In 2025, Jane Street generated US$39 billion in trading revenue.

That figure exceeds the trading revenue generated by many of Wall Street’s largest banks, including, JP Morgan Goldman Sachs, Morgan Stanley and Bank of America.

Despite its enormous size, many investors have never heard of the firm.

Unlike traditional financial institutions, Jane Street has no celebrity CEO, rarely gives interviews and reveals little about how it operates. The company does not manage wealth for retail investors, advise on mergers or underwrite public offerings. Instead, it quietly sits at the centre of modern financial markets, facilitating trades and exploiting tiny pricing discrepancies across thousands of securities around the world.

Over the past decade, this approach has transformed Jane Street from a niche trading firm into one of the most profitable financial institutions on the planet.

So how did a relatively unknown company become one of the most powerful firms on Wall Street?

What Is Jane Street?

Founded in 2000, Jane Street is a quantitative trading firm and market maker headquartered in NYC.

Unlike traditional banks, its primary business is not lending money or providing financial advice. Instead, Jane Street specialises in buying and selling financial instruments while profiting from small differences in prices across markets.

Today, the firm trades a vast range of products including equities, bonds, ETFs, options, FX and commodities futures.

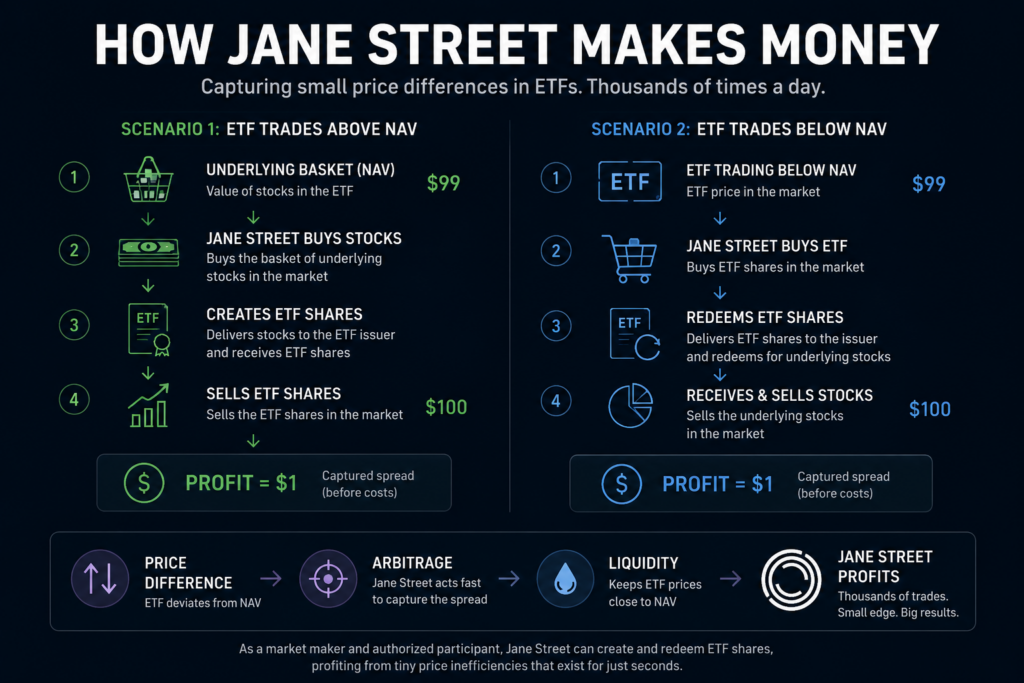

At the heart of its business is market making.

Whenever an investor buys or sells a security, someone must stand ready to take the opposite side of the trade. Jane Street performs this function on a massive scale, continuously quoting prices and providing liquidity and price discovery to the market.

In exchange, the firm earns the spread between buying and selling prices.

On a single trade the profit may be tiny. Add it up across millions of transactions every day and the profits quickly add up.

The ETF Opportunity

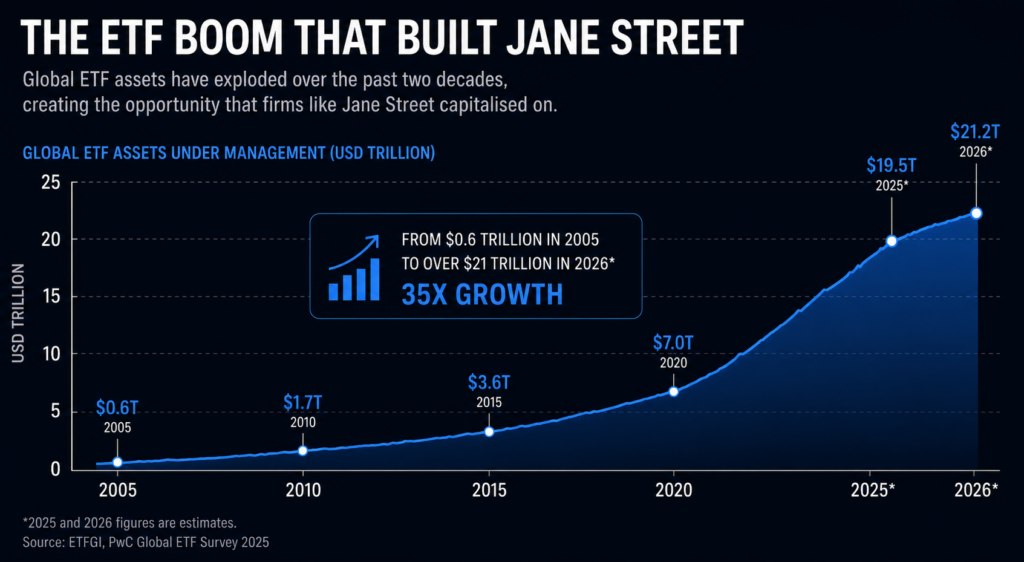

While market making has existed for decades, Jane Street’s rise coincided with a massive structural shift in modern investing: the ETF boom.

ETFs allow investors to purchase a diversified basket of assets through a single security. Over the past 20 years, their popularity has surged as investors have increasingly moved away from traditional active funds and toward lower-cost passive investment products.

As a result of this shift, trillions have flowed into ETFs.

Today, ETF trading volume is at nearly US$60 trillion annually, making them one of the fastest-growing segments in the global financial market.

Jane Street recognised this opportunity earlier than most.

While many traditional banks viewed ETF market making as a niche activity, Jane Street invested heavily in the technology, infrastructure and mathematical models required to price and trade increasingly complex ETF products.

This proved to be a significant competitive advantage.

Unlike an individual stock, an ETF can contain dozens, hundreds or even thousands of underlying securities. Determining its fair value and price discovery requires continuously analysing the prices of all those underlying assets while simultaneously monitoring supply and demand for the ETF itself.

The complexity creates opportunities.

Whenever an ETF trades slightly above or below the value of its underlying holdings, Jane Street can buy in one market and sell in another, capturing small profits through a process known as arbitrage.

On their own, these pricing discrepancies may be tiny.

However, when identified and executed millions of times across thousands of products, they can generate enormous profits.

In many ways, the growth of ETFs created the perfect environment for a firm like Jane Street. The more ETFs that launched, the greater the complexity of the market became and the more valuable Jane Street’s technology and trading systems became.

As ETF adoption accelerated, so did Jane Street’s profits.

Jane Street Thrives Off Volatility

For most investors, volatility is something to be wary of.

Sharp movements can wipe large chunks from portfolios, increase uncertainty and make forecasting significantly more difficult.

For Jane Street, volatility creates opportunity.

The firm’s business depends on facilitating trades between buyers and sellers. When markets become more active, trading volumes usually increases as investors reposition portfolios, hedge risks or react to new information.

More trading activity means more opportunities for Jane Street to earn profit from spreads and discover pricing inefficiencies.

This dynamic helps explain why some of the firm’s strongest years have coincided with periods of elevated market volatility.

During times of market stress, the differences between prices in related securities often widen. ETFs can temporarily trade away from the value of their underlying holdings, options can become mispriced and liquidity can deteriorate across certain markets.

For firms with sophisticated trading systems, these dislocations can create profitable arbitrage opportunities.

Unlike traditional investors who rely on markets rising over time, Jane Street’s profitability is instead linked to market activity itself.

Whether markets are rallying or falling is often less important than whether investors are actively trading.

This distinction helps explain why Jane Street has been able to thrive during periods that most investors would consider troublesome and challenging.

The firm is not necessarily betting on markets going up or down.

Instead, it profits from the constant movement occurring between them.

As global markets have become increasingly interconnected, complex and volatile, that opportunity set has only grown larger.

The Mathematics Behind The Machine

While many people associate Wall Street with bankers, traders and finance graduates, Jane Street has built its success by recruiting a very different type of employee.

The firm is famous for hiring PhD’s, mathematicians, physicists, computer scientists and competitive problem-solvers rather than traditional finance professionals and graduates.

Many candidates often have little or even no prior deep knowledge of financial markets.

Instead, Jane Street looks for people who excel at ] complex problem solving under uncertainty.

The firm’s interview process reflects this philosophy. Candidates are asked probability questions, logic puzzles and game theory problems rather than traditional finance, valuation, market or accounting questions.

This culture has led many observers to describe Jane Street as a hybrid between a tech company, mathematics department and trading firm.

One influence frequently cited by former employees is poker.

Successful players make decisions with incomplete information, constantly update probabilities as new information emerges and focus on expected value rather than absolute certainty. The same principles underpin many of their trading strategies.

This probabilistic approach is embedded throughout the organisation.

Rather than attempting to predict where markets will move, Jane Street focuses on identifying situations where odds seem favourable, then executing those opportunities consistently on a massive scale.

Technology plays an equally important role.

The firm invests heavily in software, algorithms and infrastructure capable of processing enormous volumes of market data in real time. In modern financial markets, identifying a pricing discrepancy is only half the challenge. The other half is executing the trade before anyone else notices the opportunity and does it themselves.

A human blinks in less than half a second.

In that same half a second, Jane Street’s systems can analyse thousands of securities, identify potential arbitrage opportunities and execute trades across multiple markets.

The combination of elite talent, advanced technology and a culture obsessed with problem-solving has created one of the most formidable trading organisations in the world.

It also helps explain why Jane Street increasingly resembles a technology company that happens to trade financial markets rather than a traditional Wall Street firm.

The Regulatory Problem

Success on this scale is going to attract attention.

For years, Jane Street operated largely outside the public spotlight. While investors, exchanges and institutional market participants were familiar with the name, it remained relatively unknown to the broader public.

That is now starting to change.

India

In recent years, regulators have increasingly scrutinised the role of quant trading firms and market makers within financial markets. The most significant challenge currently facing Jane Street stems from an ongoing investigation into its trading activities in India.

Indian regulators have accused the firm of manipulating stock and derivatives markets through trading strategies that allegedly influenced market prices to its advantage.

Jane Street strongly disputes these allegations.

The firm argues that its trading activity provides a service by providing liquidity and helped facilitate orderly markets, a role that market makers have historically performed across global exchanges.

At the centre of the debate is a broader question that extends beyond Jane Street itself.

When firms possess superior technology, greater speed and access to vast amounts of market data, where should regulators draw the line between legitimate competitive advantage and unfair market influence?

Supporters argue that firms such as Jane Street improve market efficiency by narrowing bid-ask spreads, increasing liquidity and helping investors transact at better prices.

Critics contend that increasingly sophisticated trading strategies may create advantages that are difficult for other market participants to overcome, potentially concentrating power within a small number of highly sophisticated firms.

China

The scrutiny is no longer limited to India.

Reports suggest regulators in other jurisdictions, including China, have also started to examine the role quant trading firms play in markets.

Whether these investigations ultimately lead to meaningful regulatory changes remains uncertain.

What is clear, however, is that the more successful Jane Street becomes, the harder it will be for the firm to remain out of the public light.

What Jane Street Says About The Future Of Wall Street

The story of Jane Street is really story of how Wall Street is changing.

For much of the 20th century, the most powerful institutions in finance were traditional banks. Banks that dominated markets through huge balance sheets, client relationships and access to capital.

Today, a different type of firm is emerging.

Companies such as Jane Street, Citadel, Hudson River Trading and XTX Markets increasingly derive their advantage from technology, data and mathematics instead of traditional banking activities.

Their competitive edge is not built on lending money or relationships. It’s built on algorithms, computing power and the ability to process information the fastest.

The growth of electronic trading has reduced the importance of physical trading floors. The rise of ETFs has created increasingly complex markets that favour sophisticated quantitative firms. Advances in computing power have made it possible to analyse vast amounts of data and execute trades in milliseconds.

At the same time, post-GFC regulation has limited certain activities previously dominated by large banks, creating opportunities for specialist trading firms to expand their market share.

Jane Street sits at the intersection of all these developments.

The firm resembles a technology company as much as a financial institution. Its employees are as likely to hold degrees in mathematics, physics or computer science as they are in finance. Its success depends as much on software and engineering as it does on market knowledge.

This raises an important question for investors and finance professionals alike.

If the future of finance increasingly belongs to firms like Jane Street, the skills required to succeed may also be changing.

The modern trading floor is no longer dominated solely by traders shouting orders across a room. Increasingly, it’s populated by programmers, engineers, statisticians and quants building systems capable of navigating ever more complex markets.

Whether Jane Street can maintain its advantage remains to be seen. Competition is intensifying, regulatory scrutiny is increasing and markets continue to evolve.

One thing is clear, future of Wall Street will likely look far more technological, quantitative and data-driven than its past.

And few firms embody that transformation better than Jane Street.