Market context

Inghams Group (ASX: ING) shares dropped as much as 14% in early trade on Monday 22 June 2026 and closed down 4.2% at A$2.01, after the company locked down its Western Australian farms and processing operations. The trigger was Australia’s first detection of the H5N1 strain of avian influenza, found in two wild seabirds in the Esperance region of WA. Inghams was clear that the virus has not been found in any commercial poultry, including its own birds and supply chain, and that its WA sites sit more than 690 kilometres from where the wild birds were found.

So the immediate hit to earnings is, on the company’s own account, close to nothing. That is why the stock clawed back most of its intraday loss by the close. The market treated the headline as a scare, sold first, then thought about it.

The trouble is what the scare distracts from. Monday was the third double-digit shock to Inghams in ten months. The stock fell about 22% on its FY25 result in August 2025, then 13% on its first-half FY26 result in February 2026, when management cut full-year guidance and profit fell by two thirds. It closed the 2025 financial year at A$3.55 (30 Jun 2025). At A$2.01 it has lost roughly 43% of its value in under a year. Bird flu is the noisiest of the three blows and the least fundamental. It is also the one pulling retail attention away from the other two.

The thesis

This is a call about margin of safety, not about chicken demand. Inghams sells the cheapest mainstream protein in the country, and volumes are stable. The problem is that almost none of the value of a thin-margin, capital-hungry processor accrues to equity holders once net debt sits at A$466.1m and earnings are falling. You are not buying a fortress at a discount. You are buying operating and financial leverage at a moment when a new biosecurity risk has just walked onto the continent.

What the dip-buyers in Inghams shares are missing

Start with the label. Inghams is filed under consumer staples, and the instinct on any staples sell-off is to buy the dip. But a staple is only defensive if its earnings are. Inghams converts about A$3.15bn of revenue (FY25) into roughly A$236m of underlying EBITDA before lease accounting, a margin near 7.5%. Strip rent and depreciation and interest out of that thin slice and not much is left for shareholders. In the first half of FY26 that margin fell to 5.0% and underlying profit dropped 64.9% to A$18.1m. A business that loses two thirds of its profit on a single half of cost pressure is geared, not defensive. The “staple” framing is doing a lot of unearned work in the bull case.

Then the balance sheet. Net debt rose to A$466.1m at 31 December 2025, pushing leverage to 2.4 times underlying EBITDA, above the company’s own 1.0 to 2.0 times target range. Leverage is a multiplier in both directions. It is why the equity fell 22% and 13% on results that, at the asset level, were disappointing rather than disastrous. It is also why the dividend is already being rationed: the interim payout was cut to 4.0 cents from 11.0 cents a year earlier. A genuinely defensive holding does not cut its dividend by nearly two thirds in a soft patch.

Now the part the market has barely touched. H5N1 had never reached the Australian mainland before this month. Australia was the last inhabited continent free of the strain, kept out by distance and migratory flight paths rather than by anything Inghams controls. That barrier has now been crossed. The single wild-bird detection is not the story. The repricing of probability is. The base rate for a commercial-flock outbreak in Australia just moved from near zero to something real, and overseas experience shows what that looks like: mass culls, movement restrictions, and biosecurity costs that land on producers, not consumers. A company carrying 2.4 times leverage is exactly the wrong balance sheet to meet a fat new left tail. Monday’s 4% close was a sentiment wobble. It was not the market sitting down and pricing that tail.

The contrarian point, then, runs against the obvious contrarian trade. The crowd buying Monday’s dip is fighting the last problem, the one that is 690 kilometres away and already fading. The problem worth pricing is structural, sitting on the balance sheet and in the migratory calendar, and it has not been discounted at all.

The numbers

| Metric | Figure (dated) | Read |

|---|---|---|

| Share price | A$2.01 (22 Jun 2026), down ~43% from A$3.55 (30 Jun 2025) | Three double-digit shocks in ten months |

| Market capitalisation | ~A$748m (22 Jun 2026; ~371.7m shares) | Now a small-cap |

| Enterprise value | ~A$1.21bn (market cap + net debt) | Debt is ~38% of enterprise value |

| Revenue | A$3.15bn FY25 (-1.5%); A$1.61bn 1H26 (-0.1%) | Volumes stable, top line flat |

| Underlying EBITDA (pre-AASB 16) |

A$236.4m FY25 (flat); A$80.6m 1H26 (-35%) | Margin compression is the story |

| NPAT | A$89.8m FY25 (-10%); A$18.1m 1H26 (-65%) | Operating leverage cuts both ways |

| FY26 guidance (underlying EBITDA) |

A$180m–A$200m, cut from A$215m–A$230m (20 Feb 2026) | Recovery skewed to Q4 and remains unproven |

| Net debt / leverage | A$466.1m; 2.4x (31 Dec 2025), above the 1.0–2.0x target | The defensiveness killer |

| Dividend | Interim 4.0c, cut from 11.0c; 12c trailing, fully franked | Already being rationed |

| Valuation | EV/EBITDA ~6.4x on FY26 midpoint; P/E ~13x trailing; P/B ~2.9x | Not distressed pricing |

The valuation point sits in that last row. At A$2.01 Inghams trades on roughly 6.4 times the midpoint of its own downgraded FY26 EBITDA guidance, around 13 times trailing earnings, and close to three times book. None of those are distressed multiples. The stock looks beaten up because the chart is ugly, but the price you pay is a mid-cycle multiple on a trough that has not been confirmed.

What it is worth

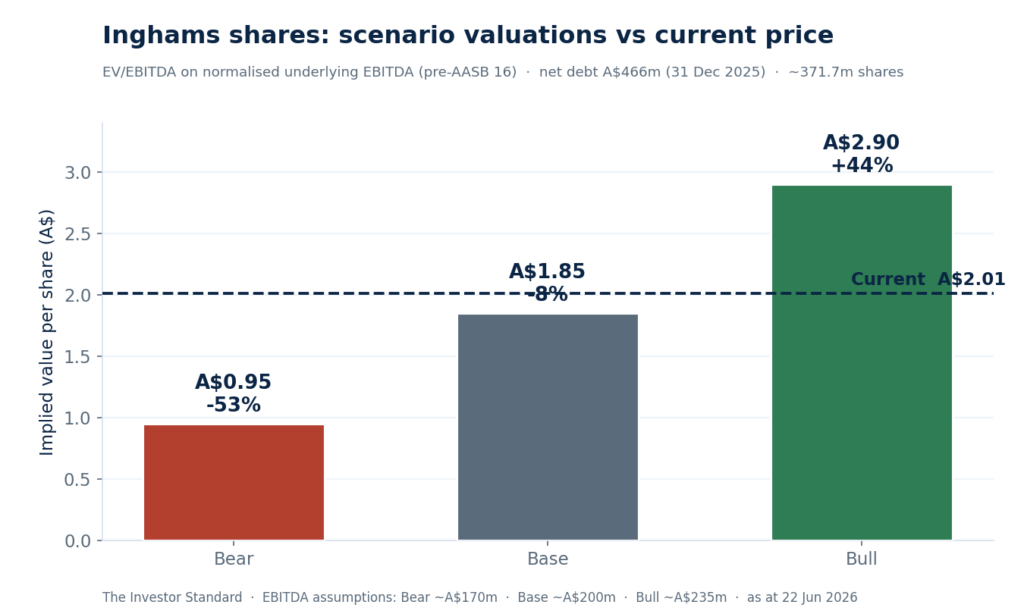

Comparable ASX-listed processors are thin and the lease accounting makes headline EV/EBITDA multiples noisy across names, so we anchor valuation on Inghams’ own normalised earnings power rather than on a peer screen. The framework is simple and deliberately so: a defensible range of normalised underlying EBITDA (pre-AASB 16), a sector-appropriate EV/EBITDA multiple of 5.0 to 6.5 times, net debt held near the reported A$466m, and about 371.7m shares.

| Case | Assumptions | Implied value | vs A$2.01 |

|---|---|---|---|

| Bear | EBITDA ~A$170m, 5.0x multiple, with net debt rising to ~A$490m due to biosecurity costs and a soft fourth quarter. | ~A$0.95 | -53% |

| Base | EBITDA ~A$200m at the top of guidance, a 5.75x multiple and net debt of approximately A$466m. | ~A$1.85 | -8% |

| Bull | EBITDA ~A$235m, reflecting a return to FY25 levels, a 6.5x multiple and net debt easing to ~A$440m. | ~A$2.90 | +44% |

The shape of that table is the whole argument. The base case, which assumes Inghams lands at the very top of guidance it has already cut twice, still sits below the current price. The bull case needs earnings back at FY25 levels and a re-rating, the kind of clean operational turnaround management has promised and missed two halves running. The bear case, a plausible one if H5N1 reaches a commercial flock, more than halves the equity. You are being offered a few cents of base-case downside and 44% of bull-case upside against 53% of bear-case downside. That is the wrong way round for a high-conviction buy.

The sensitivity grid makes the same point in finer grain. Holding net debt at A$466m, here is implied value per share across EBITDA and multiple:

| EV/EBITDA → | 5.0x | 5.75x | 6.5x |

|---|---|---|---|

| EBITDA A$170m | A$1.03 | A$1.38 | A$1.72 |

| EBITDA A$200m | A$1.44 | A$1.84 | A$2.24 |

| EBITDA A$230m | A$1.84 | A$2.30 | A$2.77 |

Only the bottom-right corner, full earnings recovery on a generous multiple, clears today’s price with any room to spare. Most of the grid sits below A$2.01. The market is not pricing a bargain. It is pricing a fair-to-full outcome on numbers that still have to be delivered.

Catalysts & Risks

The FY26 full-year result on 21 August 2026 is the swing point. The market needs to see whether the Q4-weighted recovery arrived, what happens to the dividend and where leverage lands.

Running underneath that is the Western Australian bird flu situation through winter. Any movement from wild birds into a commercial flock could trigger culls and operating restrictions.

Delivery of the cost-out program into FY27, the path of grain and feed costs, the net-debt trajectory against the 2.0x policy ceiling and the supermarket contract backdrop after the Woolworths volume reset.

A depressed enterprise value may also keep corporate interest alive. Inghams was a private-equity asset before its 2016 listing.

This is a contrarian call, so the bull case deserves a fair hearing. Chicken remains the cheapest major protein and demand may hold up in a downturn.

Two guidance cuts may have lowered expectations enough for a Q4 recovery and easier FY27 comparisons to surprise positively. Three directors also bought shares near A$2.00 in late May 2026, signalling that insiders see value around current levels.

The fully franked dividend still pays, and the H5N1 detection may remain confined to wild birds. If these factors line up, the bull case near A$2.90 remains live and our caution would be wrong.

Read More

What would change the view

We would turn constructive on Inghams shares on evidence, not on a bounce. The triggers: an FY26 result that lands at or above the top of guidance with the operational improvements visibly delivered, not deferred again; leverage falling back toward 2.0 times; a clean migratory season with H5N1 contained in wild birds and no commercial-flock incursion; and FY27 guidance that points to margin recovery rather than another year of cost absorption. Any two of those would rebuild the margin of safety that A$2.01 does not currently offer.

Investor takeaway

The reflex to buy a defensive name on a bird flu scare is understandable and, this time, misplaced. The sell-off is an overreaction to a distant event, but cheap-looking and cheap are not the same thing. On normalised earnings Inghams trades near fair value, its balance sheet removes the very defensiveness that makes the dip tempting, and the first arrival of H5N1 on the continent has handed the sector a new tail risk that Monday’s price barely acknowledged. The asymmetry runs the wrong way: limited base-case upside against a bear case that halves the equity. We would let this one prove the turnaround at the August result before paying mid-cycle multiples for a trough that is not yet confirmed. The dip is not the opportunity. It is the distraction.