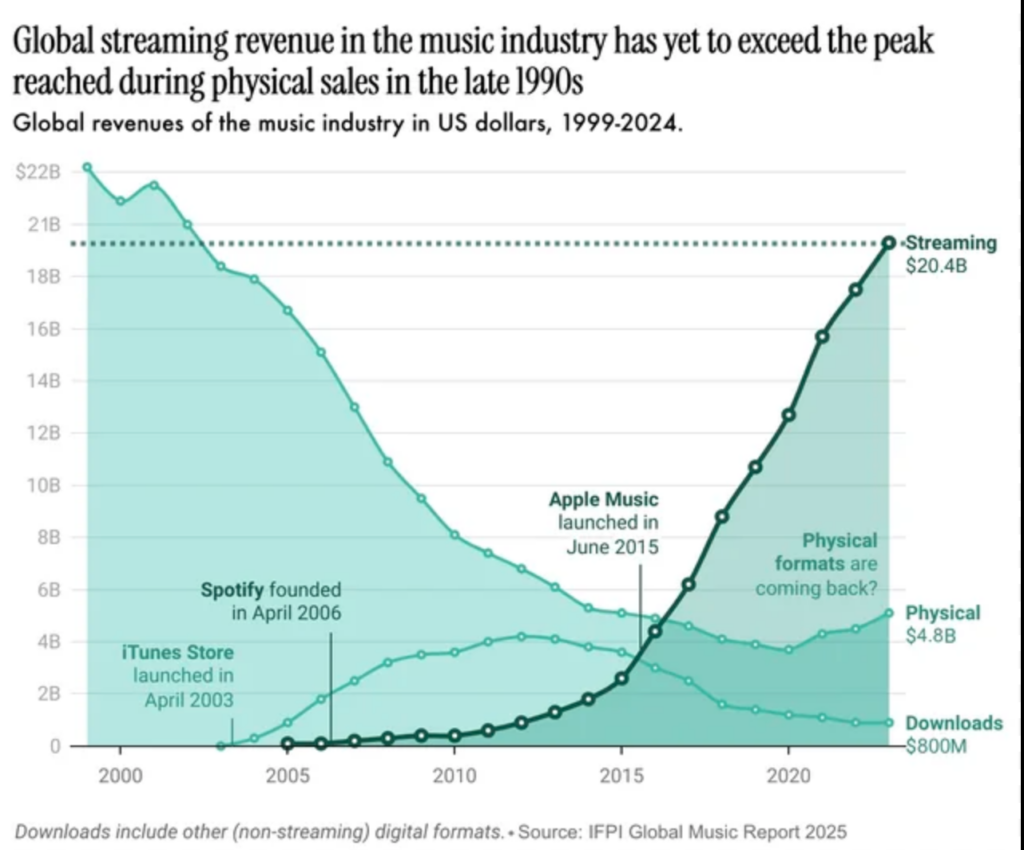

At the beginning of the century the music industry struggled with piracy and declining physical sales.

Then streaming came along.

Instead of relying on one-off purchases, music companies now generate recurring revenue through subscription services from the likes of Spotify, Apple Music and YouTube Music.

Every time a user streams a song, royalties are generated.

This creates a business model where intellectual property (IP) can continue generating cash flows for years, and even decades, after its initial release. Older songs can continue generating royalties decades after their initial release, making music catalogues particularly attractive to long-term investors.

Unlike many other industries, the marginal cost of distributing an additional song to millions of listeners is effectively zero.

Once a catalogue is created, it can continue generating revenue globally without requiring significant additional costs for things like production.

For many investors, this makes music IP and rights increasingly resemble long-duration financial assets.

Ackman’s Investment Thesis

Ackman’s argument was not that UMG was a weak business but the opposite.

He argued that the company’s share price weakness was largely unrelated to its underlying operations. Despite strong industry fundamentals, UMG’s shares have significantly underperformed over the past year.

Pershing Square’s proposal would have shifted UMG’s primary listing from Amsterdam to New York, potentially increasing its visibility among investors in the US and allowing greater inclusion in US equity indices.

Ackman’s thesis was essentially that the market was undervaluing one of the world’s strongest IP businesses.

Why The Deal Failed

The biggest obstacle was never the financing but ownership.

UMG’s largest shareholder, the Bolloré Group, publicly opposed the transaction, arguing the offer significantly undervalued the company. Cyrille Bolloré also questioned the structure of the proposal and Ackman’s management approach.

Without Bolloré’s support, Ackman himself acknowledged that a transaction would be extremely difficult to complete.

The board ultimately sided with that view and rejected the takeover bid.

The Bigger Lesson

The failed takeover highlights a broader shift taking place across the global economy.

Some of the world’s most valuable assets are no longer physical things such as factories, oil fields or industrial infrastructure.

But instead IP.

Songs, brands, software, networks and digital platforms increasingly generate enormous and recurring streams of cash and income.

Bill Ackman’s pursuit of UMG reflects this reality.

The battle was never really about music.

It was about ownership of one of the world’s most valuable collections of IP.